Abhishek Singh

Socials :

Blog By Author

Jignesh, a salaried agent, needed Rs. 3 lakhs for a family emergency. He applied for a personal loan, because he needed urgent funds and did not have investments to use as collateral.

For daily necessities like shopping, bill payments, subscriptions, and EMI repayments, people in India rely on a variety of payment methods. With the widespread acceptance of cards, wallets, and UPI apps, digital payments have become commonplace.

A few months ago, Vivek took a small consumer durable loan to buy a laptop. Around the same time, he already had a bike EMI running, and used his credit card heavily during a family trip. Later, when he applied for a personal loan, the lender said his credit exposure looked higher than expected.

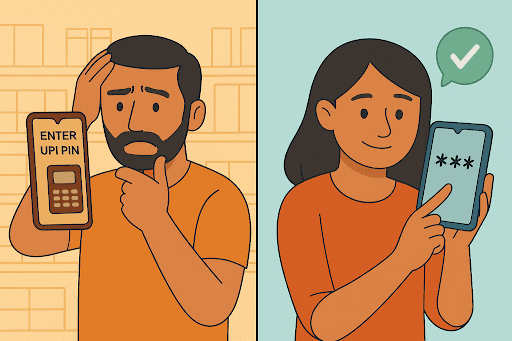

A few days ago, Mehul tried paying for groceries in Pune and suddenly blanked on his UPI PIN. That same evening, Ananya in Jaipur set up a brand new one after opening her bank account. Simple situations, yet both show how much we rely on that small number without thinking about it.

Purchasing a house is one of the most important events in one's life. Mr. Rohit Bawa wanted to move from his rented home to a house of his own. But he did not have the required funds for paying the down payment for a home loan. So, he considered getting personal loans for a down payment on a house.

Rahul had taken a personal loan two years ago to fund a family emergency. He paid his EMIs diligently for 18 months. Then came an unexpected job loss. Struggling to keep up, he called his lender and asked: “Can I just settle the loan?” The lender said yes - for a reduced amount. Rahul thought he had dodged a bullet.

When it comes to expenses related to higher studies, managing everything only through savings can be difficult. An instant Personal Loan for Education helps bridge this gap by providing quick funding to cover tuition fees, laptop costs, hostel charges and other related expenses without collateral. Since this is structured as a personal loan rather than a traditional education loan, repayment begins right after borrowing via monthly EMIs, making proactive repayment management crucial from day one.

Ever wondered what you’re really signing up for when you take a loan? Financial obligations in loans go beyond just borrowing money. They’re the commitments you make...

Ramesh needed funds, but there was no lending option available to him. When he researched his options, he learned about microcredit.