Financial Safety Net Before Taking a Personal Loan

Rahul took a personal loan to furnish his apartment. He had no buffer and believed that his paycheck offered him a safety net. After a few months, he had a medical emergency, which cost 1.5 lacs, and his salary was delayed by 45 days.

He panicked. He couldn’t pay the EMIs, and his credit score dropped.

If he had kept an emergency fund aside, he could have easily avoided the situation. Let’s see how you can build a financial safety net before applying for a personal loan.

Why Build a Financial Safety Net Before a Loan?

When you have a loan to pay back, you must follow the repayment schedule. But 60% of borrowers struggle to pay back their loans. A financial safety net helps you avoid a situation where an unexpected situation can dip into your funds, and you can’t pay for the EMI.

A financial safety net reduces stress and gives you more confidence about borrowing decisions.

Plus, you can avoid stress in case your income fluctuates for a certain period.

Key Components of a Financial Safety Net

A financial safety net helps you manage your funds efficiently. Here are key components of a financial safety net:

Emergency Fund Before Loan

Aim to keep funds that can cover six to twelve months of expenses. Account for rent, EMI, groceries, insurance premiums, kids’ school fees, and other expenses. Keep these funds easily accessible.

Insurance Before Borrowing

Make sure that you have sufficient health and life insurance, especially if you have dependents. This protects against financial shocks due to medical reasons. Plus, a credit life insurance helps pay the loan if you pass away before paying the loan.

Debt Management and Reduction

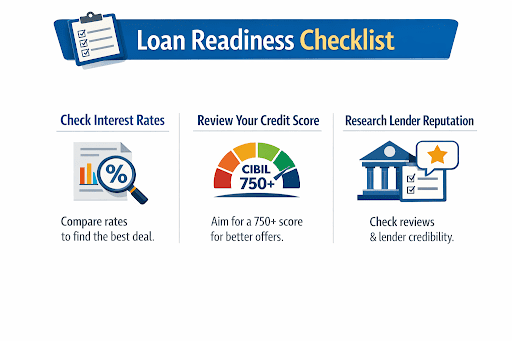

Before applying for a personal loan, try to trim off your existing debts. Pay them off to improve your cash flow. This helps you improve your credit score and lower your DTI, which helps increase your chances of personal loan approval.

Also read: Does Cheque Bounce Affect CIBIL Score?

Types of Loans and Their Financial Implications

Every loan has different terms and conditions. It is essential that you know the financial implications to plan your finances better. Here’s a quick overview of different types of loan, and how they impact your finances:

| Feature | Personal Loan | Home Loan | Car Loan |

|---|---|---|---|

| Purpose | General expenses (wedding, medical) | Constructing or buying a house | Buying a new or used car |

| Interest Rate | Usually higher (unsecured) | Generally lower (property acts as the security) | Moderate (car acts as security) |

| Tenure | Shorter | Longer | Moderate |

| Approval Time | Quick approval | Takes a longer time due to property checks | Moderate approval time |

Also read: Home Loan vs Personal Loan: Key Differences Explained

Building Your Financial Safety Net: Step-by-Step Guide

Now, let’s see a step-by-step guide to building a financial safety net before applying for a personal loan:

- Assess your income and expenses: Look at your income and expenses to cover them. Use budgeting tools to get a clear picture

- Set a savings goal: Decide the amount you want to save. For example, if your monthly expenses are ₹30000, then you should have between ₹180000 and ₹360000 as savings

- Open a separate account: Keep your emergency funds in a separate account from your regular one. This reduces the temptation to use emergency funds for non-urgent needs

- Automate savings: Set up auto transfers to your savings account. Add bonuses, tax refunds, or earnings from side hustle directly into the savings account. This helps you build consistency in your savings habit

- Keep it liquid: Avoid locking in the money in long-term investments. Instead, choose recurring deposits, a savings account, or liquid mutual funds

- Review regularly: Life situations change due to marriage, children, or death. Review your emergency fund every six months to ensure that it aligns with your income and expenses

Common Mistakes to Avoid When Building a Financial Safety Net

Even with the right planning, you may get derailed from your savings strategy. Here’s how to avoid it:

- Avoid using the emergency fund for non-urgent expenses

- Do not take more debt than needed, even if you have a financial safety net

- Don’t keep the money in risky installments that may lose value over time

How Herofincorp Supports Your Financial Preparation

Managing unexpected situations becomes easier with an emergency shield by your side. You can easily avoid a crisis when you have sufficient funds to pay off your expenses and EMIs.

After you are done planning your expenses, getting a personal loan to align with your needs is just as essential. Hero Fincorp offers that support with transparent terms, quick approval, and flexible tenures.

Apply for a personal loan with Hero Fincorp today, and manage your funds confidently.

Frequently Asked Questions

How much emergency fund should I have before applying for a loan?

You should have an emergency fund that can cover expenses between six and twelve months.

What types of insurance are essential before borrowing?

Specific insurance policies offer a financial cushion when securing a loan. You can look for life insurance, credit life insurance, and disability insurance.

How can I improve my credit score quickly?

Pay your existing debts to improve your credit score. Look for any errors in the credit score and resolve them. Make sure that you stick to the repayment schedule of your loan.

How to choose the right loan type for my financial situation?

To choose the right type of loan, assess your requirements, along with your income, expenses, and repayment capacity. Compare loan terms from different lenders to find the right option.

What is the ideal debt-to-income ratio before applying for a loan?

Lenders usually prefer a debt-to-income ratio below 36%, but the specific requirements depend on the lender.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.