NBFC vs Bank: 7 Key Differences & Which is Better for Your Personal Loan?

- What are NBFCs?

- What are Banks?

- Key Differences Between NBFCs and Banks

- Advantages of Choosing NBFCs for Personal Loan

- Advantages of Choosing Banks for Personal Loan

- NBFC vs Bank: Which is Best for a Personal Loan?

- Conclusion

- Frequently Asked Questions

- What Is The Main Difference Between a Bank and an NBFC?

- Is It Safe To Take A Loan From An NBFC?

- Which Is Better for a Personal Loan: Bank or NBFC?

- Why Do NBFCs Charge Higher Interest Rates Than Banks?

- Can an NBFC Issue A Credit Card?

- Does an NBFC Check My Cibil Score?

- Can I Deposit My Salary Into An NBFC Account?

- Why Is Loan Processing Faster In NBFCs Than in Banks?

When we think about funds, the first thing that comes to mind is usually a bank. But did you know there’s another type of financial institution that provides similar services and still helps millions with loans? These are Non-Banking Financial Companies (NBFCs). While both provide financial services, the difference between bank and NBFCs lies in their licensing, regulatory framework, and ability to accept deposits. Knowing the NBFCs vs Bank difference in India under the regulatory landscape can help you choose the right partner for your financial needs.

What are NBFCs?

An NBFC is a company registered under the Companies Act, 1956 or 2013 and regulated by the Reserve Bank of India (RBI) under Chapter III-B of the RBI Act, 1934. Unlike banks, NBFCs do not hold a banking license but are granted a Certificate of Registration (CoR) to conduct specific financial activities. Their primary functions include lending, offering fixed deposits, and distributing insurance.

What are Banks?

Banks are financial institutions governed by the Banking Regulation Act, 1949. They work as intermediaries. They accept demand deposits like savings and current accounts, and they provide loans to individuals and businesses.

In India, the difference between banks and NBFCs is quite clear. Banks are a key part of the country’s payment and settlement system. This means they can issue cheques and handle direct clearing of payments.

Key Differences Between NBFCs and Banks

The differences between banks and NBFCs become clearer when we compare their structure, roles, and how they operate in the financial system.

| Feature | Banks | NBFCs |

|---|---|---|

| Regulation | Regulated under the Banking Regulation Act, 1949. | Registered under the Companies Act, 1956/2013. |

| Deposits | Can accept demand deposits (Savings/Current accounts). | Cannot accept demand deposits; only specific NBFCs can accept term deposits. |

| Payment System | Part of the payment/settlement system (can issue cheques). | Not part of the payment system; cannot issue cheques. |

| Deposit Insurance | Deposits are insured up to Rs 5 Lakh by DICGC. | No deposit insurance is available for investors. |

| Reserve Ratios | Must maintain CRR (Cash Reserve) and SLR (Statutory Liquidity). | Not required to maintain CRR or SLR. |

| Foreign Investment | Capped at 74% for private sector banks. | Allowed up to 100% (Automatic route). |

Advantages of Choosing NBFCs for Personal Loan

Non-Banking Financial Companies have made Personal Loans more accessible by providing credit to people who may not meet traditional bank requirements.

- Faster Processing and Disbursement: Many NBFCs offer instant approval and disburse the amount into your account within 24 to 48 hours.

- Flexible Credit Criteria: NBFCs consider borrowers with a "medium" credit score or those who are first-time borrowers without an extensive credit history.

- Minimal and Digital Documentation: Most NBFCs offer an entirely paperless journey. You can simply upload your KYC documents and bank statements via an app, eliminating the need to visit a branch or submit physical copies.

- Customised Loan Products: NBFCs often design loans for specific needs such as Travel Loans, wedding loans, or even small-ticket "Bridge Loans".

- Competitive Interest for Good Profiles: While their base rates can be higher, NBFCs often offer competitive rates for personal loans with stable jobs and clean repayment records.

Advantages of Choosing Banks for Personal Loan

Traditional banks remain the preferred choice for borrowers who prioritise long-term savings and structured reliability.

- Lower Interest Rates: This is the most significant advantage. Since banks have access to low-cost funds from savings and current accounts, they can offer Personal Loans at interest rates at lower interest rates.

