Bad Debt: Meaning, Types, and How to Avoid It

Suppose you receive your salary on the first of the month. Within hours, a series of automated pings on your phone announces that a significant chunk of that hard-earned money has vanished. This way, you aren't investing in your future but paying for your past. This cycle is the reality of living with bad debt.

To use debt responsibly, it is important to understand that while some borrowing helps you climb the financial ladder, other types act as an anchor, dragging you down. Understanding the meaning of bad debt is the first step toward reclaiming your paycheck and your peace of mind.

What Is Bad Debt?

In finance, "bad debts" refers to money borrowed to purchase things that lose value quickly or do not generate any income. It is essentially expensive money used to fund depreciating assets.

Unlike a home loan, where the property value might go up, bad debt usually involves high interest rates for items that provide instant gratification but long-term financial stress.

Characteristics of Bad Debt

How do you spot the signs of bad debt? Here are the typical characteristics of bad debt:

| Characteristic | What it Looks Like | The Financial Impact |

|---|---|---|

| High Interest Rates | Rates that exceed 24% to 40% (like credit cards). | You end up paying back double or triple what you borrowed. |

| Depreciating Value | Used for things that lose value (gadgets, clothes). | You are still paying for an item that is already worth nothing. |

| No Income Potential | Funding a lifestyle choice rather than an asset. | The debt drains your monthly cash flow instead of building wealth. |

| Short-Term Use | Using a 3-year loan to pay for a 1-week vacation. | You are stuck with a long-term burden for a very brief experience. |

| No Tax Benefits | No deductions available under the Income Tax Act. | Unlike home loans, you get no government relief on the interest paid. |

Types of Bad Debts

Identifying the different types of bad debts helps you avoid financial landmines. Here are common examples of bad debt you might encounter:

High-Interest Credit Card Debt

Credit card bad debt is a major trap. You are trapped in a cycle of high-interest debt, where rates can surpass 40% annually, if you only make the required minimum payments. For instance, if you use a credit card to purchase a ₹50,000 laptop and don't pay it off right away, you might eventually have to repay twice as much.

Payday Loans and Title Loans

Payday loans are very short-term loans with astronomical interest rates meant to last until your next salary. Similarly, title loan debt involves pledging your vehicle as collateral for quick cash. Both are risky because one missed payment can lead to a debt spiral or the loss of your transport.

Debt for Depreciating or Non-Essential Assets

Taking on debt for depreciating assets like a car loan for a vehicle you can't truly afford is a common mistake. While a car is a utility, a luxury vehicle bought on high-interest credit is non-essential debt that loses value the moment it hits the road.

Gambling Debts and Impulse Purchases

Gambling debt is perhaps the most destructive, as it involves borrowing for high-risk activities with no guaranteed return. Similarly, impulse purchase debt from "flash sales" or "Buy Now Pay Later" schemes for things you didn't plan to buy can ruin a monthly budget.

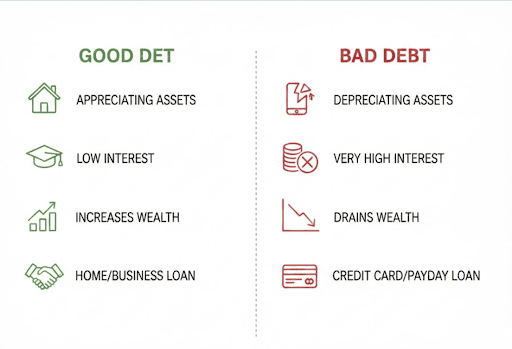

The Difference Between Bad and Good Debt

Here's a breakdown of the key differences between bad and good debt:

| Feature | Good Debt | Bad Debt |

|---|---|---|

| Asset Type | Appreciating (Home, Education) | Depreciating (Gadgets, Lifestyle) |

| Interest Rate | Low/Moderate | Very High |

| Future Wealth | Increases your net worth | Drains your net worth |

| Example | Home Loan, Business Loan | Credit Card, Payday Loan |

When "Good" Debt Can Turn "Bad"

Managing good debt is a delicate balancing act. Even the most productive loan can become a burden if not handled correctly.

