Difference Between Borrowing and Lending: A Comprehensive Guide

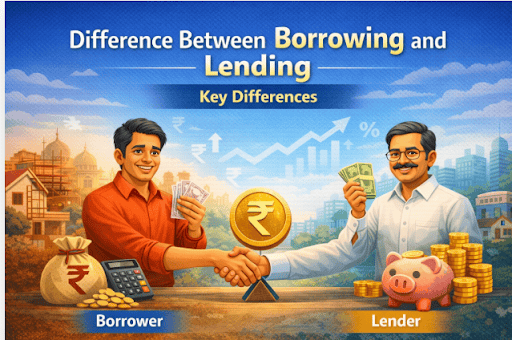

Borrowing and lending in financial transactions are like two sides of the same coin. For example, Mr. Rajan Katiyar from Delhi required ₹2 lakh to fix his house. He sought the help of a financial organisation and got a personal loan. Here, Rajan is borrowing the money, and the financial organisation is lending it.

The above example explains the difference between borrowing and lending. While both activities deal with finances, the functions played by both parties involved differ.

Understanding the difference between borrowing and lending helps people make sound financial decisions in a country like India, which is witnessing massive growth in its financial domain.

Understanding the Concept - What is Borrowing and Lending?

Lending and borrowing are an exchange of funds where borrowers agree to return the borrowed funds at a future fixed date to the lender.

Borrowing is the receipt of funds by the recipient on the condition that he/she will return them at a later time with interest attached.

Lending means providing funds to the recipient with a view to earning interest on the amount lent.

In the BFSI segment of India, lending and borrowing form the core of several transactions.

Borrowing is done by individuals and businesses to meet various needs, such as everyday expenses, education, medical expenses, travel, or home purchases.

Lenders include banks and NBFCs that provide loans as part of their services. Lenders can also be family members or friends who give loans based on relationship and goodwill, not profit-making.

Also Read: Difference between Banks and NBFC

What’s the Difference Between Lending and Borrowing?

Here, we will understand the difference between lending and borrowing and why both roles are essential for financial systems to operate smoothly:

| Feature | Borrowing | Lending |

|---|---|---|

| Meaning | When you take a loan from someone in exchange for a promise to repay it on time with interest | Lending money to someone else with the expectation of repayment with interest |

| Financial Position | Represents the borrower’s liability | Represents the lender’s asset |

| Objective | For meeting the financial requirements for various expenses | For making profits by way of interest |

| Impact of Interest | Interest payment is a cost of borrowing | Interest earned becomes income for the lender |

| Risk Involved | Debt burden | Borrower default |

| Examples | Personal loans, home loans, business loans, or education loans | Lending through bank loans, NBFC lending, and P2P lending |

Role of Interest in Borrowing and Lending

Interest plays an important role in lending and borrowing.

- For borrowers, interest means the price at which borrowed money can be utilised. Interest payments are made in monthly installments.

- For lenders, the interest payment means the return generated from risk-bearing and opportunity costs.

The following factors impact the amount charged and earned through interest:

- Monetary policies of the RBI

- The repo rate that impacts bank and non-banking finance companies' lending rates

- Borrower's creditworthiness and capability to repay

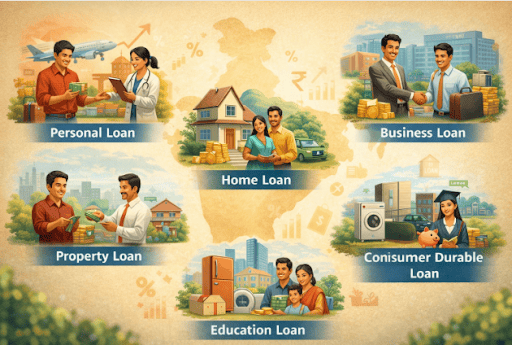

Lending and Borrowing Facilities Available in India

India has many lending and borrowing facilities that suit various financial purposes. Some of the most common ones are:

- Personal Loans: An unsecured loan that helps to meet financial emergencies such as health expenses, travel, education, or home repairs.

- Home Loan: A secured loan that can be availed to buy or build a home.

- Business Loan: This type of loan helps facilitate business growth and expansion.

- Property Loan: The borrower keeps their property as collateral to raise funds.

- Consumer Durable Loan: A loan facility to purchase consumer durables, such as electronics and appliances.

- Education Loan: A loan facility that helps to pay for children’s education.

Also Read: Can I Take Home Loan and Personal Loan Together?

Risk Assessment - Borrower’s vs. Lender’s Perspective

Both borrowing and lending have financial risks.

Risks for the borrower are:

- Inability to manage repayment

- Higher interest liabilities

- Poor credit rating due to nonpayment of EMIs

- The danger of being caught up in a debt trap by borrowing too much money

Also Read: What does EMI mean? Full form, how it works

For the lender, however, there is one primary risk, which is credit risk, or the risk of failure by the borrower to pay back the loan taken.

Lenders consider the following factors to mitigate the risks mentioned above:

- Credit rating and credit history

- Financial standing

- Current liabilities

- Debt/equity ratio.

How to Transition from a Borrower into an Investor

![]()

Borrowing can be unavoidable at different stages of one’s life, depending on circumstances. But strategic planning can enable people to advance towards generating their wealth.

Some steps include:

- Borrowing prudently

- Developing a positive credit score by repaying debts on time

- Saving and investing money

- Minimising financial liabilities

- Applying loans effectively wherever necessary.

Conclusion

It is imperative to understand the difference between lending and borrowing for making wise financial decisions. Borrowing helps people and companies get money whenever they require it. At the same time, lending helps banks contribute to economic development by generating interest revenues.

Both these processes are crucial in the Indian financial sector. However, one should borrow responsibly and manage their finances prudently.

If you wish to borrow money for your requirements, you may proceed with the Hero FinCorp personal loan experience journey.

One can also apply for loans efficiently using the Hero Digital Lending and UPI App - Android/iOS.

Frequently Asked Questions

What’s the difference between lending and borrowing?

To borrow means to get money with an agreement to pay it back. To lend means to give money with an understanding that it should be repaid on time.

Can one be both a borrower and a lender at once?

Yes. One can lend and borrow money at the same time by borrowing for one purpose while also lending by making strategic investments.

Does borrowing and lending always involve the payment of interest?

Generally, it does. When you borrow from someone, you pay interest to him/her as compensation for his/her money. In a few cases, where money is borrowed by near and dear ones, lenders can forego interest.

How can I use my credit score to get a loan in India?

Having a good credit score increases the chances of obtaining a loan at low interest rates.

What type of risks would a lender take?

There may be a risk that the borrowed money could become a non-performing asset if the borrower does not repay it.

Is borrowing an asset or a liability?

Borrowing is a liability for a person, as he/she is taking out a loan and have to repay it within the specified time, with an additional interest charge as compensation to the lender.

What are some common examples in lending?

Some examples in lending include banks offering personal and business loans. Sometimes people lend money to their friends or family members (with or without interest).

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.