- Transparent Fee Structure: Banks operate under stringent RBI guidelines regarding "hidden charges." You are less likely to encounter unexpected processing fees, "administrative" costs, or high service charges.

- Higher Loan Amount: If you need a substantial amount (e.g., Rs 20 Lakh to Rs 40 Lakh), a bank is more likely to approve such a high limit based on your income.

- Benefit of Existing Relationships: If you already have a salary account or an FD with a bank, they might offer you pre-approved loans with zero documentation at a favourable interest rate.

- Customer Support: Banks offer a physical infrastructure. If you have a grievance or want to discuss a repayment issue, you can visit the local branch.

NBFC vs Bank: Which is Best for a Personal Loan?

When choosing between a bank and an NBFC for a Personal Loan, it depends on what matters most to you: speed, flexibility, or cost.

- Banks usually offer lower interest rates but have stricter eligibility criteria and longer processing times.

- NBFCs provide faster approvals, more flexible loan options, and easier access for people with less conventional credit histories, though interest rates may be slightly higher.

If you need quick access to funds or don’t fit traditional lending criteria, an NBFC may be more suitable. If you can meet stricter requirements and want lower costs, a bank could be a better choice.

Conclusion

The difference between a bank and an NBFC comes down to their structure, regulation, and the way they handle money. Both banks and NBFCs have their own advantages when it comes to Personal Loans. Banks are reliable, offer lower interest rates, and provide the security of deposit insurance, but they can be slower and have stricter eligibility requirements. NBFCs, on the other hand, are faster, more flexible, and often reach borrowers who may not meet traditional criteria, though their interest rates can be higher and deposits are not insured.

Choosing the right option depends on your priorities, whether you value speed and flexibility or lower cost and added security. Understanding these key differences can help you make a smarter, more informed decision for your personal loan needs.

Frequently Asked Questions

What Is The Main Difference Between a Bank and an NBFC?

The main difference lies in their legal authority and role in the financial system. Banks can accept demand deposits, are part of the payment and settlement system, and offer deposit insurance. NBFCs cannot accept demand deposits (except certain term deposits), are not part of the payment system, and do not offer deposit insurance. NBFCs focus on specific financial services and are more flexible in lending.

Is It Safe To Take A Loan From An NBFC?

It is generally safe to take a loan from a regulated NBFC. All NBFCs are registered and regulated by the Reserve Bank of India. However, unlike banks, your deposits or advance payments are not insured, so always check the credibility and RBI registration of the NBFC before borrowing.

Which Is Better for a Personal Loan: Bank or NBFC?

To choose between banks and a Personal Loan depends on your needs:

- Banks: Lower interest rates, more secure, but stricter eligibility and slower processing.

- NBFCs: Faster approval, more flexible eligibility, easier for non-traditional borrowers, though rates may be higher.

Why Do NBFCs Charge Higher Interest Rates Than Banks?

NBFCs often lend to borrowers who do not meet the strict criteria of banks, which increases their risk. They also do not get low-cost deposits like banks and cannot access the RBI’s liquidity support, so they charge higher interest to cover costs and risks.

Can an NBFC Issue A Credit Card?

NBFCs cannot issue credit cards. Only banks or entities authorised by the RBI can issue credit cards. NBFCs can, however, provide loans, EMI financing, and other credit products.

Does an NBFC Check My Cibil Score?

Yes, NBFCs check your CIBIL scores before approving a loan.

Can I Deposit My Salary Into An NBFC Account?

NBFCs cannot accept demand deposits like salaries. Only banks can receive salary credits in savings or current accounts. Certain NBFCs may accept term deposits, but these are fixed for a period.

Why Is Loan Processing Faster In NBFCs Than in Banks?

NBFCs often have simpler procedures. This allows them to approve loans quickly, sometimes within minutes, whereas banks follow more traditional, paperwork-heavy processes.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Taking a personal loan is the easy part. Managing the EMIs, month after month, is where the real work begins.

