What is Written Off in CIBIL? A Complete Guide to Its Meaning and Impact

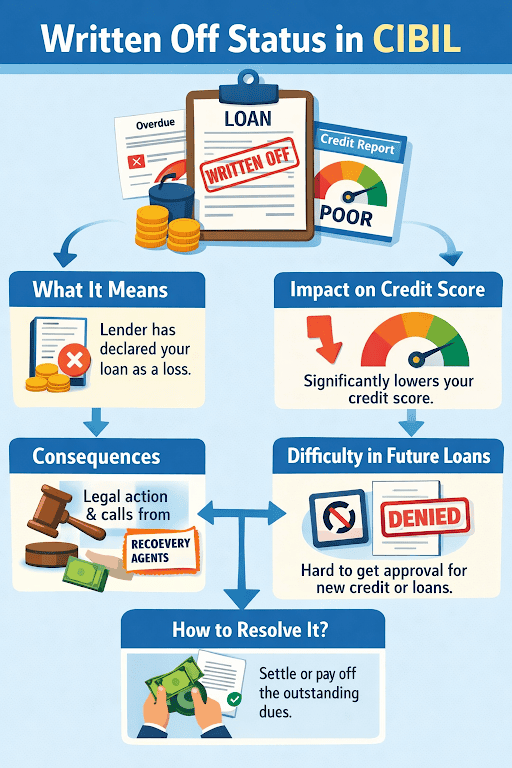

Written-off in CIBIL means a lender has classified your loan as a loss after prolonged non-payment (usually 180+ days overdue). It is an accounting action, not a waiver. You still legally owe the money, and the status negatively impacts your credit profile.

Seeing “written off” in your credit report can feel alarming. Many people assume it means the bank has forgiven the loan. Unfortunately, that’s not true.

A written-off status simply means the lender has stopped treating your loan as a performing asset because payments have not been made for a long period. Your repayment obligation continues.

Let’s break it down clearly.

Understanding the Written Off Meaning in CIBIL

As per guidelines issued by the RBI Master Circular on Prudential Norms (July 2023, IRAC norms), a loan account becomes a Non-Performing Asset (NPA) when payments remain overdue for 90 days. If dues remain unpaid for around 180 days or more, lenders classify the account as a “loss asset” and write it off for accounting purposes.

This does NOT mean:

- The loan is cancelled

- Recovery stops

- Legal action cannot be taken

It simply means the lender has removed the bad debt from its active books.

Types of Write-Offs

1. Total Write-Off

The lender writes off the entire outstanding amount—principal plus accumulated interest.

2. Principal Write-Off

Only the principal amount is written off. Interest and penalties may still appear outstanding and remain payable.

Why Does a Written Off Status Appear on Your Report?

A written-off status usually appears due to prolonged default. Common reasons include:

- Non-payment of EMIs for over 6 months

- Unpaid credit card dues despite reminders

- Settlement for less than the full amount without a No Dues Certificate (NDC)

For example, consider the case of a person based out of a tier-2 city who defaulted on several bike-loan EMIs after he lost his job for some time. And after 180 days of not being paid, the lender is able to write off the account.

Also Read: What is the Effect of Closing a Credit Card on Credit Score?

Will Interest Continue After Write-Off?

Yes. Often, contractual interest continues to run until any loan is repaid in full unless the lender agrees otherwise, in writing.

A write-off is simply an internal accounting adjustment; it does not suspend interest or cease collection activity.

How Written Off in CIBIL Affects Your Financial Future

There are various ways a written-off status in ClBIL can impact your financial standing, including-

