UPI Transaction Charges: Limits, Fees & Rules

UPI is now India’s go-to payment method, used for everything from daily purchases to large recurring payments, including paying with QR codes at stores. With new NPCI and RBI updates, one question keeps coming up: “Are there any UPI charges in 2026?”

Here’s a simple, updated breakdown of UPI transaction charges, limits, interchange fees, and the latest rules for 2026.

What Are UPI Transaction Charges?

The simple answer: Most UPI payments remain completely free for users.

NPCI built UPI as a public, zero-cost payment network for P2P (person-to-person) transfers.

This means:

- Sending money to friends/family: Free

- Bank-to-bank QR payments in stores: Free

- UPI Lite payments: Free

- UPI AutoPay (subscriptions): Free for users

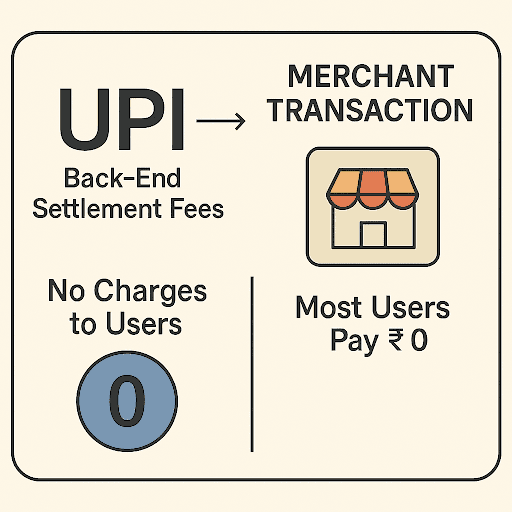

So why do people hear about “UPI fees”? Some fees apply only to specific merchants or wallet-based transactions, not to general users. The term “UPI charges” refers to internal settlement costs between payment providers and is not charged to users.

UPI Transaction Limit Per Day, Week & Month in India

NPCI sets a standard daily limit of ₹1 lakh per user for most UPI payments. However, higher limits apply for specific categories where large-value payments are common.

| Category | Previous limit | Updated Limits (Post Sept 15, 2025) |

| Regular UPI users | ₹1 lakh/day | ₹1 lakh/day |

| Capital markets | ₹2 lakh/day | ₹5 lakh/day |

| Insurance payments | ₹2 lakh/day | ₹5 lakh/day |

| Government payments | ₹1 lakh/day | ₹10 lakh/day |

| Hospitals & education | ₹1 lakh/day | ₹5 lakh/day |

Additional Notes:

- Some banks may set their own limits on per-transaction value.

- Many banks restrict UPI to 10-20 transactions per day for security reasons.

- Weekly and monthly UPI limits vary by bank and risk category.

- UPI Lite has separate limits (e-balance and per transaction).

If you ever hit a payment cap while completing an urgent transaction, using a reliable instant loan app can help you manage short-term financial needs without delays. It will ensure you have uninterrupted access to funds whenever an unexpected expense arises.

When Do UPI Transaction Charges Apply?

Although personal payments, including paying with QR codes, are free, certain merchant-side rules involve fees. These do not impact users directly.

Here are the only scenarios where charges on UPI transactions may exist:

1. Wallet-based merchant payments above ₹2,000

- Interchange fees apply (0.5%–1.1%).

- Only the merchant or wallet issuer pays this fee.

- Users are not charged.

2. Wallet top-ups using credit cards

- Some wallet providers may apply service fees.

- These are platform-based, not UPI charges.

3. Merchant payments via prepaid payment instruments (PPIs)

- UPI-PPI transactions carry interchange fees.

- Again, these fees are not charged to customers.

4. Business-side settlement charges

- Applicable only for merchant accounts or commercial entities.

- Consumer payments remain free.

Bottom line: For everyday users, UPI = ₹0 charges unless you use specific wallet-based features, and even then, you still aren’t charged.

Understanding Interchange Fees in UPI Transactions

Interchange fees often cause confusion; here’s a simple explanation:

What Is It?

A small fee is paid between payment service providers to support processing, settlement, and infrastructure.

Who Pays It?

- Merchants

- Wallet issuers

- Payment service providers

Users do not pay interchange fees.

Where Does It Apply?

- Wallet-based UPI merchant payments

- PPI-linked transactions

- High-value QR payments in some categories

Also Read: UPI vs PPI - Understanding the Key Differences

Where Does It Not Apply?

- P2P transfers

- P2M payments are done directly from bank accounts

- UPI Lite

- UPI AutoPay

- Bank-to-bank QR payments

In short, if you use UPI normally, you pay ₹0.

