NBFC Personal Loan: Benefits, Online Process and Comparison with Banks

- What is an NBFC Personal Loan?

- Why NBFC Personal Loans Are Gaining Popularity

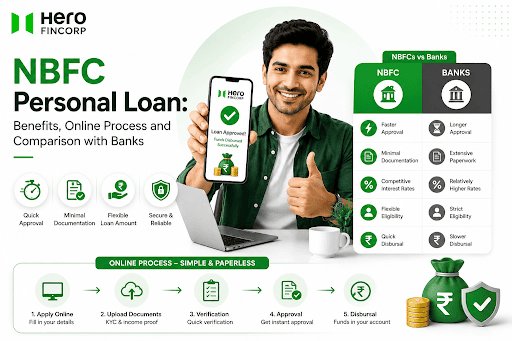

- Key Advantages of NBFC Personal Loans

- NBFC Personal Loan vs Bank Personal Loan: Detailed Comparison

- Features of NBFC Personal Loans

- NBFC Personal Loan Online: The Digital Application Process

- Choosing the Best NBFC for Personal Loans

- Hero FinCorp: A Leading NBFC for Personal Loans

- Frequently Asked Questions

Rohan, a salaried person earning Rs. 22,000 a month walks into a bank for a personal loan. Salary too low. CIBIL score 690. Application rejected before it even gets reviewed.

That same person applies to an NBFC online, uploads three documents, and has money in their account the next morning.

That gap is why personal loans have grown into something worth paying attention to.

India's lending market is heading toward $724.2 billion by 2025, with NBFCs driving a large portion of that growth by reaching borrowers banks consistently turned away. This is not a niche product anymore. Millions of Indians are using it as their first choice, not a backup plan.

What is an NBFC Personal Loan?

Most people know what a bank is. Fewer people can quickly explain what is an NBFC loan when it shows up on an app or a comparison site.

An NBFC, Non-Banking Financial Company, holds an RBI licence and can lend money but cannot accept deposits the way banks do. That difference matters because NBFCs are not sitting on public savings that need protecting through tight lending controls.

An NBFC personal loan is unsecured, needs no collateral, and suits salaried employees, self-employed professionals, freelancers, and gig workers who do not meet standard bank norms. Approval depends on income, credit history, and repayment capacity.

Why NBFC Personal Loans Are Gaining Popularity

Several things working together explain the shift toward NBFC personal loans. None of them are about marketing.

Flexible Eligibility Criteria

Most banks want applicants from listed companies, above a certain salary, with years of continuous employment. NBFCs read actual bank statements instead. A person earning Rs. 20,000 at a mid-sized company with consistent monthly credits in their account gets a fair look, not an automatic rejection.

Minimal Documentation Requirements

PAN, Aadhaar, salary slips, bank statements. Uploaded online. That is the whole list for most NBFCs. No attested copies, no passbook, no visit to a branch carrying a folder of documents.

Quick Approval and Instant Disbursal

NBFCs often disburse personal loans almost instantly, while certain banks can take days to release the amount. Automated systems read the application and generate an offer without a credit committee sitting down to review a file manually.

Lower Credit Score Requirements

Banks typically draw the line at a CIBIL score of 750. Many NBFCs approve loans for borrowers at 650 or above, though at a higher rate. People with thin credit files because they have never borrowed before also have a better shot here than at a bank.

Hassle-Free Online Process

Application, KYC, document upload, offer review, acceptance. All of it on one screen. No appointment, no branch, no callback that arrives three days after the urgent need has passed.

Key Advantages of NBFC Personal Loans

A few specific things make NBFC personal loan products practical in ways that matter day-to-day:

- No security or collateral needed regardless of loan amount

- Loan amounts tied to actual income, not a flat product ceiling

- Tenure choices from 12 to 36 months so monthly EMI stays manageable

- Flexi loan variants on some platforms where interest applies only to the amount drawn

- Pre-approved offers for repeat borrowers with clean repayment histories

NBFC Personal Loan vs Bank Personal Loan: Detailed Comparison

On paper both are unsecured personal loans. Getting one from an NBFC and getting one from a bank are genuinely different experiences once the application goes in.

| Factor | NBFC Personal Loan | Bank Personal Loan |

| Minimum CIBIL Score | 650 and above | Usually 750 and above |

| Processing Speed | Often within 24 hours | Several days |

| Documentation | Minimal, fully digital | More extensive |

| Interest Rate | 12% to 24% per annum | Lower for strong credit profiles |

| Who Qualifies | Broader, includes gig workers | Stricter income and employment norms |

| Branch Visit | Not required | Sometimes required |

| Collateral | None | None |

Borrowers with a 780 CIBIL score at a large firm might get a better rate at a bank. Most other borrowers tend to get a faster, easier outcome through an NBFC.

