What is NMI in a loan? Understanding Net Monthly Income

Rohit earns well and feels confident about applying for a personal loan. When the lender reviews his application, they ask for his Net Monthly Income instead of just his salary. He feels confused because his payslip already shows his earnings.

The lender explains that income alone does not tell the full story. This blog explains what NMI is, how to calculate it, and why it directly affects your loan approval.

What Does NMI Means in Loan?

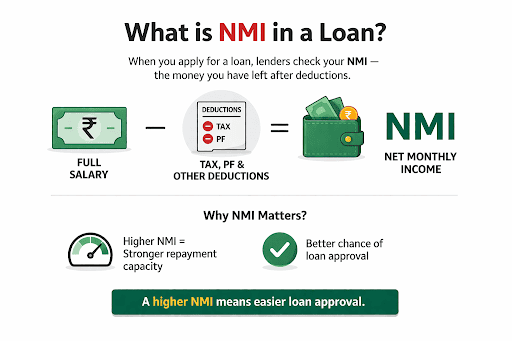

When lenders evaluate a loan application, they do not look at your full salary. They focus on what remains after regular deductions and fixed obligations. This remaining amount is called NMI in a loan assessment.

NMI shows how much money you actually have available each month to handle repayments. Lenders use this figure to understand whether you can manage a new EMI without financial strain. A higher NMI provides lenders with greater confidence because it reflects stronger repayment capacity.

NMI Full Form in Banking

Banking terms often sound technical, but the NMI's meaning is simple when broken down clearly. NMI, full form in banking, stands for Net Monthly Income.

Net Monthly Income refers to the amount you receive after deductions such as taxes, provident fund contributions, and other fixed commitments. This figure reflects your real monthly cash flow rather than your gross salary. Lenders rely on this number because it shows your actual financial position instead of a theoretical one.

Importance of NMI in Loans

Every loan decision connects back to how comfortably you can repay it. NMI plays a direct role in this evaluation process.

Lenders rely on NMI to assess repayment strength and mitigate risk. A clear view of your income helps them offer loan amounts that match your capacity.

- It helps lenders decide how much loan you can afford

- It reduces the chances of missed payments

- It ensures EMI planning stays realistic

- It builds trust between borrower and lender

How to Calculate NMI in Loans?

Understanding how to calculate NMI helps you prepare better before applying for a loan. It gives you clarity on what lenders will see when they assess your finances.

Here is a simple way to understand the NMI calculation formula:

Monthly Salary = ₹60,000

Income Tax + PF = ₹5,000

Existing EMI = ₹10,000

NMI = 60,000 − 5,000 − 10,000

NMI = ₹45,000

This final amount shows what you have available to manage the EMI for a new loan.

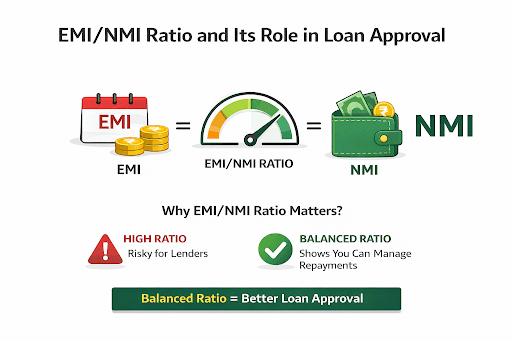

EMI/NMI Ratio and Its Role in Loan Approval

Once NMI is calculated, lenders proceed to the next step: evaluating how much of it can be applied to loan repayment. This is where the EMI/NMI ratio becomes important.

The EMI-to-NMI ratio shows what portion of your Net Monthly Income goes towards EMIs. If this ratio is too high, lenders see it as risky. A balanced ratio indicates you can manage repayments without affecting daily expenses. Most lenders prefer this ratio to stay within a comfortable range so that borrowers do not feel financially stretched.

Also Read: CIBIL Score Range: Know Whether Your CIBIL Score is Good or Bad

How NMI Affects Loan Eligibility and Approval?

Loan approval does not depend only on income size. It depends on how much usable income remains after obligations are met. This is where NMI plays a direct role.

A higher NMI improves your chances of approval because it shows stronger repayment capacity. A lower NMI reduces your eligibility even if your salary looks high. Lenders use this number to decide the loan amount, tenure, and approval confidence. NMI loan eligibility depends on how stable and sufficient your remaining income is after expenses.

What is a Good NMI Percentage for Loan Approval?

Borrowers often wonder how much of their income should go into EMIs. Understanding this helps you plan better before applying.

A good NMI percentage ensures that your EMI does not take up most of your available income. Lenders usually prefer the ideal EMIs-to-NMI ratio to stay around 30 to 40 percent. This range allows you to manage daily expenses while comfortably paying EMIs. Staying within this limit improves approval chances and reduces financial pressure.

Strategies to Improve NMI for Loan Eligibility

Improving your financial position before applying for a loan can make a clear difference. Simple steps can help you increase NMI and improve loan approval rates.

- Reduce existing loan EMIs before applying for a new loan

- Avoid unnecessary fixed expenses that reduce take-home income

- Include stable additional income sources if documented

- Choose a longer tenure to lower the EMI burden

- Maintain a clean repayment record to build trust

These actions help improve NMI and strengthen your overall loan profile.

Plan Your Loan with Clear Income Awareness

When you understand your NMI, loan decisions become easier. You know what EMI fits your budget, and avoid taking on more than you can handle.

Hero FinCorp makes this simpler with tools that help you check eligibility and move forward with clarity. A reliable personal loan app lets you track, plan, and manage your loan without confusion.

Frequently Asked Questions

What is Net Monthly Income (NMI)?

Net Monthly Income is the amount you receive after deductions like taxes and existing obligations, which reflects your real repayment capacity.

How is NMI different from EMI?

NMI shows your available income after deductions, while EMI is the fixed monthly payment you make towards a loan.

How do I calculate my NMI?

You calculate NMI by subtracting taxes, deductions, and existing EMIs from your total monthly income.

Why is NMI important for loan applications?

Lenders use NMI to assess whether you can repay a loan comfortably without financial stress.

What is a good EMI to NMI ratio?

A ratio within 40-50% is generally considered comfortable for loan approval.

Can income from investments or side jobs be included in NMI?

Yes, lenders may consider it if it remains stable and properly documented.

What documents are used to verify NMI?

Salary slips, bank statements, income tax returns, and employment proof help verify your income.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.