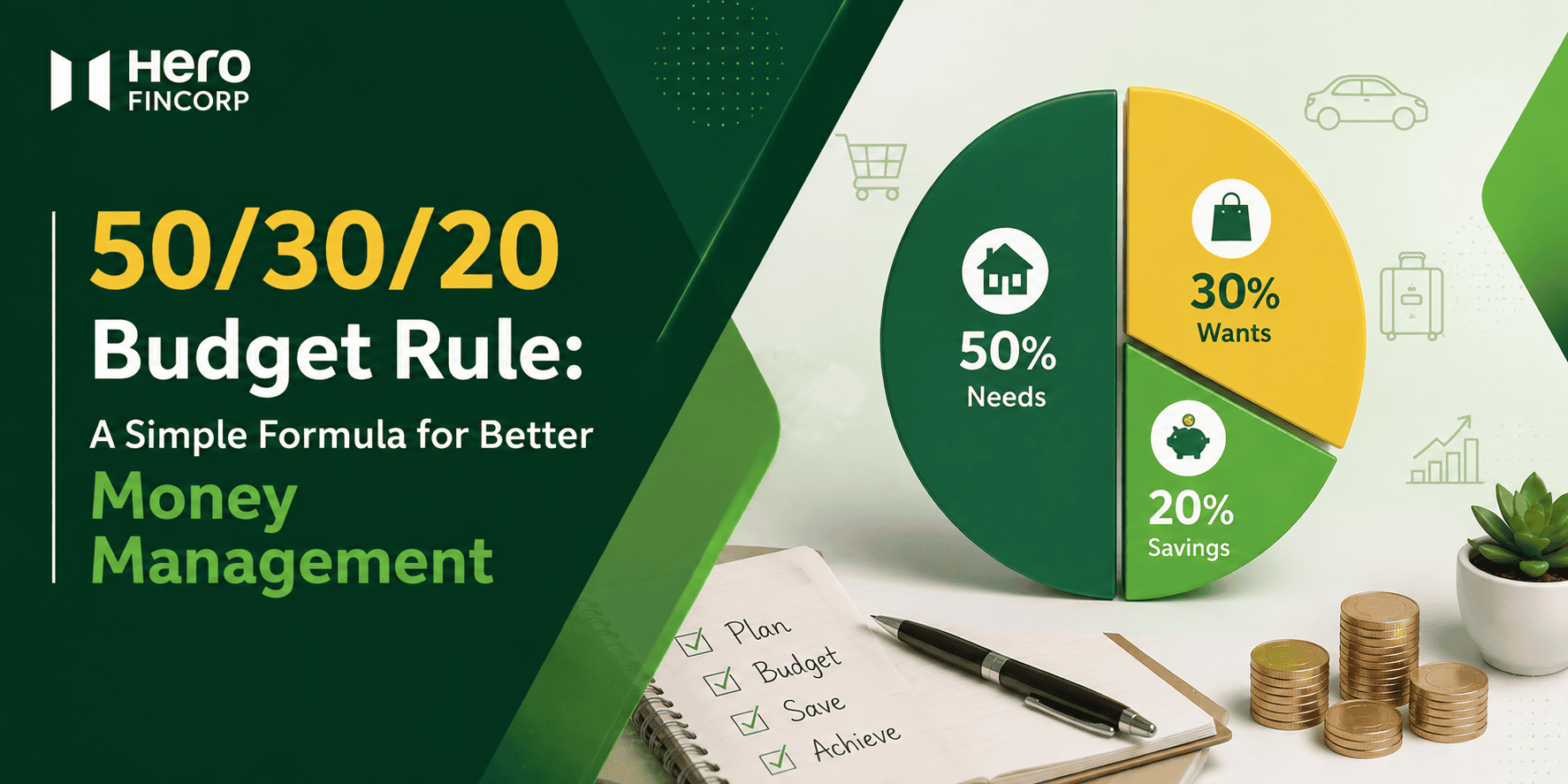

You look at your bank balance in the middle of the month. You think about where your salary went. This happens to a lot of people. The 50/30/20 budget rule is a way to stop feeling bad about how you spend your salary.

Every month, a slice of your salary vanishes into something called “PF”. It’s easy to treat it as just another deduction, but that deduction is quietly building your retirement corpus, tax-free. Understanding PF in salary, such as what it means, how it’s calculated, and when you can withdraw it, helps put you in charge of your long-term financial health. Let’s decode it without the jargon.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.