How NRI Users Can Send Money to India Using UPI

Sending money to India from another country used to mean long wait times, high fees, and complicated banking processes. But not anymore, thanks to UPI.

In November 2025 alone, UPI processed over 20.4 billion transactions worth ₹26.3 lakh crore in India, showing just how trusted and widely used the system has become.

With recent updates from the National Payments Corporation of India (NPCI), UPI for NRIs enables quick, secure, and low-cost transfers directly from their NRE or NRO bank accounts.

This guide explains how UPI for NRIs works, who is eligible, and how you can get started. Read on!

More About NRI UPI Payments

Unified Payments Interface (UPI) enables users to transfer funds instantly between bank accounts in India. UPI for NRIs enables non-resident Indians to use the system with their NRE/NRO accounts to send money conveniently via registered Indian or international mobile numbers. NRIs can use UPI payments to

- Send money quickly to friends and family.

- Make quick domestic transfers.

- Pay bills

Read More: Cross-Border UPI—Paying Abroad with Indian Tech

UPI For NRI- Eligibility Criteria

When it comes to using UPI as an NRI, certain eligibility conditions must be met to ensure compliance with RBI and NPCI guidelines. These requirements help banks verify identity, account type, and international usage permissions before enabling UPI access.

To be eligible for UPI as an NRI, you:

- Must hold NRE or NRO bank accounts in India

- Must qualify as an NRI under RBI regulations

- Must have a mobile number (Indian or International) registered with the bank

- Must be from one of the countries (USA, UK, UAE, Singapore, Canada, Australia) approved for international UPI transactions.

Want a loan but not sure if you’re eligible? Use our loan eligibility calculator to find out instantly!

UPI Setup for NRIs – Step-by-Step Guide

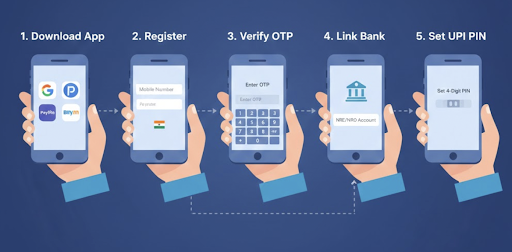

Setting up UPI International is quite simple.

Follow these steps to activate UPI on your NRE or NRO account and start making payments seamlessly from abroad:

- Download an international UPI app such as Google Pay, PhonePe, Paytm, or BHIM.

- Register yourself with the mobile number associated with your NRE/NRO account.

- Type the OTP sent by your bank for verification.

- Select your bank for NRE/NRO and link your account.

- Set your UPI PIN to complete the UPI international setup.

Also Read: How to Change and Reset UPI PIN?

UPI Payments for NRIs: How Does it Work?

UPI payments for NRIs work just like regular UPI transactions, but the transfer originates from outside India.

Here is a step-by-step account of how NRI UPI payments work:

| 1. Payment Initiated | NRI uses an international UPI app from abroad |

| 2. Request Sent to Indian Bank | App forwards UPI request to NRE/NRO-linked bank |

| 3. Account Debited in INR | The bank deducts funds from the NRE/NRO account. |

| 4. Transaction Completed | The recipient in India receives INR instantly |

Currency Conversion

- No direct foreign-currency handling via UPI.

- Conversions happen before the funds enter the NRE/NRO account via the bank/card network. The conversion rates vary and are not controlled by UPI.

- Transfers remain in INR.

- There’s no fee for international transfer.

Transaction Limits

- Up to ₹100,000 daily

- Transaction limits can vary.

Here's a breakdown of the differences between NRE and NRO Accounts for UPI Payments for NRIs:

| Feature | NRE Account | NRO Account |

| Fund Origin | Foreign income | Indian income |

| Repatriation | Full | Restricted |

| Tax | No | Yes |

UPI for NRI- Benefits

Let’s take a look at how UPI makes a real difference for NRIs through a simple, everyday example:

Aarav and Rishi both live in Dubai and send money to their families in India every month.

But their experiences couldn’t be more different.

Aarav uses UPI International on his UAE mobile number.

Rishi still uses traditional remittance services.

Aarav needed to send ₹10,000 to his parents.

He opened an international UPI app, selected his NRE account, and hit send.

Money reached in seconds. No fees. No delays.

Rishi, on the other hand, used his usual money transfer service. The process took longer and came with additional charges.

This contrast highlights why many NRIs are switching to UPI. Here are the key benefits of using UPI for NRI payments:

- Transfer instantly to any Indian bank

- Low or Nil fees for UPI transactions

- Use UPI apps from anywhere in the world

- Simple and secure payments, backed by NPCI standards

- No need for complicated wire transfers or high forex charges

Read More: Advantages of Using UPI for Everyday Transactions

Conclusion: Is UPI the Best Payment Option for NRIs?

With UPI for instant payments, managing finances has never been more convenient for NRIs.

However, if you need extra funds for medical expenses, home upgrades, travel, or education, a hassle-free, fully digital, paperless personal loan from Hero FinCorp can provide the support you need quickly and reliably.

What makes it even better? You can pay your loan EMIs through UPI in just a few seconds. Platforms like Hero FinCorp let you set up UPI AutoPay, so your EMIs are always paid on time without any reminders.

So why wait? Check your personal loan eligibility and apply online—take control of your finances today!

Frequently Asked Question

Can NRIs use any UPI app or only specific ones?

NRIs can use most major UPI apps. However, the app and the bank should support NRE/NRO accounts and international mobile numbers.

Is it mandatory to have an Indian mobile number for UPI?

NRIs can register using international mobile numbers linked to their NRE or NRO bank accounts.

Are there any fees for UPI transactions for NRIs?

There are no additional charges from banks or apps for NRIs when sending or receiving money via UPI.

What is the daily limit for UPI for NRIs?

Most banks allow up to ₹100,000 to be transferred daily via UPI. Some banks may set lower limits for NRE/NRO accounts or newly activated international numbers.

Disclaimer: The information provided in this is for informational purposes only. While we strive to present accurate and updated content, travel conditions, weather, places to visit, itineraries, budgets, and transportation options can change. Readers are encouraged to verify details from reliable sources before making travel decisions. We do not take responsibility for any inconvenience, loss, injury, or damage that may arise from using the information shared in this blog. Travel involves inherent risks, and readers should exercise their judgment and caution when implementing recommendations.