What Is a Repayment Schedule for a Personal Loan at Hero FinCorp?

- What Exactly Is a Loan Repayment Schedule?

- Key Components of a Repayment Schedule

- How Is Your Personal Loan Repayment Schedule Calculated?

- Factors Influencing Your EMI Amount

- Types of Repayment Schedules

- Benefits of a Well-Planned Repayment Schedule

- Managing Your Personal Loan Repayment Effectively

- Borrow Responsibly, Repay Confidently

- Frequently Asked Questions (FAQs)

According to a recent study, 74% of borrowers focus on the interest rate. It makes or breaks the deal for them. Next comes the loan’s tenure, processing fee, and ease of application.

For most people in India, the personal loan repayment schedule comes way down on the priority list. Not because it isn’t important or relevant. But because they don’t really know how it affects their financial planning.

So in today’s blog, we’ll break down what is a repayment schedule, its importance, components, types, and effective management. Let’s start!

What Exactly Is a Loan Repayment Schedule?

Also known as a loan amortisation schedule, a personal loan repayment schedule is a detailed blueprint that shows the payments you will make during the loan tenure to repay it. It lists down the key elements of those payments, like their amount, due dates, and EMI breakup (e.g., how much of each payment goes toward principal and interest).

Key Components of a Repayment Schedule

A loan repayment schedule doesn’t have a fixed format. However, here are a few essential elements that generally show up in any repayment schedule:

- Principal Amount: The total loan amount borrowed

- Interest Rate: The rate charged on the outstanding principal as interest

- Loan Tenure: The total duration of repayment

- EMI Amount: The amount you will repay every month

- Principal Component: The part of EMI that goes toward paying off the loan principal

- Interest Component: The part of EMI that goes toward paying off the interest charged on the principal

- Payment Number: The sequence of payments (Month 1, 2, 3…)

- Due Dates: The scheduled payment dates

- Outstanding Balance: The remaining loan amount after every payment

Get quick funds without any hassle—check out our Instant Loan App today!

How Is Your Personal Loan Repayment Schedule Calculated?

The personal loan repayment schedule calculation is pretty simple. Consider this example:

Suppose you take a loan of ₹5 lakhs for 12 months at an interest rate of 12% p.a. To create your loan repayment schedule, your lender will first ascertain your monthly EMI using the following formula:

EMI = [P × r × (1+r)^n] ÷ [(1+r)^n – 1]

Where:

- P = Principal loan amount

- r = Monthly interest rate (annual rate ÷ 12 ÷ 100)

- n = Total number of monthly payments

As per our example:

- P = ₹5,00,000

- r = (12 ÷ 12 ÷ 100 ) = 0.01

- n = 12

After the calculation, our monthly EMI amount will be ≈ ₹44,470.

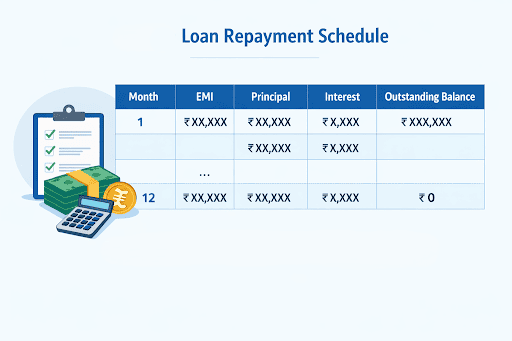

Based on this, your personal loan repayment schedule will look something like this:

| Month | EMI (₹) | Principal (₹) | Interest (₹) | Outstanding Balance (₹) |

| 1 | 44,470 | 39,470 | 5,000 | 4,60,530 |

| 2 | 44,470 | 39,865 | 4,605 | 4,20,665 |

| 3 | 44,470 | 40,264 | 4,206 | 3,80,401 |

| 4 | 44,470 | 40,667 | 3,803 | 3,39,734 |

| 5 | 44,470 | 41,073 | 3,397 | 2,98,661 |

| 6 | 44,470 | 41,482 | 2,988 | 2,57,179 |

| 7 | 44,470 | 41,894 | 2,576 | 2,15,285 |

| 8 | 44,470 | 42,310 | 2,160 | 1,72,975 |

| 9 | 44,470 | 42,728 | 1,742 | 1,30,247 |

| 10 | 44,470 | 43,150 | 1,320 | 87,097 |

| 11 | 44,470 | 43,574 | 896 | 43,523 |

| 12 | 44,470 | 43,523 | 947 | 0 |

Note:

- The interest rate is fixed, so the EMI remains constant throughout the loan tenure.