a. Impact on Credit Score

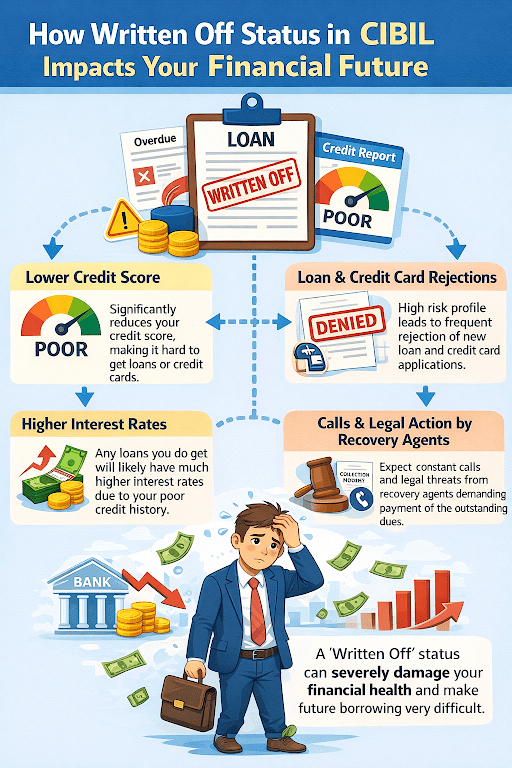

A written-off status in your CIBIL report can cause an immediate and significant drop in your credit score. Industry observations suggest the impact can exceed 100 points depending on your profile, payment history, and credit mix.

This signals a serious default to lenders and reduces creditworthiness.

b. Difficulty in Future Loan Approvals

Lenders typically treat a written-off account as a high-risk indicator, as it shows past inability to repay debt. This makes banks cautious and reduces approval chances for home, car, or business loans.

Also Read: What is the Difference Between Loan Write off and Loan Waive off?

Step-by-Step Guide: How to Clear a Written Off Status

Here is how you can proceed to clear a written-off status-

1. Obtain Your Credit Report

Apply for a detailed credit bureau report from the TransUnion CIBIL.

2. Get in touch with the Lender

As a second step, you will have to get in touch with the lender recovery / nodal officer to confirm the actual amount payable and discuss repayment options.

3. Negotiate Full & Final Settlement

Instead of requesting a partial loan settlement letter, it is better to get them ready for the full and final payment.

4. Collect No Dues Certificate (NDC)

After clearing your dues, you must get a signed NDC – this acts as an acknowledgement of the fact that no amount is pending from your end.

5. Confirm Status Update

Verify that the lender updates the account status as Closed with CIBIL (within a month to 45 days) after payment is made.

6. Raise a Dispute if Needed

If your report is not updated, raise a credit bureau dispute online through CIBIL’s dispute resolution portal and attach payment proof and NDC.

Strategies to Rebuild Credit After a Write-Off

Being written off is serious, but it is not permanent. The key is structured repayment and disciplined credit behaviour to improve your credit score.

Clear outstanding dues, obtain proper documentation, monitor your report regularly, and rebuild gradually.

If you need structured repayment support, you may explore regulated lending options such as the Hero Fin Corp Personal Loan App after carefully checking eligibility.

Disclaimer: Information provided here is for educational purposes only and does not constitute financial advice. Consult a qualified financial advisor for personalised guidance.

Also Read: Personal Loan Default Consequences in India & Legal Impact

Can Lenders Still Take Action After Write-Off?

Yes. Write-off does not prevent:

- Recovery calls

- Legal notices

- Civil recovery proceedings

- Reporting to credit bureaus

For secured loans, lenders may initiate recovery under the SARFAESI Act provisions. Also, under the Limitation Act, lenders typically have three years from the date of default to initiate legal recovery (subject to acknowledgements or part-payments extending the limitation).

Take Control Today to Rebuild Your Credit Future

Being written off should not be seen as the end of your financial standing, but rather a serious wake-up call. The good news is: recovery is achievable with time and effort.

Begin by paying back all your pending liabilities through a structured time-bound repayment model. Then work on the opportunity to restore your credit with judicious borrowing and timely repayment.

If you need a structured personal loan, services like Hero FinCorp Personal Loan App could be one avenue.

Also Read: Days Past Due: Meaning & Calculation in CIBIL Report

Frequently Asked Questions

1. Does "Written Off" mean I don't have to pay the money back?

No, you still legally owe the money.

2. Can I get a home loan if I have one written-off account?

It becomes difficult unless cleared, and your score improves.

3. What is the difference between ‘Settled’ and ‘Written Off’?

“Settled” means partial repayment accepted; “Written Off” means classified as a loss due to non-payment.

4. Can CIBIL remove the status if I pay only the principal amount?

No, the lender must update the account after proper settlement.

5. Will my CIBIL score improve immediately after repayment?

No, improvement is gradual over time.

6. Does partial payment revive the account?

Partial payment may update the balance, but usually changes status to “Settled,” not “Closed.”

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.