What is a UPI Merchant? Understanding UPI Merchant Accounts

Ravi runs a small grocery store in a busy lane where most customers pay through UPI. He checks his phone after every transaction to confirm the payment. One evening, a customer shows a success screen, but the amount does not appear in his account.

Ravi feels unsure about what went wrong and where to check the status. Many business owners face this when they accept payments but do not understand how the system works. This blog explains how a UPI merchant account works, along with its charges, benefits, and setup process.

What is a UPI Merchant?

If you run a business and accept payments through UPI, you are already working as a UPI merchant. It could be a shop, a small stall, or even a freelance setup where clients pay you online.

Instead of money coming in without a trail, every payment gets recorded properly. You can go back and check who paid, how much they paid, and when it happened.

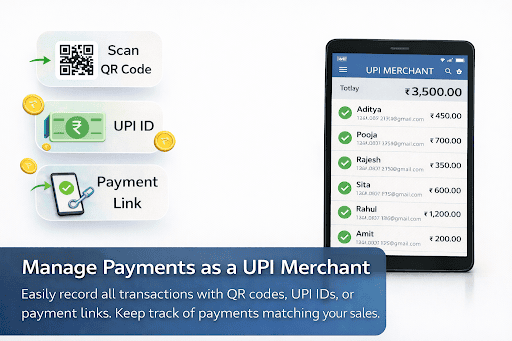

A UPI merchant account makes this easier. You can collect payments using a QR code, a UPI ID, or even a simple payment link. Over time, this record becomes useful because you always know if your payments match your actual sales.

Also Read: How to Create Your UPI Number Using a Mobile Banking App

UPI Merchant Account Benefits

Once you start using UPI for business, you notice the difference almost immediately. Payments feel faster, and you do not have to deal with loose cash or constant change.

A UPI merchant account also makes UPI merchant payment tracking easier, especially when your daily transactions start increasing.

- Money comes in instantly, which helps with daily cash flow

- Banks secure each transaction, so you do not have to worry about safety

- Customers can pay from any UPI app without asking questions

- You get a clean record of all payments in one place

- Handling more customers becomes easier during busy hours

Also Read: Merchant QR Code: Meaning & How to Get

Charges for UPI Merchant Payments

This is one of the first questions most business owners ask. The good news is that most UPI payments do not incur a Merchant Discount Rate(MDR), a fee is charged for accepting digital payments. So you usually receive the full amount.

Some platforms may charge for additional features, such as detailed reports or payment gateway services. These are optional and depend on what you choose to use.

Simple example:

Payment received = ₹2,000

MDR = ₹0

Final amount = ₹2,000

This is why many small businesses prefer UPI. The cost stays low, and the process stays simple.

Also Read: GST on UPI Payments: Everything You Need to Know

How does UPI Merchant Payment Work?

The process may look technical, but it happens in seconds and follows a simple flow.

Step 1: The customer enters your UPI address or scans the QR code

Step 2: Your name appears on their screen for confirmation

Step 3: They enter the amount and approve it with their PIN

Step 4: The bank processes the request instantly

Step 5: The amount gets credited to your account

Step 6: Both of you receive a confirmation message

How to Create a UPI Merchant Account?

Setting up your account does not take much time. Most apps guide you step by step, so you do not feel stuck at any point.

Step 1: Download a trusted payment or UPI app

Step 2: Register using your mobile number linked to your bank

Step 3: Complete KYC with basic business details

Step 4: Set up your UPI ID for receiving payments

Step 5: Generate your QR code

Step 6: Start accepting payments and track them digitally

Who Should Use a UPI Merchant Account?

If you accept payments regularly, this system makes your life easier. It works for almost every type of small or growing business.

- Local shop owners and street vendors

- Freelancers who get paid by clients

- People running online or home businesses

- Restaurants, cafes, and service providers

- Tutors and consultants handling multiple payments

UPI Merchant Payment Features

Over time, these systems have improved a lot. They do more than just collect payments.

- Easy setup with most apps and platforms

- Quick settlements that keep money moving

- Secure transactions with bank-level checks

- Clear reports that show your daily collections

- Support teams that help when something goes wrong

Stay in Control of Your Payments with Hero Fincorp

Understanding digital payments gives you more control over your business. When you know how transactions flow and how records stay updated, you can focus on growth instead of chasing payments.

Hero Fincorp supports this journey with simple tools and reliable systems. You can explore financial solutions, use the personal loan app, check eligibility online, and apply here when you need quick support for your business needs.

Frequently Asked Questions

What is the difference between a merchant UPI account and a personal UPI account?

A merchant account maintains proper records of business payments, while a personal account is meant for individual use and does not offer detailed tracking.

How do I open a UPI merchant account with Herofincorp?

You can sign up on their platform, complete KYC, create your UPI ID, and start accepting payments using a QR code.

Are there any charges for UPI merchant payments?

Most UPI payments do not have MDR, but some platforms may charge for added services.

Is the merchant UPI account free to create?

In most cases, yes. Some advanced features may incur a fee, depending on the provider.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.