Outstanding Loan Amount: Meaning & How to Find Out?

- What is Outstanding Amount in Loan?

- Components of Outstanding Loan Amount

- How to Check Outstanding Loan Amount

- Difference Between Outstanding Amount and Remaining Balance

- How Outstanding Loan Amount Has a Financial and Credit Score Impact

- How to Reduce Outstanding Loan Amount Effectively

- Frequently Asked Questions

Rahul, based in Pune, has been repaying his personal loan EMIs for almost two years now.

However, while making plans to repay the outstanding loan amount using his annual bonus, Rahul found himself unable to determine what is outstanding amount in loan.

It is simple to learn how to check the outstanding loan amount. This information will help you make decisions regarding payments, prepayments, and financial planning in general.

What is Outstanding Amount in Loan?

Outstanding loan amount meaning is defined as the amount that remains unpaid on your loan. It consists of the unpaid principal, interest, and other charges, calculated according to your loan schedule.

Here is an example:

Rahul takes a personal loan of₹3,00,000 from Hero FinCorp. Here are the loan details:

- Term - 5 years

- Interest Rate - 18%

- Monthly EMI - ₹7,620

Here are the outstanding loan amount details after Rahul has paid EMIs for 12 months:

| Component | Amount (₹) |

| Original Loan Amount | 3,00,000 |

| Total EMIs Paid in 12 Months | 91,440 |

| Portion Paid Towards Interest | 51,950 |

| Portion Paid Towards Principal | 39,490 |

| Outstanding Principal Balance | 2,60,510 |

Even after paying ₹91,440 in EMIs, the principal amount remains at about ₹39,490. The remaining ₹51,950 has gone towards interest payments.

As a result, your outstanding loan amount after one year is still about ₹2.61 lakh.

Also Read: What is Loan Amortization and How It Works?

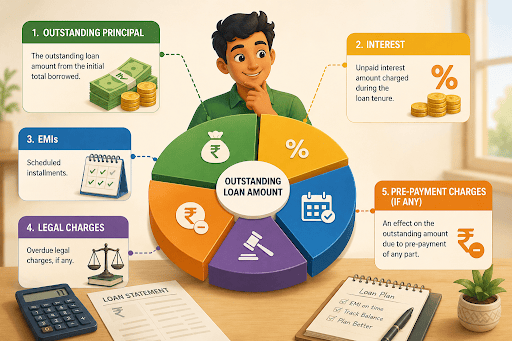

Components of Outstanding Loan Amount

The components of an outstanding amount in loans are:

- Outstanding Principal - The outstanding loan amount from the initial total borrowed.

- Interest - Unpaid interest amount charged during the loan tenure.

- EMIs - Scheduled installments.

- Legal Charges - Overdue legal charges, if any.

- Pre-payment Charges (if any) - An effect on the outstanding amount due to pre-payment of any part.

Also Read: What is Personal Loan Prepayment & How is it Calculated?

How to Check Outstanding Loan Amount

Here are various methods to check the outstanding loan amount:

Method 1 - Using the Hero FinCorp Digital Lending App

Step 1 - Access your account using the app - Android/iOS

Step 2 - Go to your active loan information.

Step 3 - Find your loan summary.

Step 4 - Get your loan balance details.

Method 2 - Using Your Online Loan Account

Step 1 - Access the lender's customer portal page.

Step 2- Log in to your account.

Step 3 - Access your loan dashboard.

Step 4 - Go through your loan balance details.

Step 5 - Review Your Loan Account Statement

Method 3 – Check Your Account Statement

Your account statement has the following information:

- Outstanding principal

- Interest information

- History of EMI

- Remaining loan term

Method 4 - Reach Out to Customer Support Services

You can approach the lender’s customer support and ask for your latest outstanding loan amount.

Method 5 - Visit the Bank's Branch

Customers can visit their nearest bank branch to check the outstanding loan amount.

Also Read: Can I prepay my personal Loan without any extra charges?

Difference Between Outstanding Amount and Remaining Balance

Though these terms can be used synonymously, knowing this difference makes it easier to understand the outstanding loan amount meaning.

| Parameter | Outstanding Amount | Remaining Balance |

| Meaning | Total amount currently owed | The principal amount that still needs to be paid |

| Includes Interest | Yes | Principal-focused |

| Includes Charges | May include | May not include |

| Changes Over Time | Updates regularly | Reduces as the principal amount is repaid |

| Used For | Foreclosure and repayment planning | Loan tracking |

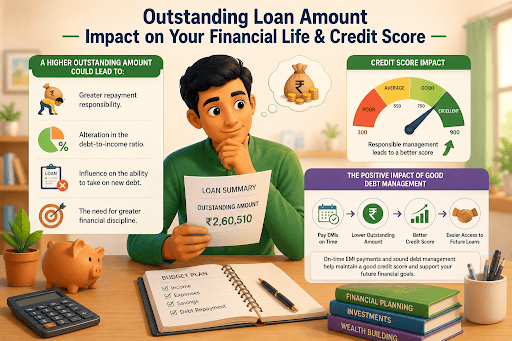

How Outstanding Loan Amount Has a Financial and Credit Score Impact

The outstanding loan amount is a significant aspect of one’s overall financial situation.

A higher outstanding amount could lead to:

- Greater repayment responsibility.

- Alteration in the debt-to-income ratio.

- Influence on the ability to take on new debt.

- The need for greater financial discipline.

On-time EMI payments and sound debt management can help borrowers maintain a good credit score. This can be useful if they plan any prepayment or future financial activity.

Also Read: What Is Personal Financial Management (PFM)? Definition, Full Form, Tools and Apps

How to Reduce Outstanding Loan Amount Effectively

Here are some effective ways to lower your outstanding loan balance:

- Pay EMI On Time - Consistent repayments help you keep up with the decrease in your loan balance.

- Go for Part Prepayment - Part prepayments can effectively reduce your outstanding principal.

- No Delay In Repayment - Delaying repayments might cost you more with extra fees and increase the total amount of repayment due.

- Monitor Loan Statements Periodically - Keep track of your loan balance to take action and make faster repayments.

- Consider Foreclosure If Possible - Foreclosure is another way to lower your outstanding balance.

Looking for money to finance your plans? Check your eligibility for a personal loan using Hero FinCorp's Instant Personal Loan journey.

Frequently Asked Questions

How is the outstanding loan amount different from EMI?

EMI is the periodic monthly payment towards your loan. The outstanding loan amount is the total amount still owed.

How often is the outstanding loan amount updated?

The outstanding loan amount is updated after EMI payments or prepayments.

Does the outstanding loan amount increase once the loan is disbursed?

Yes, as there may be interest accrued on it. Applicable interest accruals, charges, or penalties (if any) may also affect the outstanding amount.

Will paying the loan ahead of time lower the loan balance?

Any prepayment can lower the outstanding loan balance.

How can I find my loan balance offline?

You can contact customer service or visit a nearby branch to check the outstanding loan amount.

Does the outstanding loan balance include penalties and fees?

Based on the lender's calculation method, the outstanding loan amount might include applicable penalties or fees.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.