Personal Loan Insurance: Everything You Should Know

Personal loans provide easy access to money, whether you're financing a big buy or organising your ideal holiday. However, many borrowers ignore a crucial add-on: personal loan insurance, while concentrating on interest rates and EMIs.

Having personal loan coverage allows you to continue making loan repayments in times of need. In addition, it helps you maintain your credit score during financial emergencies. Read on to learn more about personal loan insurance, how it works, its benefits, drawbacks and more.

What Is Personal Loan Insurance?

Personal loan insurance (also known as a payment protection plan) is a specific insurance policy that protects borrowers’ interests when they are unable to repay the loan.

These events may include:

- Death

- Permanent or temporary disability

- Involuntary job loss

In such situations, the insurance policy helps cover the outstanding loan amount, either partially or fully, based on the policy terms.

How Does Personal Loan Insurance Work?

There are many similarities between a personal loan insurance plan and other insurance policy plans on the market. You have the option to pay the premium in instalments or as a single sum, depending on your needs.

Depending on the conditions of your policy, the insurer will either totally or partially repay your remaining loan when you choose this add-on. This ensures your family or co-borrower isn’t burdened with repayment during emergencies.

Let’s understand this with an example:

You choose to get personal loan insurance, with the cost added to your EMIs, and take out a five-year personal loan of ₹5 lakh.

In order to prevent defaults and save your credit score, the insurer might pay your EMIs for a set amount of time (say, six months) if you leave your job two years later. In case of permanent disability or death, the policy can settle the outstanding loan amount, easing the financial burden on your family.

Is Personal Loan Insurance Mandatory in India?

No. Personal loan insurance is not legally mandatory in India. Although several banks and NBFCs may recommend or bundle it to safeguard loan repayment in case of situations such as job loss, disability, or death, borrowers are not required by law to buy it.

Many customers assume it's mandatory to have personal loan insurance because lenders often include it in loan packages or add the premium to the loan amount. But you can accept, decline, or choose another insurer.

Here are some of the other important things to consider:

- Always review loan documents to ensure no unwanted insurance charges are added

- Lenders push personal loan insurance as it reduces their repayment risk and protects borrowers during emergencies

- You are free to decline it before signing the agreement and rejecting personal loan insurance will not affect your loan approval

Having said this, please keep in mind that having personal loan insurance is useful as it offers financial protection for your family in unpredictable situations.

Also Read: What is a Personal Loan?

