GST on UPI Payments: Everything You Need to Know

- What Is GST on UPI Payments?

- Current Applicability of GST on UPI Transactions in India

- GST on Transaction Amount vs GST on Service Charges

- Government Notifications and Updates on GST for UPI (As of 2025)

- Who Bears the GST Burden on UPI Payments?

- Make Better Payment Decisions with Hero FinCorp

- Frequently Asked Questions

- Is GST applicable to every UPI transaction in India?

- Can small merchants claim Input Tax Credit on the GST paid for UPI service charges?

- What is the threshold for mandatory GST registration for businesses accepting UPI payments?

- Will GST on UPI payments increase the costs for consumers?

- How do payment aggregators handle GST compliance on UPI transactions?

- Are cross-border UPI transactions subject to GST in India?

UPI is a popular payment method in India.

In October 2025, UPI transactions reached ₹27.28 lakh crore in value. But what if you have to pay tax on it?

Rumours have it—UPI transactions exceeding ₹2,000 can attract an 18% Goods and Services Tax (GST)! But is it true or just a hollow speculation? And if GST on UPI payments is indeed an impending reality, what should you know about it? Read on as we discuss everything.

What Is GST on UPI Payments?

To understand GST on UPI payments, you first need to understand the indirect tax landscape of India.

India currently has only one major indirect tax—GST. It’s a single, unified indirect tax that’s levied on the supply of goods and services.

GST is destination-based and levied at every stage of the supply chain. The four GST tax slabs are 5%, 12%, 18%, and 28%. Moreover, some items like petrol, alcohol, and electricity are outside the purview of GST.

A UPI payment doesn’t classify as a supply. So, when we say GST on UPI transactions, it essentially means the tax that is imposed on any fee charged by the payment aggregator (Google Pay, PhonePe, Paytm, etc.) or the bank, not the transaction value itself.

Also Read: What is CGST & SGST? Key Differences Between Them

Current Applicability of GST on UPI Transactions in India

There’s serious confusion about GST on UPI payments—in some cases, it’s not applicable, but in others, it is. So, here’s a table that summarises the situation:

| Transaction Type | Amount Threshold | Is There Any Fee? | GST Applicable? |

|---|---|---|---|

| P2P (Person-to-Person) | Any amount | No | No |

| P2M (Person-to-Merchant) | Any amount | No | No |

| M2M (Merchant-to-Merchant) | Any amount | Rarely (MDR, convenience fee, surcharges) | 18% (if charged) |

| P2M via Wallet (PPI) | Above ₹2,000 | Interchange fee of up to 1.1% | 18% |

| UPI Payments with Add-on Services | Any amount | Yes (varies from platform to platform) | 18% |

| Cross-border UPI Payments | Any amount | Yes (varies from platform to platform) | 18% |

| UPI Autopay | Any amount | Sometimes | 18% (if a fee is charged) |

GST on Transaction Amount vs GST on Service Charges

Many people don’t understand the meaning of “GST on UPI payments” or what it exactly entails. So, let’s break it down for you.

GST on UPI transactions doesn’t apply to the transaction value of the payment. Rather, it applies to any fee levied on the same.

A common example is the Merchant Discount Rate (MDR). In M2M UPI transactions, the merchant receiving the payment is often charged a certain percentage of the payment as MDR. GST is taxed on that fee.

Consider this example:

Suppose you’re a merchant who received a UPI payment of ₹50,000 from a fellow merchant. If your bank charges an MDR of 1% for processing the transaction, you will also have to pay an 18% GST on that. This means,

MDR = 50,000 x 1% = ₹500

GST = 500 X 18% = ₹90

You will ultimately receive = ₹50,000 - ₹(500+90) = ₹49,410

Not just MDR—even if you’re charged any service/convenience/interchange fee, the same calculation will prevail.

Government Notifications and Updates on GST for UPI (As of 2025)

As per a recent press release, the Government of India has officially refuted all rumours surrounding GST imposition on UPI transactions above ₹2,000.

As mentioned earlier, GST on UPI applies only to extra charges, such as the Merchant Discount Rate (MDR). Since the government removed MDR on Person-to-Merchant (P2M) UPI transactions in January 2020, there is no GST applicable on these transactions.

