UPI vs PPI - Understanding the Key Differences

Digital payments are prominently used among Indians. People are using online payment methods to pay grocery stores, shopkeepers, and even to split restaurant bills.

The key online payment systems enabling such transactions are Unified Payments Interface UPI and Prepaid Payment Instruments PPI.

They are both cashless but differ from each other. In UPI, the user's bank account is linked with the app, whereas in PPI, the user has already paid the amount.

To determine which is better, let us compare UPI vs PPI.

What is UPI?

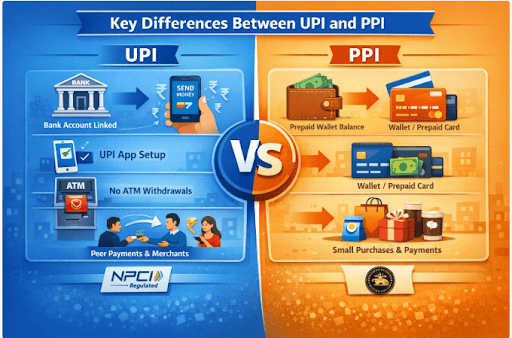

Unified Payments Interface is a mobile-based digital payment system that allows users to make online payments or transfer funds using a UPI ID, mobile number, or QR code.

Key characteristics of UPI:

- Direct bank account transfers

- Instant payment availability 24/7

- Secure authentication using a UPI PIN

- Support for QR code payments and bill payments

Also Read: What is UPI and How Does UPI Work?

What is PPI?

A Prepaid Payment Instrument is a system in which the user deposits money into a wallet, card, or voucher before making transactions.

PPIs are used for:

- Online purchases

- Mobile recharges

- Utility bill payments

- Transport and ticket bookings

Types of PPI Explained

According to RBI guidelines, PPI types are based on how and where they can be used.

1. Closed PPIs

Closed PPIs are issued by a company, and users can purchase goods or services only from that company. Cash withdrawal or fund transfers are not permitted.

Examples:

- Store gift cards

- E-commerce store credits

2. Semi-Closed PPIs

Semi-closed PPIs can be used across multiple merchants that accept the wallet/instrument. They cannot be used for cash withdrawals.

You can use them for:

- Digital wallet payments

- Utility bill payments

- Retail transactions

3. Open PPIs

Open PPIs are issued by banks and provide greater flexibility compared to other UPI and PPI types.

Users can:

- Make purchases

- Transfer funds

- ATM cash withdrawals

Difference Between UPI and PPI

Here is the UPI and PPI difference:

| Feature | UPI | PPI |

|---|---|---|

| Source of funds | Linked to a bank account | Preloaded wallet balance |

| Payment method | Bank-to-bank transfer | Wallet or prepaid instrument |

| Setup requirement | Bank account linked to the UPI app | Wallet balance must be loaded first |

| Cash withdrawal | Not used for ATM withdrawals | Allowed only for open PPIs |

| Usage | Peer transfers, merchant payments | Merchant payments, small transactions |

| Regulation | NPCI framework under RBI oversight | Regulated by RBI |

UPI vs PPI

The difference between UPI and PPI relates to how money flows during a transaction.

With UPI, the transaction debits your bank account at the time of payment. This makes UPI suitable for quick transfers between individuals or merchants.

PPI instruments work differently. Funds are first added to the wallet or prepaid account. Payments are then made using that stored balance.

The QR-based payment and mobile-based payment options are available in both the UPI and PPI, which makes both extremely popular in the digital payment space.

How UPI and PPI Complement Each Other

Although UPI and PPI differences exist,, there is not always competition. In many cases, these systems work together.

UPI is ideal for:

- Sending money instantly to friends or family

- Paying merchants directly from a bank account

- Large-value daily transactions

PPIs can be useful for:

- Budgeting daily spending

- Managing prepaid balances for specific purposes

- Making quick micro-payments

Recent regulatory developments have also facilitated greater interoperability between UPI and PPI systems. This has helped to make digital payments even more flexible and user-friendly.

UPI & PPI Transaction Charges & Limits

The transaction limits and charges may vary depending on the guidelines issued by the RBI.

| Payment System | Transaction Limit | Charges |

|---|---|---|

| UPI | Often up to ₹1 lakh per transaction (varies by bank) | Usually free for individual users |

| PPI Wallets | Limits depend on wallet type and KYC status | Some services may include fees |

| Prepaid Cards | Issuer-specific limits | Charges may apply for certain transactions |

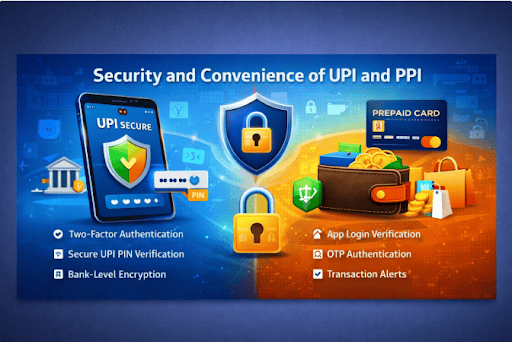

Security and Convenience of UPI vs PPI

Both payment systems are designed with security mechanisms that help protect user transactions.

UPI security features include:

- Two-factor authentication

- Secure UPI PIN verification

- Bank-level encryption

PPI wallets use:

- App login verification

- OTP authentication

- Transaction alerts

Choosing Between UPI vs PPI - What Suits You Best?

Here are the basic differences between the two:

- UPI is best suited for direct bank transfer.

- PPI is best suited for a prepaid budget.

Many users combine both options for everyday convenience.

Using Digital Payment Solutions

Digital payments have simplified financial transactions. By understanding the different types of UPI and PPI, you can make the best use of digital payment services.

For digital users, financial tools are often used alongside payment options. If you face an unexpected expense, you may choose financial options like checking your eligibility for a personal loan.

You can check your eligibility for a Hero FinCorp personal loan online here. The process can also be managed on mobile through the Hero Digital Lending App (Android/iOS).

Frequently Asked Questions

What is the difference between UPI and PPI?

UPI facilitates instant bank transfers, while PPIs are prepaid instruments that store funds and can be used to make payments.

Are UPI transactions free to use for individuals?

Yes, most UPI transactions are free to use, although policies may vary.

What are the transaction limits applicable to UPI and PPI?

The transaction limit applicable to UPI is usually up to 1 lakh rupees, while that applicable to PPI depends on the wallet type and KYC status.

Can PPI be used to connect with UPI?

Yes, it is possible to connect PPI with UPI systems.

How secure are UPI and PPI transactions?

Both UPI and PPI transactions are secure and include various security features to ensure maximum protection.

What different PPI types are available?

The various types of PPIs available are closed, semi-closed, and open PPIs.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

A decade ago, if someone said cash payments would have a serious rival, no one would’ve believed it. But today, that’s a reality.

For daily necessities like shopping, bill payments, subscriptions, and EMI repayments, people in India rely on a variety of payment methods. With the widespread acceptance of cards, wallets, and UPI apps, digital payments have become commonplace.

A few years back, leaving home meant checking for your wallet first. Cash, bank cards, faded receipts, maybe a few coins rattling around. Now, many of those payments happen through a phone without much thought. Tap at the kirana store, scan to pay the cab driver, and settle a bill while standing in line. Digital wallets have slipped into everyday life across India.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.