Digital Payment in India: Meaning, Types, & Benefits

- What Is Digital Payment in India?

- Why Should You Choose Digital Payments?

- Popular Examples of Digital Payments in Daily Life

- Types of Digital Payments in India

- Important Security Tips for Safe Digital Transactions

- How Do Digital Payments Work in India?

- Benefits of Digital Payments in India

- How Hero FinCorp Supports Your Digital Payment Journey

- Conclusion

- Frequently Asked Questions

India’s financial landscape has evolved.

A decade ago, if someone said cash payments would have a serious rival, no one would’ve believed it. But today, that’s a reality.

As per a government report, the volume of digital payments in India shot up by 44% in 5 years. And with younger generations increasingly using these methods in daily life, it’s expected to shoot up even more.

So, if you’re new to digital payments, read this blog as we discuss its meaning, types, and benefits in depth.

What Is Digital Payment in India?

Digital payment is a payment method that doesn’t involve cash. Both payer and payee use digital platforms or tools to send and receive the amount. Basically, it’s a cashless, electronic method of payment.

Apart from this, some other characteristics that define the digital payment system in India include speed, security, convenience, and traceability.

A day-to-day example of a digital payment in India is a UPI transaction. When a person sends money to another person via a UPI app, it’s considered a digital payment.

Why Should You Choose Digital Payments?

Digital payments have become a faster, safer, and more convenient alternative to cash transactions. They help users transfer money instantly, pay bills online, and complete purchases without carrying physical cash. Digital payment systems also improve financial access for people in remote and developing regions, including low-income groups and women. Enhanced security features reduce the risks of theft, fraud, and cash handling issues. In addition, digital transactions improve transparency by creating proper payment records that are easier to track and manage. Businesses, governments, and organisations can also reduce operational and transaction costs by adopting digital payment systems for everyday financial activities and support fast payments for users.

Popular Examples of Digital Payments in Daily Life

- Mobile Payment Apps: Apps like Google Pay, PhonePe, and PayPal help users make instant payments.

- Digital Cards: Debit cards, credit cards, and prepaid cards are widely used for online and offline transactions.

- Contactless Payments: NFC-enabled cards and mobile wallets allow users to make quick tap-and-pay transactions.

- Bank Transfers: Users can transfer money directly between bank accounts for personal or business payments.

- FASTag Payments: FASTag enables automatic toll payments on highways without stopping vehicles.

- Biometric Payments: Smartphones and banking apps increasingly use fingerprint or face authentication for secure transactions.

Types of Digital Payments in India

There are various types of digital payment methods in India -

1. Unified Payments Interface (UPI)

UPI is a real-time digital payment solution. Built in India, it enables instant money transfer between two bank accounts. All you need is a UPI-enabled application like Google Pay, PhonePe, or Paytm, and you can easily send money without any cash.

As per a report by the Press Information Bureau of India, UPI alone accounts for over 80% of all retail payments across the country.

2. Mobile Wallets

Mobile wallets are digital applications on your smartphone that store money to enable cashless transactions. Some of the most popular mobile wallet apps in India are Paytm, Amazon Pay, and MobiKwik.

3. Banking Cards

Debit and credit cards are also types of digital payment methods. They let users carry out transactions without cash, through online platforms or POS machines.

4. Aadhaar Enabled Payment System (AEPS)

Just like UPI, AEPS is also a digital payment system built in India. It allows users to send, receive, and transfer money at micro-ATMs merely with their Aadhaar number and biometrics. It’s extremely popular in rural areas.

5. Unstructured Supplementary Service Data (USSD)

Most digital payment methods require the internet to function. So, for low connectivity areas, the government introduced USSD. It’s a cellular digital payment method through which you can make payments by just dialling a code. The USSD code for UPI payments and mobile banking is *99#.

6. Other Methods

Apart from the ones listed above, transactions enabled by internet banking, mobile banking, POS systems, and micro-ATMs also qualify as digital payment methods.

Need funds but don’t know whether you qualify for it? Use our Personal Loan Eligibility Calculator; it's free!

Important Security Tips for Safe Digital Transactions

- Use strong passwords with numbers, symbols, and mixed-case letters for all payment and banking apps.

- Enable two-factor authentication for additional account security during digital transactions.

- Keep payment apps and mobile operating systems updated with the latest security patches for safer online payments.

- Avoid making financial transactions over public Wi-Fi networks to reduce data theft risks.

- Activate SMS and app transaction alerts to quickly identify suspicious activity.

- Download payment apps only from official platforms like Google Play Store or Apple App Store to avoid fraudulent applications.

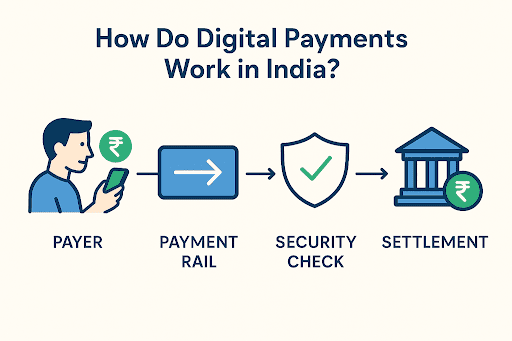

How Do Digital Payments Work in India?