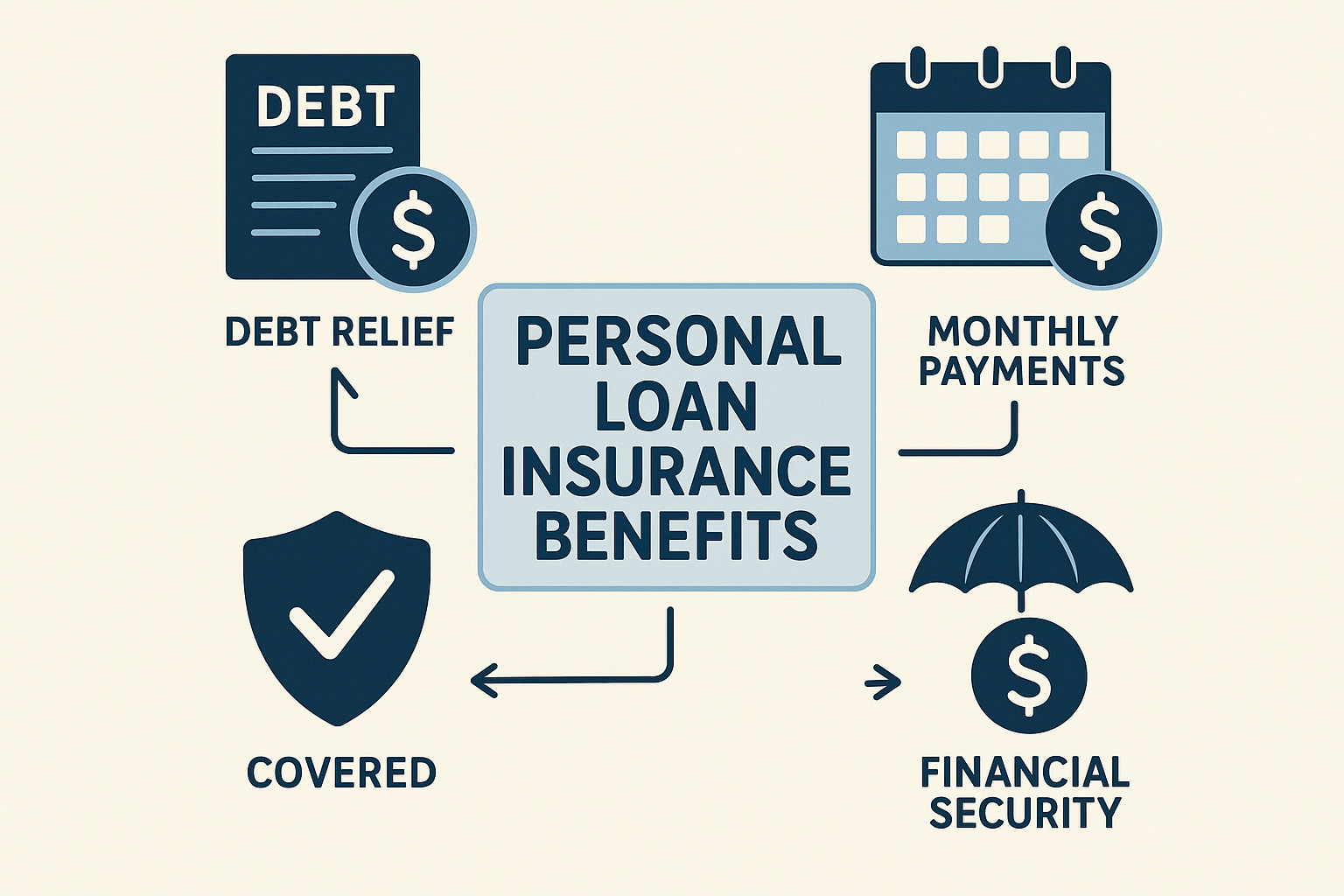

Benefits of Personal Loan Insurance

There are several benefits of personal loan insurance, such as:

Credit Score Protection

The policy helps you prevent defaults, late fines, and penalties by guaranteeing the insurer makes loan payments on schedule. This keeps your credit score from dropping. To get future credit at favourable rates, you must have a solid credit history.

Family Protection

In the unfortunate event of death or permanent disability, the personal loan insurance policy can cover the remaining loan balance. This can prevent your family or dependents from being burdened with the unwanted debt.

Income Security

For events such as involuntary unemployment or temporary disability, some policies offer an income stream to cover your monthly EMIs for a specified period (e.g., 3 to 12 months), giving you time to recover or find new employment.

Tax Advantage

In some cases, premiums paid for personal loan insurance may give you the advantage of tax deductions under relevant tax laws.

