Debt Instruments: Meaning, Structure, and Types

Governments, private companies, and banks constantly need funds to build infrastructure, expand operations, or manage short-term cash flows. But how do these institutions raise money? The answer is debt instruments.

From government bonds, corporate debentures, to loans and commercial paper, debt instruments are crucial in today’s financial landscape for both investors and businesses.

Here’s a guide that breaks down everything you need to know about these financial tools.

What Is a Debt Instrument?

A debt instrument is a financial contract that represents a borrowing arrangement between two parties - the issuer (borrower) and the investor (lender). When a company or government needs capital, it can issue debt instead of selling ownership stakes. It is essentially borrowing money with a legal obligation to repay the principal amount along with the interest rate.

Let’s assume this example: if you borrow money from the bank for your home loan, it’s a debt instrument. Similarly, the Indian government issues Treasury Bills, and when big corporations issue bonds, these become debt instruments.

The terms of borrowing, such as interest rates, repayment schedule, and maturity date, are clearly defined upfront. Debt instruments have lower risk, making them attractive for conservative investors. However, they are different compared to equity instruments like stocks, as they offer ownership of the company but without any guaranteed returns.

In the Indian market, you will come across multiple forms of debt instruments like bonds, loans, debentures, fixed deposits, etc. These keep money circulating through the economy.

Key Features and Structure of Debt Instruments

Every debt instrument has a legal contract binding the issuer and lender. It specifies all the terms and conditions, protecting both parties. It’s essential to understand the structural components of debt instruments.

Legal Contract Binding the Issuer and the Lender/Investor

Debt instruments offer a structured, legally binding way to manage borrowing and lending without giving up ownership or control.

Interest Rate

Debt instruments come with fixed or floating interest rates. Fixed rates offer predictability, so you know exactly how much return you’ll earn. Floating rates are tied to market benchmarks, thus adjusting periodically and providing flexibility in changing economic conditions.

Maturity Period

This refers to when the issuer must repay the principal amount. Maturity period can be for short-term, from a few days to one year, whereas long-term can span several years to decades.

Security and Collateral

Some debt instruments are secured, meaning they’re backed by specific assets. Investors can claim these assets if the issuer defaults. On the other hand, unsecured assets have no such backing, thus making them riskier but offering higher returns.

Tradability

Many debt instruments can be purchased and sold in secondary markets. This allows investors to exit their positions before maturity.

Repayment Priority

If the issuer goes bankrupt, debt holders are given priority over equity shareholders. This structure provides creditors with better protection than equity investors.

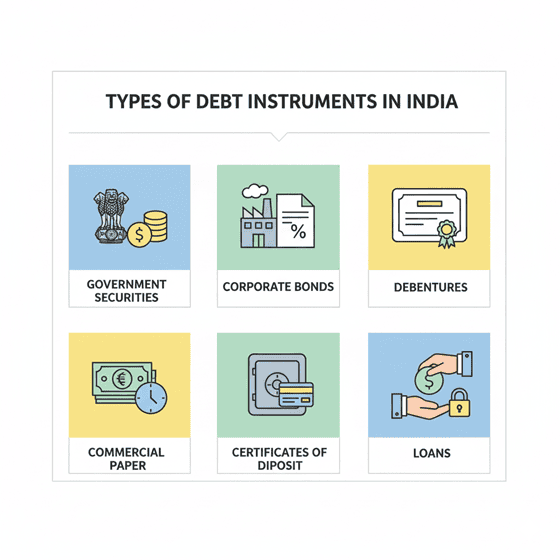

Types of Debt Instruments in India

The debt market in India offers various instruments tailored to various investor profiles, time horizons, and corporate needs.

1. Government Securities (G-Secs)

These are the safest debt instruments issued by the Government of India. This is done to finance public expenditure.

Treasury bills (T-Bills) are short-term instruments that mature in 91, 182, and 364-day maturities

Government bonds have longer maturities with variable interest rates

State governments also issue State Development Loans to fund development projects.

2. Corporate Bonds

- Companies issue corporate bonds to raise capital for expansion and projects. These are offered in three types:

- Secured or unsecured loans

- Convertible debentures (can be converted into equity)

- Non-convertible debentures (NCDs) are popular among retail investors in India

3. Commercial Paper

Commercial Paper is a short-term, unsecured debt instrument. It helps businesses handle their short-term liquidity demands and typically matures in 90 days.

4. Debentures

Non-banking entities issue debentures. These are also available as secured or unsecured.

5. Certificate of Deposit (CD)

Banks and financial institutions issue certificates of deposit against fixed interest and maturity dates. This makes them popular for those seeking a safe, short-term return.

6. Loans and Advances

Loans of any kind such as personal loan, business, and also credit lines from NBFCs and banks function as debt instruments.

Also Read: What Is Debt Management? Meaning and Plan Explained

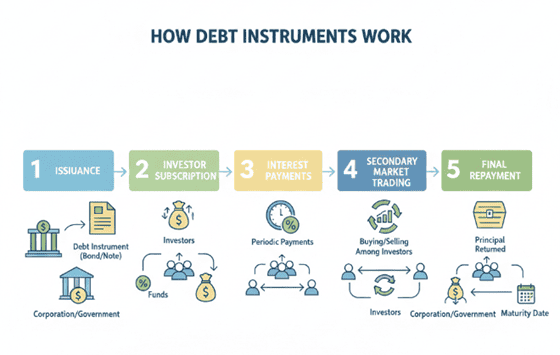

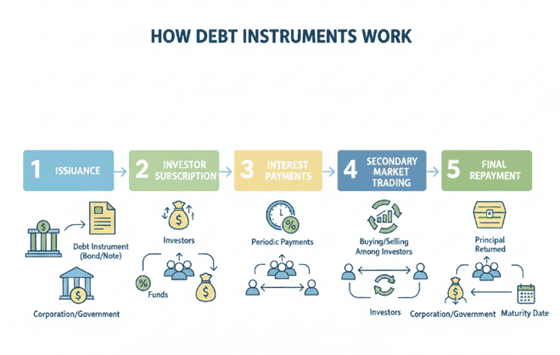

How Debt Instruments Work: Issuance, Trading, and Repayment

Debt instruments have a clear lifecycle.

