Different Types of Credit Scores Explained

- Credit Score - An Overview

- Different Types of Credit Scores

- Why Are There Different Types of Credit Scores?

- Understanding Credit Score Ranges

- How are Credit Scores Calculated?

- How to Read and Understand Your Credit Score?

- Tips to Improve Your Credit Score in India

- Importance of Regular Credit Score Monitoring

- Take Control of Your Credit Score Today

- Frequently Asked Questions

Rahul applied for a personal loan and felt confident about its approval. After all, he had a strong 796 credit score in one app. However, when the bank checked it, the score was a bit different. He was baffled, wondering how a single individual could have different credit scores.

Many people don’t realise that there are different types of credit scores, each calculated by a different bureau in its own way. Understanding this can make a big difference in your financial journey.

In this blog, we break down the types of credit scores, the credit ranges and how your credit score is calculated.

Credit Score -An Overview

A credit score helps lenders understand your creditworthiness. The 3-digit number is calculated from your credit report, using the number of credit accounts you have, your repayment history, and other credit-related factors.

Read More: What is a Credit Score? Meaning, Importance, Calculation ...

Different Types of Credit Scores

In India, multiple credit bureaus may use different formulas to calculate a score for the same individual, resulting in varying scores.

There are four leading credit bureaus, which are

- TransUnion CIBIL

- Equifax India

- Experian India

- CRIF High Mark

CIBIL Score: India’s Most Popular Credit Score

- In India, CIBIL is the most trusted credit bureau.

- It stores credit information of more than 1,000 million individuals and businesses worldwide.

- The CIBIL score is the most popular credit score in India. It ranges from 300 to 900 and is used extensively by banks and NBFCs.

Equifax Credit Score Explained

- Equifax India is a joint venture between Equifax Inc. and seven leading financial institutions in India, and has been functional since 2010.

- Equifax generates a score using a specific algorithm and is another important metric lenders use.

- Equifax had set up a separate bureau for Micro Finance Institutions.

Experian Credit Score: What You Need to Know

- The Experian score is globally recognised and also widely used in India.

- It details your credit habits and is usually calculated alongside other credit scores to provide lenders with a broad view of your financial trustworthiness.

CRIF High Mark Score: Emerging Credit Bureau in India

- The CRIF High Mark score is a new type of credit score and has recently become popular amongst lenders.

- It is India's first credit bureau, offering comprehensive credit information for all types of borrowers.

Also Read: CRIF VS CIBIL: Learn Key Differences

Why Are There Different Types of Credit Scores?

There are multiple types of credit scores because each bureau has data from different lenders and its own scoring model.

This leads to slight differences in your score, even though your financial behaviour remains the same.

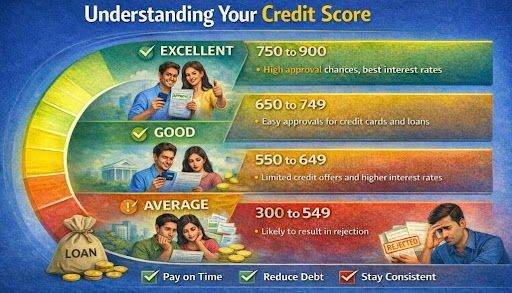

Understanding Credit Score Ranges

These score ranges are important as they help you know where you stand and what lenders see when they evaluate your application.

| Credit Score Range | Category of Credit Score | Score Meaning | Result |

|---|---|---|---|

| 725 to 900 | Excellent | Indicates strong repayment history | High approval chances, best interest rates |

| 650 to 749 | Good | Indicates a strong profile and good financial discipline | Easy approvals for credit cards and loans |

| 550 – 649 | Average | Indicates moderate risk and that the borrower has struggled with repayments | Limited credit offers and higher interest rates |

| 300 to 549 | Poor | Indicates high risk and defaulted payments | Likely to result in rejection |

Read More: What's a Good Credit Score to Get a Loan?

How are Credit Scores Calculated?

Although 3 types of credit scores are commonly discussed, most scoring systems rely on these factors.

| Criteria | Percentage | Effect |

|---|---|---|

| Payment History | 35% | Timely repayments increase your score, while missed payments will reduce it. |

| Credit Utilisation | 30% | Using less than 30% of your credit limit |

| Credit History Length | 15% | Older accounts improve your score |

| Credit Mix | 10% | A mix of secured and unsecured loans strengthens your profile |

| New Credit Inquiries | 10% | Too many applications in a short time can lower your score. |

These form the backbone of credit score calculation across different types of credit scores.

How to Read and Understand Your Credit Score?

To understand your credit score, you have to look beyond the number. Look for patterns in payments, amounts owed, and credit usage in your report.

You can get a clearer picture of your financial situation by comparing credit scores across different bureaus.

Tips to Improve Your Credit Score in India

Improving your credit score in India requires consistent, smart financial habits like

- Paying your EMIs and bills on time

- Keeping your credit utilisation below 30%

- Avoiding multiple loan applications simultaneously

- Having a healthy mix of credit types

- Checking your credit reports regularly

These habits help improve your score across all types of credit scores.

Read More: How to Rebuild Your Credit Score: A Complete Guide

Importance of Regular Credit Score Monitoring

You have to check your credit score regularly to detect errors, catch fraud, and monitor your progress.

It also makes you better informed before applying for loans, so that you can get the best terms and get approved.

Take Control of Your Credit Score Today

Your credit score mirrors your financial history. Understanding your credit score and its importance will help you make informed decisions and be financially responsible.

Check your credit scores online for free from lenders such as Hero FinCorp. You don't have to worry, even if your credit score is low. They offer you several loan options, even with bad credit, based on your overall eligibility.

So, don't wait for your best credit score. Apply for a personal loan or download their Instant Loan App for extra convenience.

Frequently Asked Questions

1. How does my credit score affect my loan approval?

A good credit score makes loan approval easier at better rates, while a poor credit score results in rejection or higher interest rates.

2. Do credit scores differ between bureaus?

Yes, the scores vary as each bureau's information and calculation methods differ.

3. What is a good credit score?

In India, a credit score of 725 is considered good.

4. How often should I check my credit score?

You should check every 3-6 months to stay aware of any changes and detect errors early.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.