What is UPI and How Does UPI Work?

Key Takeaways

- UPI enables instant bank-to-bank transfers using a UPI ID or QR code.

- It works 24×7, including weekends and holidays.

- Users can pay without sharing account numbers or IFSC codes.

- Every transaction is secured with a UPI PIN and two-factor authentication.

- One UPI app can manage multiple bank accounts.

- UPI is free, fast, and widely accepted across India.

Picture this: you’re sipping tea at a roadside stall. It’s time to pay. You grab your phone, scan a QR code, and ka-ching. The payment is settled within minutes. Now imagine you’re in the queue for the next iPhone. When it’s your time to pay, you repeat the action. Scan and pay.

No cash, no card, just a quick UPI payment. That’s how common it’s become in India. From street vendors to large retailers, Unified Payments Interface (UPI) has changed the way we pay. It’s fast, safe, and built for modern, digital India.

What Is UPI?

UPI (Unified Payments Interface) is a real-time, mobile-first payment system that lets users transfer money instantly between any two Indian bank accounts using a Virtual Payment Address (VPA) without sharing bank account numbers or IFSC codes. It was developed and launched by the National Payments Corporation of India (NPCI) in April 2016, under Reserve Bank of India regulation.

Key facts about UPI:

- Full form: Unified Payments Interface

- Operator: NPCI (a non-profit set up by RBI and the Indian Banks Association)

- Regulator: Reserve Bank of India

- Launch year: 2016

- Active monthly users (2025): Over 491 million

- Participating banks: 675+ banks across public-sector, private, cooperative, payments, and regional rural banks

What problem UPI solves for daily payments:

- Removes the need to remember account numbers, IFSC codes, or branch names

- Removes the dependency on cards, card readers, and POS hardware for merchants

- Removes the 2-step authentication friction of net banking

- Works 24×7 including weekends and bank holidays - unlike older payment rails that historically had banking-hour windows

Also Read: UPI Mandate Meaning

Key Features and Benefits of UPI : Why It Became India's Preferred Payment Method

UPI's combination of speed, security, and zero cost is the reason it overtook cards, wallets, and net banking to become India's most-used digital payment rail.

Core features and benefits:

- Instant transfers: Money moves between any two banks in seconds, regardless of time or amount (within UPI limits)

- 24×7 availability: Works every day including weekends, holidays, and outside banking hours

- Interoperability: Any UPI app works with any UPI-enabled bank, no app lock-in

- Two-factor security: Device binding + UPI PIN authentication on every transaction

- No transaction fees: P2P and most P2M payments are free for the user under current government policy

- Single-app multi-account management: One UPI app can handle multiple bank accounts (savings, current, salary)

- Merchant-friendly: Businesses receive instant credit with no hardware, no POS setup, no MDR (under zero-MDR policy)

Also Read: Using Two Bank Accounts with One Mobile Number for UPI

How UPI Compares with Net Banking, NEFT, RTGS, and IMPS

UPI is one of several digital payment rails in India. The right choice depends on amount, urgency, and the user's comfort with the channel.

UPI vs Net Banking: easier for first-time digital payment users?

UPI is significantly easier for first-timers because:

- No login flow - UPI uses a PIN at transaction time, not a session-based username and password

- No beneficiary registration - UPI uses a VPA directly; net banking requires adding the beneficiary and waiting 30 minutes

- Mobile-native - UPI is designed for smartphone use; net banking is web-first and clunky on small screens

- Instant - UPI settles in seconds, 24×7; net banking transfers via NEFT/RTGS settle in batches

UPI vs NEFT, RTGS, and IMPS: when to use what:

- UPI - for amounts up to Rs 1 lakh (standard) or up to Rs 5 lakh for select categories. Settles in seconds, 24×7. Free for the user.

- IMPS - for Rs 1 lakh to Rs 5 lakh single transfers where UPI's standard cap is exhausted. Settles in seconds, 24×7. May attract a small fee (Rs 2.50–Rs 25).

- NEFT - for any amount with no upper cap; settles in 30-minute batches, 24×7. Free or low fee at most banks.

- RTGS - for transfers above Rs 2 lakh that need same-day high-value settlement; works 24×7 since 2020. Used primarily for business and corporate transfers.