The digital payment system in India basically runs on a simple flow.

There are three parties: the sender, the receiver, and their respective banks.

When a person starts a payment, the request goes through payment networks like UPI, IMPS, or card networks. These systems use PINs, OTPs, or biometrics to ensure the transaction is safe and legitimate.

Once the transaction is approved, the money moves almost immediately. The banks then handle the settlement process in the background.

Benefits of Digital Payments in India

The government encourages the use of digital payments in India, and it’s not a casual plea. Here are a few advantages of using them -

1. Quick and Convenient

Digital payments can be made anytime, anywhere. Moreover, they are executed in real-time. Unlike other cashless methods like cheque payments, they are settled instantly. It makes them both convenient and instant.

2. Better Security

When you pay digitally, your details are scrambled, masked, and checked at different steps so others cannot misuse them. That is why digital payments are generally safe for everyday spending.

3. More Cost-Effective

Digital payments have zero to negligible handling, processing, or labour costs associated with them. This makes them way more economical and cost-effective than most traditional banking methods.

4. Higher Transparency

Every digital payment is duly recorded in the host app with dates, timestamps, and exact transaction details. This makes them transparent and easy to trace.

In fact, a study showed that small businesses that adopted digital payments reduced their monthly account reconciliation time from 8-10 hours to just 2-3 hours.

5. Superior Customer Experience

Customers love how digital payments let them pay fast and without fuss, secure enough for daily use. It just makes the whole process feel better and keeps them coming back.

6. Additional Government Incentives and Promotions

The Indian government often has deals to get people to use digital payments, like cashback, discounts, etc. These deals make it even more attractive to pay online, which gets more people doing it.

Thinking of taking a loan? Use our Instant Loan App to avail a personal loan without hassle!

How Hero FinCorp Supports Your Digital Payment Journey

With digital payment in India becoming an essential part of everyday business and personal finance, having the right financial partner can make all the difference.

At Hero FinCorp, we help you navigate this shift with solutions that integrate seamlessly with digital payments. You can access flexible business loans, fintech support, and tools designed to simplify transaction management, reduce reconciliation time, and enhance your cash flow. For your personal needs, we provide quick and secure personal loans, making digital transactions smoother and more convenient.

By combining technology, tailored financing, and expert guidance, we empower you to make the most of digital payments while growing your financial potential.

So, take charge of your finances. Apply for a personal loan with Hero FinCorp today.

Conclusion

Digital payments in the country have transformed the way people manage everyday financial activities. From UPI and mobile wallets to cards and AEPS, these systems offer speed, convenience, transparency, and security. As adoption continues to grow, users and businesses are increasingly shifting towards cashless transactions for faster and more efficient financial management across personal and professional needs.

Frequently Asked Questions

Are digital payments safe and secure in India?

Yes, digital payments in India are mostly safe and secure.

What are the most popular digital payment methods used in India?

The most popular digital payment methods in India are UPI, mobile wallets, and card payments.

How has demonetisation influenced digital payment adoption?

Demonetisation paved the way for digital payment adoption in India by creating a shortage of cash and compelling people to shift to digital modes.

Can I use digital payments without a smartphone?

Yes, you can use digital payments without a smartphone through the UPI 123PAY system.

What government initiatives support digital payments in India?

The government backs digital payments through UPI, RuPay cards, the BHIM app, and Jan Dhan bank accounts. It also runs various awareness drives and incentive programs.

What fees are associated with digital payments?

Most UPI and bank transfers are free. Cards/wallets may add 1-2% convenience or processing fees.

Which is the safest digital payment method in India?

UPI apps with two-factor authentication, biometric verification, and RBI-regulated banking systems are considered among the safest payment methods.

Are digital payments free in India?

Most UPI and bank transfer transactions are free for users, though certain platforms may charge convenience or service fees.

What is contactless payment?

Contactless payment allows users to complete transactions by tapping NFC-enabled cards or smartphones near compatible payment terminals.

What are the risks of digital payments?

Digital payments may involve phishing scams, fake apps, data theft, unauthorised access, and transaction fraud if users are careless.

How can I avoid UPI scams?

Never share your UPI PIN, OTP, passwords, or banking details, and avoid clicking suspicious payment or refund links.

What happens if a digital payment fails?

Failed digital payments are usually reversed automatically within bank timelines, though some cases may require complaint registration or support assistance.

Can digital payments work without the internet?

Certain services like UPI Lite X support limited offline payments using NFC technology even without active internet connectivity.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

For daily necessities like shopping, bill payments, subscriptions, and EMI repayments, people in India rely on a variety of payment methods. With the widespread acceptance of cards, wallets, and UPI apps, digital payments have become commonplace.

A few years back, leaving home meant checking for your wallet first. Cash, bank cards, faded receipts, maybe a few coins rattling around. Now, many of those payments happen through a phone without much thought. Tap at the kirana store, scan to pay the cab driver, and settle a bill while standing in line. Digital wallets have slipped into everyday life across India.

Ever made an online transfer and wondered where your money went? That’s when the UTR number becomes important. It’s a unique identifier generated for every bank transaction, helping you track payments and resolve issues quickly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.