UPI Transaction Charges and Limits Across Different UPI Apps

Different UPI apps follow similar RBI and NPCI guidelines, but transaction limits, merchant fees, and transaction status checks may vary slightly by platform.

| UPI App | User Charges | Merchant Charges | Daily Transaction Limit | Additional Limit |

| PhonePe | Free for users | 0.5%–1.1% interchange fee in some categories | Up to ₹1 lakh | Max 20 transactions daily |

| Google Pay | Free for users | Applicable for some merchants | Up to ₹1 lakh | Max 20 transactions daily (Standard NPCI limits apply) |

| Paytm | Free for users | Charges may apply for merchants on select transactions | Up to ₹1 lakh | Limits may vary by bank |

| Amazon Pay | Free for users | Merchant interchange charges may apply | Up to ₹1 lakh | Standard NPCI limits apply |

| BHIM UPI | Free for users | Merchant fees may apply in some cases | Up to ₹1 lakh | Max 20 transactions daily |

UPI Transaction Limits for Top Banks in India

UPI transaction limits in India are broadly guided by NPCI rules, but individual banks may apply their own transfer and daily usage restrictions.

| Bank Name | UPI Daily Aggregate Limit | UPI Per-Transaction Ceiling | Max P2P Transactions / Day |

| State Bank of India (SBI) | ₹1,00,000 | ₹1,00,000 | 20 Transactions |

| Punjab National Bank (PNB) | ₹50,000 | ₹25,000 | 10 Transactions |

| IDFC FIRST Bank | ₹1,00,000 | ₹1,00,000 | 20 Transactions |

| Indian Bank | ₹1,00,000 | ₹1,00,000 | 20 Transactions |

| Bank of India (BOI) | ₹1,00,000 | ₹1,00,000 (₹10,000 cap on standard P2P transfers) | 10 Transactions |

| Indian Overseas Bank (IOB) | ₹1,00,000 | ₹50,000 | 10 Transactions |

Note: These baseline caps scale up significantly to ₹5 Lakh for specific regulated high-value transactions like Tax Payments, Hospital bills, Educational institutional fees, and verified IPO subscriptions.

New UPI Rules & Settlement Guidelines Effective 2025

NPCI announced several updates in August and November 2025 to strengthen UPI safety, transparency, and settlement.

Important Rule Changes:

- Separate Settlement Cycles: Authorised vs disputed transactions now settle differently for better tracking.

- Limits on Balance Checks: Reduce unnecessary load on the system.

- Restrictions on Frequent Account Linking: Designed to prevent fraud.

- Updated Auto-Debit Processing Window: Ensures smoother recurring payments.

- Improved Payee Name Display: Enhances clarity before confirming a transaction.

- Faster Settlement Timeline for Merchants: Helps businesses track payments in real time.

Also Read: Payee Meaning in Banking and Finance Explained

How This Impacts You:

- More transparency when sending money

- Smoother recurring payments

- Better fraud prevention

- Clearer transaction details

- Reduced failed transaction risk

If you often pay bills, EMIs or service fees via UPI, keeping your bank account funded is essential. On this note, Hero FinCorp offers instant personal loans to help you manage unexpected expenses without disrupting your payments.

Install our app now and apply for an instant personal loan in just a few steps!

Conclusion

UPI transactions remain free for everyday users, while higher limits apply only to select categories such as taxes, healthcare, education, and certain investment payments. By keeping up with custom bank limits and new fraud-prevention safety protocols, consumers can confidently navigate India's financial ecosystem with complete peace of mind.

Frequently Asked Questions

Are UPI transactions free for personal users?

Yes. Bank-to-bank UPI payments remain free for regular users.

Who pays UPI interchange fees?

Merchants or wallet issuers, and not customers.

Is there a daily limit for UPI transactions?

Yes. Most users have a limit of ₹1 lakh per day.

What charges apply for wallet-based UPI payments?

Interchange fees may apply for merchants on transactions above ₹2,000.

Can banks set their own UPI transaction limits?

Yes. Banks can set daily, weekly, and monthly caps for risk control.

Are there any hidden fees in UPI transactions?

No hidden charges apply to personal UPI payments.

How many UPI transactions can I make in a day?

Most banks allow 10–20 transactions daily, but this varies based on your bank’s internal policies and security guidelines.

Is there any hidden income tax liability if I receive more than ₹50,000 through UPI from friends?

Personal transfers from friends are usually not taxed as income, but tax treatment can depend on the nature of the transfer.

Do I have to pay any charges if I hit my daily UPI transaction limit?

No extra charges apply. Further transactions are usually blocked until the bank’s daily UPI limit resets automatically.

What is the maximum amount a newly registered UPI user can transfer?

Many UPI apps temporarily restrict new users to around ₹5,000 during the first 24 hours after registration.

Are merchants charged a fee when a customer loads their wallet using UPI?

Merchants may incur interchange or processing charges depending on wallet provider policies and transaction categories involved.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.