- In this example, the interest is calculated using the reducing balance method.

Factors Influencing Your EMI Amount

In the example above, we demonstrated how EMI is calculated. But do you know about the EMI amount factors that influence how much you pay every month? Here are the primary ones:

- Loan Amount: It’s self-explanatory—the higher your loan amount, the higher your monthly EMI.

- Loan Tenure: Your loan tenure decides how slowly or quickly you pay off the loan. Hence, a short tenure means bigger monthly EMIs, while a long tenure means smaller monthly EMIs.

- Interest Rate: Your personal loan interest rate has a direct impact on your EMIs. A high interest rate means high EMIs, whereas a low interest rate means lower EMIs. Moreover, if the lender charges interest on a floating rate basis, the EMI will change each time the rate fluctuates.

- Additional Charges: If your loan includes processing fees, GST, or other costs, they will raise your EMI.

Manage your financial obligations effortlessly—use our Personal Loan EMI Calculator for free!

Types of Repayment Schedules

Three types of personal loan repayment options commonly exist in India. They define the different ways personal loans are scheduled for repayment:

1. Standard Fixed EMI Schedule

Under the standard EMI structure, the borrower pays a fixed amount every month. The EMI includes both principal and interest and is calculated using the reducing balance method. This means interest is charged only on the outstanding principal each month, so the interest portion of the EMI decreases over time while the principal portion increases.

2. Step-Up EMI Schedule

Under the step-up schedule, EMI payments increase at predefined time periods during the loan tenure. The initial EMIs are lower and then increase.

3. Flexible EMI Schedule

As the name suggests, the flexible repayment schedule lets borrowers modify their repayment terms during the loan tenure, subject to the lender’s approval. They may adjust their EMI amount, tenure length, etc.

Also Read: What Does Emi Mean?

Benefits of a Well-Planned Repayment Schedule

There are various short-term benefits of a loan repayment plan. But here are two ways in which it helps you in the long run:

Budgeting and Financial Stability

In India, people spend nearly 33% of their monthly income on EMI. A structured repayment schedule helps in personal loan budgeting by enabling you to track and manage all your monthly EMI obligations effectively.

Improving Your Credit Score

A well-thought-out loan repayment schedule significantly reduces the chances of EMI defaults. And timely EMI payments help with credit score improvement.

Managing Your Personal Loan Repayment Effectively

Acquainted with the benefits? Now, here are some personal loan tips you can use to manage your personal loan repayment efficiently:

- Enable auto-debit to avoid missing out on EMIs

- Select the tenure that best suits your cash flow

- Avoid having multiple active loan accounts

- Consider personal loan prepayment or loan foreclosure to reduce your total interest burden

- Always track your outstanding loan balance to understand how much principal is due

Borrow Responsibly, Repay Confidently

Understanding your repayment schedule helps you borrow with confidence. From how your EMI is worked out to choosing the right loan period, everything affects how much you pay and how easy it is to manage your loan. When you choose the right schedule, your payments will fit your income and your financial goals.

A well-planned Hero FinCorp personal loan can be a step toward true financial empowerment, giving you access to funds while keeping repayment predictable and manageable.

Apply for a Hero FinCorp personal loan today and take the next step with confidence!

Frequently Asked Questions (FAQs)

Can I change my personal loan repayment schedule?

Yes. You can change your personal loan repayment schedule if your lender allows it.

What is the minimum and maximum tenure for a personal loan?

Personal loan repayment tenures are short, typically between 12 to 36 months.

Are there any charges for prepaying my personal loan?

Yes. Some lenders may charge a prepayment or foreclosure fee if you close the loan account early.

How can I access my personal loan repayment schedule document?

You can access your personal loan repayment schedule through your lender’s online portal or mobile app by logging into your account. It is usually available under the loan details or statements section.

Does a longer repayment tenure mean higher interest paid overall?

Yes. Typically, a longer repayment tenure means you have to pay higher interest overall.

What is the difference between principal and interest in an EMI?

Principal is the original loan amount you borrow. Interest is the cost you pay to the lender for borrowing that amount. In an EMI, one part goes toward repaying the principal, while the other covers the interest charged on the outstanding loan balance.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision...

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.