Quick decision rule: Use UPI for everyday payments and amounts under Rs 1 lakh; switch to IMPS or NEFT only when the amount exceeds UPI's cap or when the recipient's UPI ID isn't available.

What Is a UPI PIN and How to Set It?

Your UPI PIN is a 4- or 6-digit secret code used to authorise every transaction. Think of it as your personal digital signature. Unlike an MPIN, which is used for mobile banking, this PIN is specific to your UPI app and linked bank account.

Here’s how to set or reset your UPI PIN:

- Open your UPI app and go to “Bank Account” or “Set PIN”

- Select your bank. The app will verify your linked number via SMS

- Enter the last six digits of your debit card and expiry date

- Set your desired PIN and confirm

Done! You can now make secure payments.

Short on cash? Get instant funds - download our Instant Loan App and apply for your loan today!

Read Also: A Simple Guide to Scanning and Paying with QR Codes via Mobile Banking

Understanding UPI ID, UPI Number, and UPI Address

UPI ID, address, or number is like your digital identifier. It allows people to send or receive money without needing your bank details.

- Your UPI ID, also known as a VPA, is your unique digital identity, such as name@bankname.

- UPI address is just another term for your VPA.

- A UPI number, usually your mobile number. It can also act as a payment identifier if linked to your bank.

They all serve the same purpose: to simplify payments and keep your account information private.

Also Read: What is a UPI Address? Meaning and How It Works

How Does UPI Payment Work? Step-by-Step Process

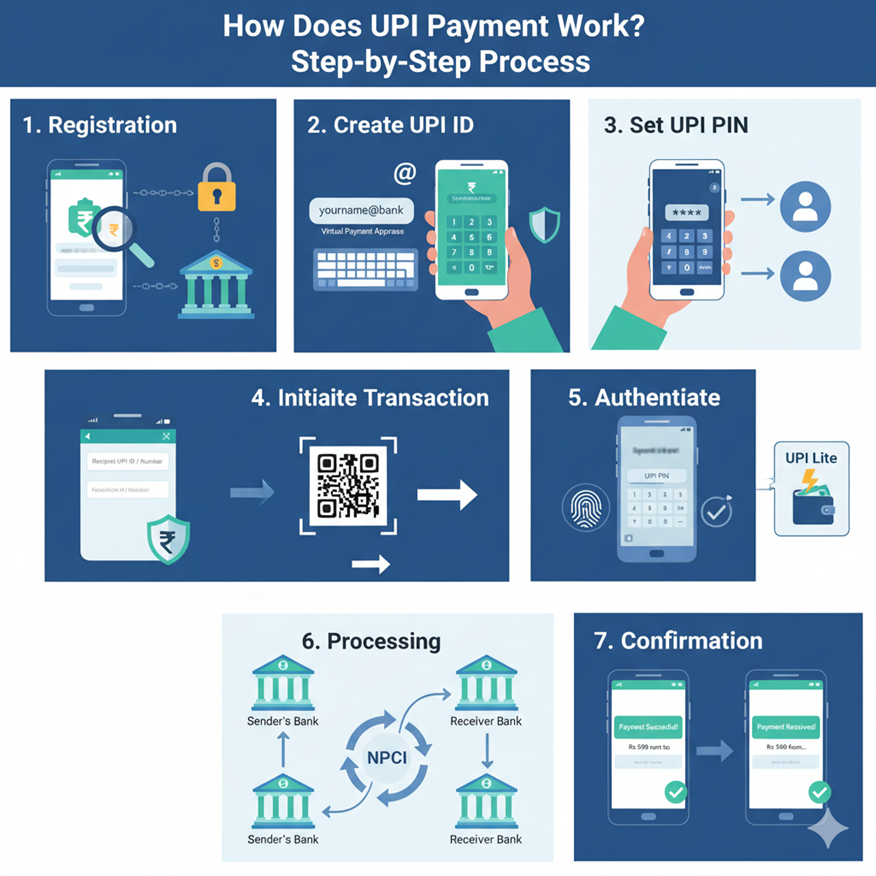

Here’s a simple breakdown of how UPI payment works:

- Registration: Download a UPI app and link your bank account

- Create UPI ID: Generate your unique VPA

- Set UPI PIN: Create your secure code for authorising transactions

- Initiate Transaction: Enter the recipient’s UPI ID, number, or scan their QR code

- Authenticate: Verify the payment by entering your UPI PIN

- Processing: The app connects both banks via NPCI for real-time transfer. For small transactions, UPI Lite allows instant payments without fully going through the bank

- Confirmation: You and the receiver get instant notifications once the payment is successful

Also Read: UPI Daily Transaction Limit

How to Transfer Money Using UPI (Step-by-Step)

Sending money through UPI is quick once your bank account is linked and set up on a UPI-enabled app. Follow these simple steps to complete a transfer securely:

- Download a UPI-enabled app

- Set up your UPI ID by following the app’s instructions

- Add and verify your bank account using OTP

- Select the recipient or enter their UPI ID or bank details

- Enter the amount and add remarks if needed

- Confirm and authorise the payment using your UPI PIN

The amount is transferred instantly to the recipient’s bank account once the transaction is completed.

What are the Benefits of UPI for Merchants

Understanding how UPI helps merchants unlock faster, low-cost digital payments. Here are key benefits:

- Instant Settlements: Receive payments in real time, improving cash flow.

- Low Transaction Cost: Minimal or zero MDR makes it cost-effective.

- Easy Integration: Works with QR codes, apps, and POS systems.

- 24/7 Availability: Accept payments anytime, even on holidays.

- Secure Transactions: Multi-layer authentication reduces fraud risks.

- Better Customer Experience: Quick, hassle-free checkout boosts sales.

What are the Benefits of UPI for Customers

Understanding what UPI is reveals why it’s transforming digital payments for users:

- Instant Transfers: Send and receive money in real time, 24/7.

- Easy to Use: Pay via mobile number, QR code, or UPI ID.

- No Extra Charges: Most UPI transactions are free for customers.

- Secure Payments: Protected with PIN authentication and bank-grade security.

- All-in-One Solution: Manage bill payments, recharges, and shopping in one place.

- Wide Acceptance: Accepted across merchants, apps, and platforms in India.

Wrapping Up

UPI is a financial revolution, positioning India as a leader in the global digital finance movement. New features like UPI AutoPay, UPI Lite, and even international UPI payments are only making it better. It’s surely an exciting time to be at the centre of all the action.

Want to make payments without touching your savings? Go for a personal loan by Hero FinCorp.

We not only offer quick and hassle-free disbursal but also flexible repayment options tailored to your needs, helping you manage your finances with ease and confidence. So why wait? Explore our range of options and apply for a loan today!

Frequently Asked Questions

How are a UPI ID and a UPI number different?

Your UPI ID is your Virtual Payment Address (like name@bank). On the other hand, your UPI number is your mobile number linked to the account.

Can I use UPI without a smartphone?

Yes. UPI 123Pay (launched 2022) lets feature-phone users make UPI transactions through IVR, missed-call dial-ups, sound-based proximity payments, and app-based payments on basic phones without needing a smartphone or internet connection.

What if I forget my UPI PIN?

Instantly reset your UPI PIN from your UPI app with the updated card details.

Is UPI safe for online shopping?

Yes. UPI is protected by multi-level authentication and encrypted transactions.

Can I link multiple bank accounts to a single UPI ID?

Typically, one UPI ID maps to one primary bank account within a UPI app. To use multiple bank accounts, create separate UPI IDs (one per account) within the same app and switch between them when transacting.

What is the full form of UPI?

The full form of UPI is Unified Payments Interface, a system built by NPCI enabling instant digital bank transfers across India.

Who launched UPI in India?

UPI was launched in April before 2016 by the National Payments Corporation of India to promote digital payments nationwide.

What is the main purpose of UPI?

The main purpose of UPI is to simplify fast, secure, and seamless digital transactions without sharing bank details.

Is UPI available 24/7?

Yes, UPI is available 24/7, enabling users to send and receive money anytime, including weekends and holidays.

Is there a transaction fee for UPI payments?

No. UPI transactions are free of cost for users under the current government policy. Merchants also pay no MDR on UPI transactions under the zero-MDR framework.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.