For instance, if you take an education loan which is traditionally a "good debt," to pursue an MBA.

However, if you over-borrow to cover a luxury lifestyle during your studies and your starting salary cannot cover the massive EMIs, that is when good debt becomes bad. The debt changes from being a source of wealth to a danger to your financial stability the instant your loan repayments forced you to forgo necessary expenses like health insurance.

Why Avoiding Bad Debt is Crucial for Your Financial Health

To avoid bad debt is to give yourself a raise. Focusing on financial health debt management is vital because:

- Increases Liquidity: You have more cash available for investments.

- Protects Credit Score: Avoiding high-interest traps keeps your CIBIL score high.

- Compound Interest Works for You: Instead of paying interest to the bank, you earn interest through savings.

Also Read: CIBIL Score Range: Know Whether Your CIBIL Score is Good or Bad

Strategies to Avoid Falling into Bad Debt

Following a bad debt prevention plan is the best way to stay secure. Here is how to avoid bad debt:

- Make and Follow a Realistic Budget: Make sure your spending never surpasses your income by using a realistic budget. The best way to practise financial discipline is to create a budget to prevent debt.

- Create an emergency fund: Create a fund with six months' worth of costs. If you have emergency reserves, you won't have to take out a high-interest loan in the event of a medical emergency or job loss.

- Improve Your Credit Score: Practice good credit habits, like paying bills in full. A plan to improve your credit score ensures you get the best rates on "good" loans.

- Think Before You Borrow: Use responsible borrowing tips. Before taking a loan, evaluate debt by asking if the item will help you earn money or save money in the future.

Managing Existing Bad Debt: Hero FinCorp's Approach

If you are already struggling, effective debt management strategies Hero FinCorp suggests including:

- Debt Consolidation and Refinancing: Use debt consolidation loans to pay off multiple high-interest cards. To refinance bad debt into a single, lower-interest EMI makes repayment much easier.

- Seeking Professional Financial Guidance: If things feel out of control, financial counselling for debt can provide a structured path out. Debt relief services help negotiate terms you can actually manage.

Hero FinCorp: Your Partner for Smart Financial Decisions

A future free from bad debt is absolutely attainable. By focusing on solid financial planning and resisting the temptation of high interest and easy credit, you can direct your money toward your own goals, not just toward paying interest.

At Hero FinCorp, we are committed to helping you make the right moves. Whether you need Hero FinCorp debt solutions to consolidate high-interest bills or Hero FinCorp financial advice to plan your next big purchase, we provide the support you need to ensure your financial journey is smooth and productive. Get in touch with us for more info!

Frequently Asked Questions

What is the primary indicator of bad debt?

The primary indicator is a high interest rate on a loan used to purchase something like a gadget or vacation that loses value over time.

Can poor debt harm my credit score significantly?

Indeed, excessive credit card use and late payments on high-interest loans can seriously harm your CIBIL score, making it more difficult to obtain "good" loans in the future.

Is a student loan considered good debt or bad debt?

Since a student loan represents an investment in your future earning potential and often pays off over the course of your career, it is generally seen as positive debt.

Are credit cards always considered bad debt?

No, credit cards are just a tool if you pay the full balance every month. They only become bad debt when you carry a balance and pay high interest.

How can Hero FinCorp help me manage or avoid bad debt?

We offer personal loans for debt consolidation, allowing you to pay off multiple high-interest debts and replace them with a single, lower-interest monthly payment.

What is the debt snowball method vs. the debt avalanche method?

For psychological incentive, the snowball method emphasises paying down the smallest sum first. In order to save the most money, the Avalanche technique focuses on paying off the debt with the highest interest rate first.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.