RBI’s New 2FA Rule for Digital Payments

- What is RBI’s New 2FA Rule?

- Why RBI is Implementing the New 2FA Rule

- Accepted Authentication Factors Under RBI 2FA Rule

- Impact on Digital Payment Channels

- Risk-Based Authentication (RBA) Explained

- RBI 2FA Rule for Cross-Border Transactions

- Responsibilities and Compliance for Payment Providers

- Key Exemptions to RBI’s 2FA Rule

- How Hero FinCorp Supports Secure Digital Payments

- Conclusion

- Frequently Asked Questions

Mr. Rao booked his dinner order through an app and confirmed the transaction using his UPI PIN. This security measure is part of the 2FA rule, which has been initiated by the RBI for digital payments.

Digital payment methods in India are being used tremendously. Almost 20 billion UPI transactions were made in one month in 2025.

This raises concerns related to user protection and the need to mitigate fraudulent activities.

The newly implemented 2FA rule for digital payments came into effect in April 2026. Under this rule, most of the transactions will be verified twice before making any payments.

What is RBI’s New 2FA Rule?

The new RBI guideline for 2FA mandates that before initiating any transaction, the system should authenticate the user through the use of two different means of identification.

2FA includes:

- Something the user knows (PIN/Password)

- Something the user possesses (Mobile/OTP)

- Something the user is (biometric verification)

Under the updated digital payments 2FA rules, payment providers must ensure that digital transactions-whether through cards, UPI, or wallets - follow this layered authentication process.

The objective of the 2FA rule for digital payments is simple - to make digital payments more secure while maintaining a smooth user experience.

Why RBI is Implementing the New 2FA Rule

The RBI introduced digital payments 2FA rules to counter cybersecurity risks in digital transactions.

Some of the reasons behind the RBI 2FA rule include:

- Rising digital payment volumes increase fraud exposure

- Online phishing and payment scams that compromise users' security

- Protection of consumer data and funds

- Following the global payment security standards

- Increasing the reliability of digital finance systems

Instances of digital payment fraud have compelled regulatory authorities to improve the authentication process.

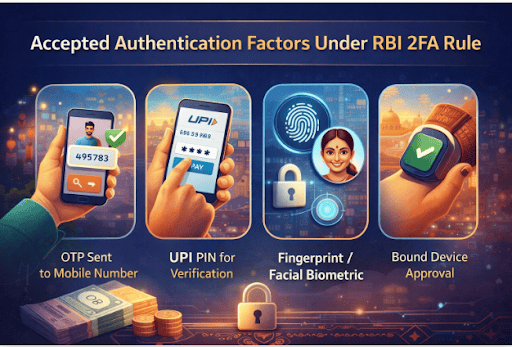

Accepted Authentication Factors Under RBI 2FA Rule

Under the 2FA rule for digital payments, authentication must use two different types of factors.

- Accepted authentication methods under the RBI 2FA rule include:

- OTP (One-Time Password) sent to a registered mobile number

- UPI PIN for transaction verification

- Fingerprint or facial recognition through biometric authentication

- Approval of the transaction via a bound device

- Password or transaction PINs

Such levels of authentication will help protect the transaction even when a single layer gets compromised.

Impact on Digital Payment Channels

The implementation of digital payments 2FA rules affects several payment channels across India.

| Payment Mode | RBI’s new 2FA rule |

| UPI payments | Mandatory two-step authentication before approval |

| Card transactions | OTP or additional authentication required |

| Mobile wallets | Multi-layer verification during payments |

1. UPI Payments

RBI’s new 2FA rule strengthens UPI payment security by:

- Authenticating transactions using UPI PIN and device validation

- Checking high-value transactions

- Employing better fraud monitoring mechanisms

Under the 2FA rule for digital payments, such measures ensure that UPI payments remain convenient and secure.

Also Read: How to Change UPI PIN

2. Card Transactions

Card-based payments also fall under the RBI 2FA rule, which must include:

- OTP verification for card payments

- Secure PIN authentication

- Tokenisation-based card protection

3. Mobile Wallets and Prepaid Instruments

These methods also need to comply with the 2FA rule for digital payments by:

- Verifying OTP for transactions

- Authenticating devices for access to the wallet

- Using transaction alerts for user monitoring

Risk-Based Authentication (RBA) Explained

Along with the RBI’s new 2FA rule, financial institutions may also use Risk-Based Authentication that analyses factors such as:

- Location of the device used for payments

- Transaction behaviour of the user

- Amount of payment

- Spending patterns of the user

Low-risk transactions may go through smoothly, while high-risk transactions may need further verification. This helps maintain security and convenience.

RBI 2FA Rule for Cross-Border Transactions

International digital transactions must follow the RBI 2FA rule, and they may require:

- OTP-based authentication

- Device verification

- Card tokenisation mechanisms

Responsibilities and Compliance for Payment Providers

Payment providers need to:

- Apply authentication systems

- Scrutinise and report suspicious activity

- Secure consumer data privacy

- Ensure compliance with RBI guidelines to avoid regulatory penalties.

Key Exemptions to RBI’s 2FA Rule

RBI’s new 2FA rule is mandatory for most digital payments; however, there are certain exceptions, like:

- Low-value payments or recurring ones

- Pre-approved subscription-related transactions

- Specific transactions that fall under RBI-approved limits

- Automated standing instructions

However, even these exemptions follow strict regulatory oversight.

How Hero FinCorp Supports Secure Digital Payments

There is an ongoing need for financial platforms to improve the security infrastructure due to regulatory changes.

Customers can explore digital financial services and check eligibility for a personal loan online through Hero FinCorp’s personal loan journey. Users can also conveniently manage their financial services through the Hero Digital Lending App on Android/iOS.

The security measures taken by Hero FinCorp make its platforms safe and secure to use in accordance with industry regulations.

Conclusion

The digital economy in India continues to grow at an impressive rate, making security a key concern for regulatory authorities and the financial industry. The implementation of 2FA for digital payments by the RBI is one step towards achieving such security and minimising any risk of fraud.

Since all payments require several authentication procedures, the implementation of 2FA for digital payments will ensure that consumers as well as business organisations benefit from greater protection of their transactions within the digital space.

Frequently Asked Questions

Does the RBI’s new 2FA rule slow down digital payments?

Not necessarily. The rule adds another security step, ensuring greater security while keeping transactions quick.

Are small-value transactions affected by the 2FA policy?

Some low-value or periodic transactions may qualify for exemption under the RBI guidelines.

How does the 2FA policy impact international card transactions?

Cross-border transactions require additional authentication under the updated digital payment security framework.

What are acceptable authentication factors under RBI’s 2FA rule?

Examples of authentications that are recognised are OTP, PIN, biometrics, and device-based authentications.

How can risk-based authentication provide a better user experience?

RBA analyses transaction risk and applies additional verification only when necessary.

What happens if a payment provider fails to comply with the RBI’s 2FA rule?

Non-compliance may result in regulatory penalties or restrictions under RBI supervision.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.