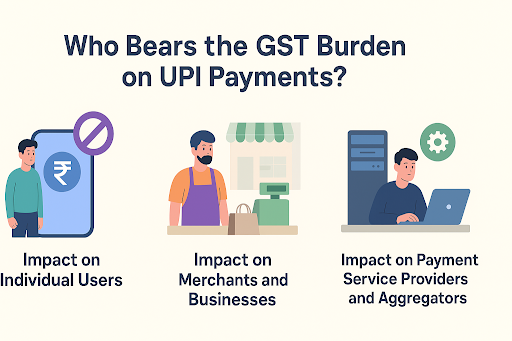

Who Bears the GST Burden on UPI Payments?

Now, let’s come to the most crucial part of the discussion—will GST on UPI payments affect your budget? Let’s see:

Impact on Individual Users

If you’re an individual who relies on UPI for every payment, relax—you’re least likely to be affected by GST.

As mentioned earlier, all P2P and P2M UPI transactions are not subject to GST. The 18% GST on P2M UPI transactions is borne by the merchant, not you. However, there can be indirect effects.

If merchants incur GST on MDR or other charges, they might increase product prices or add small convenience fees. So while GST isn’t charged to individual users on UPI transactions, the final cost of goods or services may still reflect it.

Splurged via UPI a bit too much? Don’t worry—apply for a personal loan instantly with our Instant Loan App now!

Impact on Merchants and Businesses

If you’re a merchant, you will face the real impact of GST on UPI transactions.

Whenever a bank or payment aggregator charges MDR, convenience fees, or interchange fees, GST is added on top. This will increase your operating cost. You can either absorb it, build it into pricing, or impose small digital payment surcharges.

However, you must weigh customer experience against margins and choose whether to pass the GST burden forward.

Impact on Payment Service Providers and Aggregators

Payment apps have small profit margins. Any service fee they charge—gateway, interchange, convenience fees—is subject to GST. This increases their costs and might make them change MDR rates, pricing, or operations to stay competitive.

It also affects their negotiating power with banks and merchants, especially for high-volume transactions.

Also Read: What is the Structure of GST in India?

Make Better Payment Decisions with Hero FinCorp

UPI is still one of the cheapest and most convenient ways to move money in India. The only time GST shows up is when there’s an extra fee involved—not on the payment itself.

As long as you understand where these charges kick in (wallet payments, add-on services, cross-border transfers, or M2M fees), you’re solid. For everyday users and most merchants, nothing really changes.

And if you're planning something big and need quick funding, apply for a personal loan with Hero FinCorp!

Also Read: What is CGST & SGST? Key Differences Between Them

Frequently Asked Questions

Is GST applicable to every UPI transaction in India?

No, GST isn’t applicable to every UPI transaction in India. Only if the payment aggregator you use levies a service charge will it be treated as GST.

Can small merchants claim Input Tax Credit on the GST paid for UPI service charges?

Yes, small merchants can claim Input Tax Credit (ITC) on the GST paid for UPI transactions, provided they are registered under GST and the service charge is levied on business-related transactions.

What is the threshold for mandatory GST registration for businesses accepting UPI payments?

In most states, the mandatory GST registration threshold for businesses supplying goods is ₹40 lakhs, and for those supplying services, it is ₹20 lakhs.

Will GST on UPI payments increase the costs for consumers?

Not really. UPI transfers are free, so there’s no GST on the payment itself. Costs only rise if a payment app adds a service or platform fee, and that fee is subject to GST.

How do payment aggregators handle GST compliance on UPI transactions?

Payment aggregators don’t charge GST on regular UPI transactions. GST applies only to any service or platform fees they levy. Aggregators collect this GST from the merchant or customer (whoever pays the fee) and deposit it with the government, issuing a tax invoice for the same.

Are cross-border UPI transactions subject to GST in India?

No, cross-border UPI transactions aren’t inherently subject to GST in India. However, if the UPI platform charges any fee for the same, it will attract GST.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

A decade ago, if someone said cash payments would have a serious rival, no one would’ve believed it. But today, that’s a reality.

For daily necessities like shopping, bill payments, subscriptions, and EMI repayments, people in India rely on a variety of payment methods. With the widespread acceptance of cards, wallets, and UPI apps, digital payments have become commonplace.

A few years back, leaving home meant checking for your wallet first. Cash, bank cards, faded receipts, maybe a few coins rattling around. Now, many of those payments happen through a phone without much thought. Tap at the kirana store, scan to pay the cab driver, and settle a bill while standing in line. Digital wallets have slipped into everyday life across India.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.