Features of NBFC Personal Loans

Loan Amount and Limits

Most NBFCs offer personal loans from Rs. 50,000 to Rs. 55 lakh. The number on the offer letter depends on monthly income, existing EMI load, and employer type. Two people applying for the same amount can receive different offers based entirely on their financial profile.

Interest Rates and Processing Fees

Annual rates run between 12% and 24% across most NBFC personal loans. Credit score, income level, and employer profile determine where in that range the borrower lands. Processing fees sit between 1% and 3% and appear in the Key Fact Statement before any decision needs to be made.

Repayment Tenure and EMI Options

12 to 36 months. Shorter tenure means lower total interest but a higher monthly outflow. Longer tenure does the reverse. Flexi variants exist on some platforms where the borrower draws from a limit and pays interest only on what is actually being used at any given time.

Eligibility and Credit Score Requirements

Age 21 to 58. CIBIL score of 725 or above. Verifiable monthly income. Self-employed applicants substitute salary slips with bank statements and ITR. Total EMI obligations across all active loans should stay under 50% of net monthly income per RBI norms.

NBFC Personal Loan Online: The Digital Application Process

Having PAN, Aadhaar, salary slips, and bank statements ready before starting makes the NBFC personal loan online process considerably faster.

- Open the loan app or the lender website

- Register using a mobile number and complete e-KYC with Aadhaar OTP and PAN

- Enter income, employment details, and the amount needed

- Upload documents digitally, nothing physical goes anywhere

- Review the offer: rate, EMI, processing fee, tenure

- Accept and receive funds directly in the bank account per RBI Digital Lending Directions 2026

Also Read: Digital Lending Platforms in India: Transforming Credit Access

Choosing the Best NBFC for Personal Loans

Picking the best NBFC for personal loan products is not just about comparing interest rates on a spreadsheet.

- Check RBI registration at rbi.org.in before sharing any financial data

- Look at the Annual Percentage Rate, not just the headline rate, since processing fees change the real cost

- Read prepayment terms before accepting any offer

- Check customer support availability because loan issues rarely arise at convenient times

- An existing borrowing relationship with the NBFC can unlock pre-approved offers and better terms on the next application.

Hero FinCorp: A Leading NBFC for Personal Loans

Hero FinCorp has been in retail lending since 1991 as a licensed NBFC under the Hero Group. As one of the best NBFC lenders in India, it offers loan amounts based on real repayment capacity, tenures from 12 to 36 months, a fully digital process with no branch visit, a Flexi Loan option, and upfront pricing with no hidden charges.

Apply for a Hero FinCorp personal loan here for quick disbursals. Download the instant loan app on Google Play or the personal loan app on the App Store.

Frequently Asked Questions

What is an NBFC personal loan?

A loan from a Non-Banking Financial Company licensed by the RBI. No collateral, no branch visit. The lender reads income, credit score, and employment and generates an offer. Funds land directly in the bank account. End use is unrestricted. Medical bills, home repairs, travel, debt consolidation, a wedding, the borrower decides. Nobody asks what the money is for.

How does an NBFC personal loan differ from a bank loan?

Speed and who gets approved are where the actual difference shows up. Banks draw the CIBIL line at 750. NBFCs work from 650. Banks take longer and ask for more documentation. Someone with a strong credit profile at a large employer might get a slightly lower rate from a bank. Everyone outside that narrow profile tends to get a better result from an NBFC, faster and with considerably less friction at every stage.

Can I apply for an NBFC personal loan online?

Yes, entirely. The whole NBFC personal loan online journey covers identity verification, income assessment, and offer acceptance on a phone or laptop. Nothing physical needs to go anywhere.

What is the minimum credit score for an NBFC personal loan?

Most NBFCs set the minimum at 650. Below that the options narrow but do not disappear entirely, since income consistency and banking behaviour carry weight alongside the bureau number. Someone earning steadily with 12 months of clean bank credits has a reasonable shot even with a lower score.

How fast can I get approval from an NBFC?

NBFC personal loans are often disbursed almost instantly for eligible applicants. Automated underwriting removes the manual review queue. Applicants with documents ready and a qualifying income profile can receive funds the same day in many cases.

What documents are required for an NBFC personal loan?

PAN card, Aadhaar, income proof. Salaried applicants need recent salary slips and three to six months of bank statements. Self-employed applicants need bank statements and one to two years of ITR. Everything goes in through the app. No courier, no attested copies, no branch counter.

Are NBFC personal loans safe and regulated?

NBFCs function under the Companies Act and the Reserve Bank of India regulates them directly. RBI rules cover rate disclosure, direct bank account disbursal, data protection, and fair recovery practices. Checking the lender's registration at rbi.org.in before applying is a basic step worth taking. A registered NBFC carries the same borrower protections as a bank on unsecured personal loans.

What are the interest rates on NBFC personal loans?

Rates generally run from 12% to 24% annually across NBFC personal loan products. Credit score, income level, and employer profile determine the actual number. It shows up in the loan offer and the Key Fact Statement before the borrower commits to anything.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision...

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.