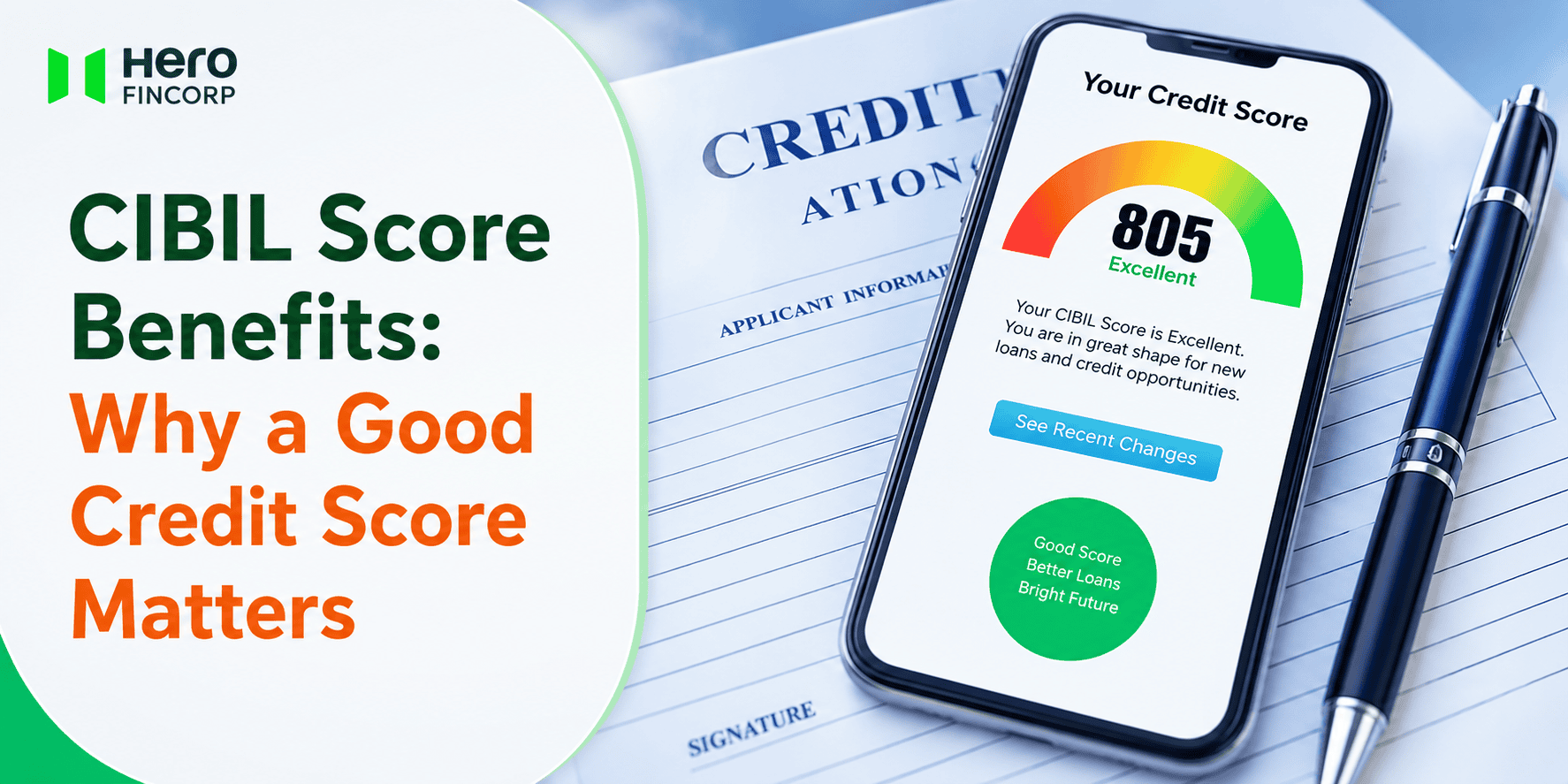

CIBIL Score Range: Know Whether Your CIBIL Score is Good or Bad

- What is the Range of CIBIL Score?

- Key Factors Influencing Your CIBIL Score

- Benefits of Maintaining a Good CIBIL Score

- Factors That Negatively Affect Your Score Range

- How to Improve and Maintain Your Score Range

- How to Check Your CIBIL Score

- Why Choose Hero FinCorp for Your Credit Needs?

- Conclusion

- Frequently Asked Questions (FAQs)

A credit score can seem like a number that has a lot of control over your money. When you learn about the CIBIL score range, you will see how it can help you get loan deals and have your loans approved faster.

You’ll want to know about it if you are looking to secure a loan or a new credit card, or if you just want to know how you are managing your money. This guide will give you all the information you need.

What is the Range of CIBIL Score?

CIBIL score is a three-digit number ranging between 300 and 900. It shows lenders how you handle your money. The range of the CIBIL Score is used by lenders to decide if you are a good credit risk and have the ability to repay the loan.

The higher your CIBIL score, the more lenders will trust you with their money. And this is why the CIBIL score range is very important.

| CIBIL Score | Credit Status | Impact on Credit Access |

| 300–549 | Poor | Very difficult to get new credit; signals past default or settlement |

| 550–649 | Fair | Some lenders may approve, but with higher interest rates |

| 650–749 | Good | Considered a healthy score; most loans get approved |

| 750–799 | Very Good | Excellent repayment history; you get competitive offers |

| 800–900 | Excellent | Top-tier credit behaviour; lenders see you as ultra-low risk |

Key Factors Influencing Your CIBIL Score

- When it comes to your payment history, missing even one EMI can significantly hurt your score and may move you down to a lower band.