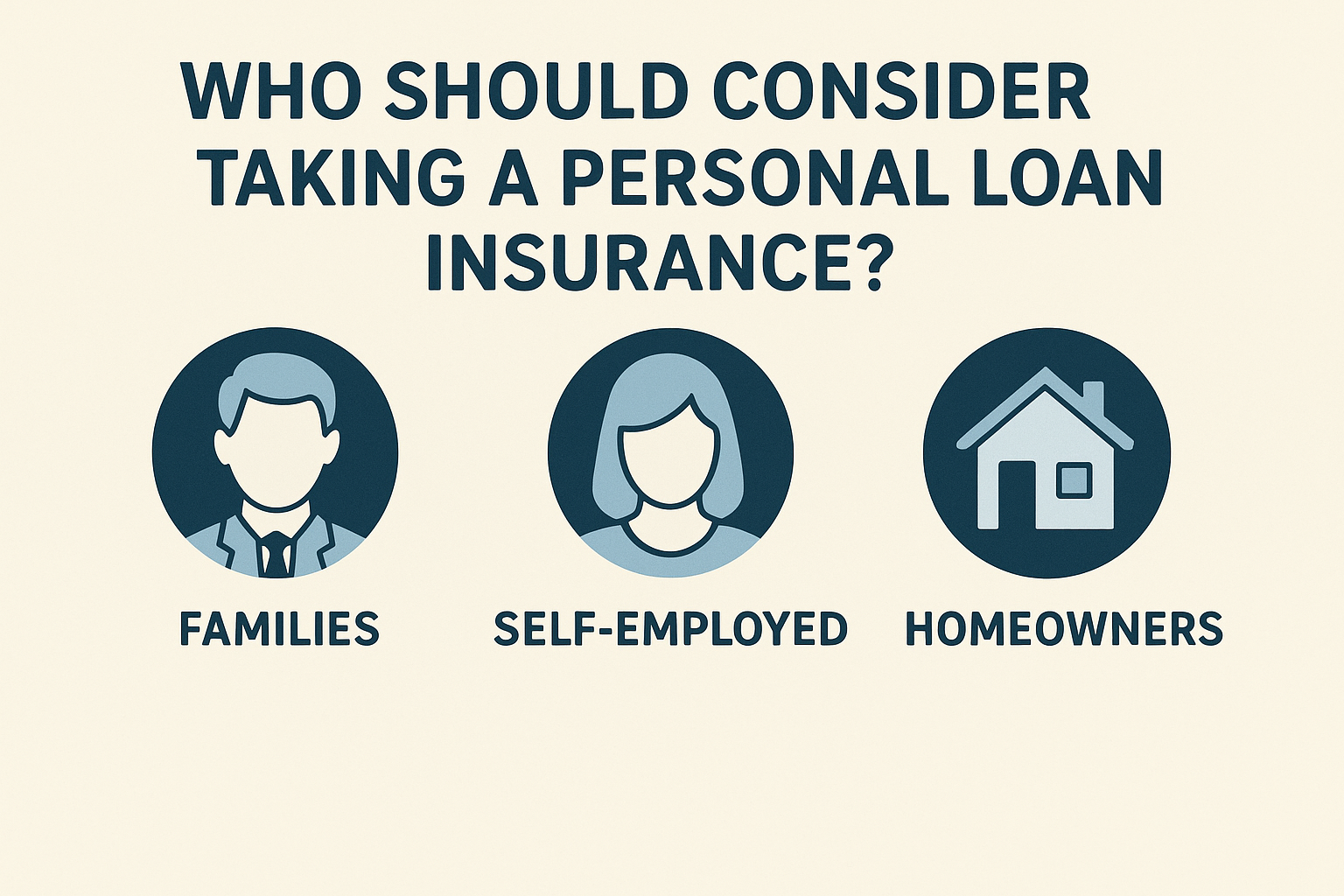

Who Should Consider Personal Loan Insurance?

You should consider personal loan insurance if you're the sole earner, have an unstable job, are self-employed, or have existing health risks.

Here are the details of some of the key candidates for personal loan insurance:

- Self-Employed Professionals: The fluctuations in income can be covered during lean periods.

- Primary Income Earners: If your family relies solely on your income, this ensures they aren't burdened with debt if you can't work.

- People with Unstable Jobs: If your industry faces frequent layoffs or your income is irregular (e.g., gig workers, contract jobs), having personal loan insurance offers a safety net.

- Borrowers with Health Risks: For a borrower with pre-existing conditions, it protects payments in case illness prevents you from working.

- People with Limited Savings: A personal loan insurance coverage offers a safety net in the event that unanticipated events leave you without funds.

Drawbacks and Limitations of Personal Loan Insurance

While there are several benefits, personal loan insurance also comes with many drawbacks that borrowers should consider.

Some of the disadvantages of personal loan insurance are discussed below:

- High Premiums: Premiums for personal loan insurance are generally on the higher side

- Restricted Coverage: Provide restricted protection, excluding coverage for certain crucial situations and pre-existing medical conditions.

- Redundant Protection: If borrowers already have life, health, or disability insurance, they can end up with redundant coverage.

Secure Your Finances and Apply Smarter

Personal loan insurance serves as a smart safety net to safeguard you from financial burden during unexpected emergencies.

If you are also looking to get a personal loan to cover your financial needs, we've got you covered. At Hero FinCorp, you can apply for a personal loan through a simple, digital process designed to offer quick access to funds with transparency and ease.

So why wait? Explore our loan options and borrow with confidence now!

Frequently Asked Questions

Is personal loan insurance compulsory for all personal loans in India?

No, personal loan insurance is not mandatory for all personal loans in India.

Can I cancel my personal loan insurance once I've taken out the loan?

Yes, in most cases, you can opt out of personal loan insurance after taking the loan.

Does personal loan insurance cover pre-existing medical conditions?

Personal loan insurance coverage usually does not cover pre-existing medical conditions.

Are pre-existing medical issues covered by personal loan insurance?

Pre-existing medical issues are typically not covered by personal loan insurance policies.

How long does it take to settle an insurance claim?

The resolution of a personal loan insurance claim often takes ten to thirty days.

Is it possible to make many claims on personal loan insurance over the course of the loan?

It is contingent upon the particular coverage type and the policy's terms and conditions.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.