1. The issuer decides to raise funds through borrowing rather than equity and takes help from investment banks or brokers.

2. The debt offering is prepared and then listed on exchanges like NSE and BSE.

3. Investors then subscribe to these instruments during the primary issuance phase.

4. Once issued, the instrument can be traded in secondary markets at prevailing market prices.

5. Issuers make periodic interest payments called coupons.

6. Upon maturity, the entire principal amount is paid to the investor.

This structure ensures transparency and predictability for both the borrower and lender.

Advantages and Disadvantages of Debt Instruments

Debt instruments come with advantages and disadvantages for both the issuer and lender.

Advantages

- Debt instruments offer predictable income streams through regular interest payments

- They have lower volatility compared to stocks

- Debt instruments offer priority repayments in case of default scenarios

- For issuers, debt instruments enable capital raising without ownership dilution

- They get tax benefits on interest expenses

Disadvantages

- Issuers can fail to repay, so there’s a chance of default risk

- Fluctuating interest rates affect prices

- Debt instruments offer limited upside compared to equity

Debt Instruments Examples Explained

Let’s assume you invest ₹1 lakh in a 10-year bond issued by the Government of India at 6.5% annual interest. You will receive ₹6,500 every year until maturity, when your full principal is returned. This shows a straightforward, low-risk nature of a debt instrument.

For short-term returns with minimal commitment, you can purchase a 91-day T-Bill or Commercial Paper. Large, reputable companies issue corporate bonds. Meanwhile, fixed deposits are a retail-friendly debt instrument.

You can invest in debt instruments through two main avenues: directly purchasing securities or investing via debt mutual funds. Choose the avenue depending on your risk appetite, investment horizon, and desired liquidity.

1. Debt Mutual Funds

This is the most common and convenient method for retail investors, as fund managers handle the investment decisions and diversification.

How to Invest:

1. Ensure your Know-Your-Customer (KYC) details (PAN, Aadhaar, bank details) are verified with a bank, Asset Management Company (AMC), or online platform.

2. You can invest via three platforms. So, choose among -

- Bank platforms (e.g., ICICI Bank, HDFC Bank)

- Online investment platforms/brokerage apps (e.g., Zerodha, Jiraaf)

- The AMC's website.

3. Choose a fund that aligns with your financial goals and risk tolerance. Options range from

- Low-risk overnight or liquid funds for short-term needs

- Higher-duration or credit risk funds for longer horizons and potentially higher returns

4. Decide between a lump sum investment or a Systematic Investment Plan (SIP) for disciplined investing, and complete the transaction online.

2. Direct Investment in Securities

For investors who prefer direct control over their assets, several government and corporate options are available.

Government Securities (G-Secs) and RBI Bonds

How to Invest: You can invest through the RBI Retail Direct Scheme platform or via brokerage platforms like the NSEGoBID platform or the Kite app.

Corporate Bonds and Non-Convertible Debentures (NCDs)

How to Invest: You can buy them through a Demat account on stock exchanges like the NSE or BSE, similar to buying shares. Platforms like Jiraaf also curate high-quality corporate debt opportunities.

Fixed Deposits, Corporate FDs, Public Provident Fund (PPF), and National Savings Certificates (NSC)

How to Invest: Invest in these debt instruments directly through banks or post offices.

Pro Tip - Always diversify the debt portfolio across issuers and maturities to mitigate risks effectively.

Role of NBFCs in Debt Instrument Financing

While large institutions often rely on bonds and market-linked securities to raise capital, individuals and small businesses typically need simpler, more accessible debt solutions. This is where Hero FinCorp plays an important role in the debt financing ecosystem.

We offer regulated, transparent loans to help borrowers meet real financial needs such as emergencies, education, or business expenses. The focus stays on clarity, flexible repayment options, and a smooth digital process, making structured borrowing easier to understand and manage.

Plus, simple eligibility checks, quick approvals, and a fully digital process make borrowing predictable and manageable.

If you are planning an expense or need timely funds, explore Hero FinCorp’s personal loan options today and apply with confidence.

Frequently Asked Questions

1. What is the difference between a debt instrument and a debt security?

There are many types of debt instruments, and debt securities are one type. All securities are instruments, but not all instruments are traded securities.

2. Are debt instruments safer than equity investments?

Yes. They offer fixed returns and priority repayments in case of default scenarios. However, they still carry some credit risk.

3. Can individuals invest directly in corporate bonds in India?

Yes, these are available through exchanges, brokers, and debt mutual funds.

4. What happens if the borrower defaults?

Secured debt instrument investors can claim the underlying assets. Unsecured investors may have to recover funds through legal proceedings.

5. How do credit ratings affect investments?

Higher ratings usually offer lower returns while indicating lower default risks. Low-rated instruments offer higher returns along with higher risks.

6. Can NBFCs issue debt instruments?

Yes, NBFCs regularly issue bonds, debentures, and commercial paper to raise capital.