- Your credit utilisation ratio is also important. If you use more than 30 per cent of your credit card limit, it looks like you are too dependent on credit.

- The length of your credit history is another thing that matters. If you have more accounts and you always make your payments on time, your credit score will be better.

- Having a credit mix is also a good idea. This means having a mix of credit, like a home loan and unsecured credit, like a personal loan.

- When you apply for a lot of loans at the same time, it can also lower your credit score. This is because it looks like you are applying for many loans at once, which is not a good sign.

Benefits of Maintaining a Good CIBIL Score

- Faster loan and credit card approvals

- Lower interest rates, saving you thousands in the long run

- Higher credit limits and better negotiating power

- Easier approvals for rental agreements and even some job roles

- Peace of mind when you need quick emergency funding

If you’re sitting in the 750+ band, checking your eligibility for a Hero FinCorp personal loan takes just minutes. Check your offer instantly with no impact on your score.

Factors That Negatively Affect Your Score Range

- Late or missed payments, even a single 30-day delinquency, get reported.

- High credit utilisation, maxing out credit cards every month.

- Multiple hard inquiries are applied to several lenders simultaneously.

- Loan settlements or write-offs stay on your report for up to 7 years.

- Being a guarantor for a loan that defaults hurts your score as well.

How to Improve and Maintain Your Score Range

To build a strong credit score, you need to follow a few small habits regularly.

- You should pay your bills on time every time. The best way to do this is to set up auto-debit for at least the minimum amount that is due. If you make one late payment, it can really hurt your credit score and make it go from good to fair.

- Don’t close old credit cards: Older accounts lengthen your credit history. Use them once every few months and pay in full to keep them active.

- Limit new applications: Each personal loan or credit card inquiry triggers a 'hard pull'. Space them out by at least 6 months.

- Monitor your co-signed accounts: If you’re a joint applicant or guarantor, ensure timely payments. Their missed EMI is your credit score dip.

- Diversify credit type gradually: A small personal loan repaid on time adds positively to your credit mix, but only when you’re ready for the commitment.

- Check your own report once a quarter: This is a 'soft inquiry' and never hurts your score. It helps you spot errors and fix them via dispute resolution.

Building a strong score takes 12–18 months of disciplined behaviour. But every timely payment moves you closer to that 'Excellent' bucket.

How to Check Your CIBIL Score

You’re entitled to one free CIBIL report per year. Here’s the simplest way:

- Visit www.cibil.com

- Click and generate the report

- Fill in your credentials

- Verify your identity via OTP and reply

- Your score and detailed report appear instantly.

Alternatively, many digital lending apps (like the Hero Digital Lending App on Google Play or the App Store) offer free credit report checks with no impact on your score.

Why Choose Hero FinCorp for Your Credit Needs?

Hero FinCorp, an RBI-registered NBFC, designs personal loans around real life with fast digital processing, transparent terms, and tenures that fit your budget. Whether your score is in the good range and you want quick funds, or you’re rebuilding and need a small-ticket loan to strengthen your profile, our process is hassle-free. You can check your eligibility in minutes without hurting your CIBIL score, and manage everything via Hero Fincorp, an award-winning lending app. Explore your personalised loan offer today.

Conclusion

Your CIBIL score range reflects your credit habits. It tells you how to build your credit score. First, know where you are. A higher score gets you places, a lower score just means you have a plan to rebuild. No matter your current range, Hero FinCorp’s digital tools help you take confident next steps.

Frequently Asked Questions (FAQs)

What is the difference between a CIBIL score and a credit score?

A credit score is available from any of the four bureaus, such as CIBIL, Experian, Equifax, and CRIF High Mark. A CIBIL score is a three-digit number given by TransUnion CIBIL.

Can a low CIBIL score affect my credit card approval?

Yes, it is possible. Most credit card companies want to see a CIBIL score of 650+.

How often should I check my CIBIL score?

You should check your CIBIL score every three or four months.

H3: Does closing credit accounts affect my CIBIL score?

Closing your card makes your credit history shorter and may lower your CIBIL score. Keep accounts active with small purchases.

H3: How long does a negative event stay on my credit report?

Late payments, defaults and settlements stay on your report for up to 7 years. They get less important over time as you do good things.

Can I improve my CIBIL score without taking a loan?

Paying credit card bills in full and on time while keeping utilisation low, and avoiding enquiries will raise your CIBIL score without a new loan.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Somewhere behind every loan application sits a name most borrowers never bother to ask about. Nine times out of ten it's CRIF, licensed by the Reserve Bank of India alongside just three others. Whatever they report back can be the difference between a quick yes and a frustrating delay, which is reason enough to figure out what CRIF actually is and how it compares to CIBIL.

If you’ve been wondering why my credit score is decreasing, the answer is usually linked to recent changes in how you use credit, repay loans, or how lenders report your activity.

Nobody thinks about their CIBIL score until a loan application is in front of them. By that point, years of high credit card utilisation, a couple of missed EMIs, or just never having borrowed at all have already shaped the number sitting in the bureau's records.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.