UPI Lite vs UPI: Full Comparison for Indian Users

Digital payments have become second nature in India. Whether it’s buying a cup of chai or ordering electronics, you can do it all in a few taps no cash needed. UPI has been central to this shift. But now there’s UPI Lite, a simplified on-device wallet version for everyday small spends.

What’s the difference between UPI and UPI Lite? And which one should you use and when? Let’s break down the UPI vs UPI Lite differences clearly based on the latest 2025-2026 guidelines.

What is UPI?

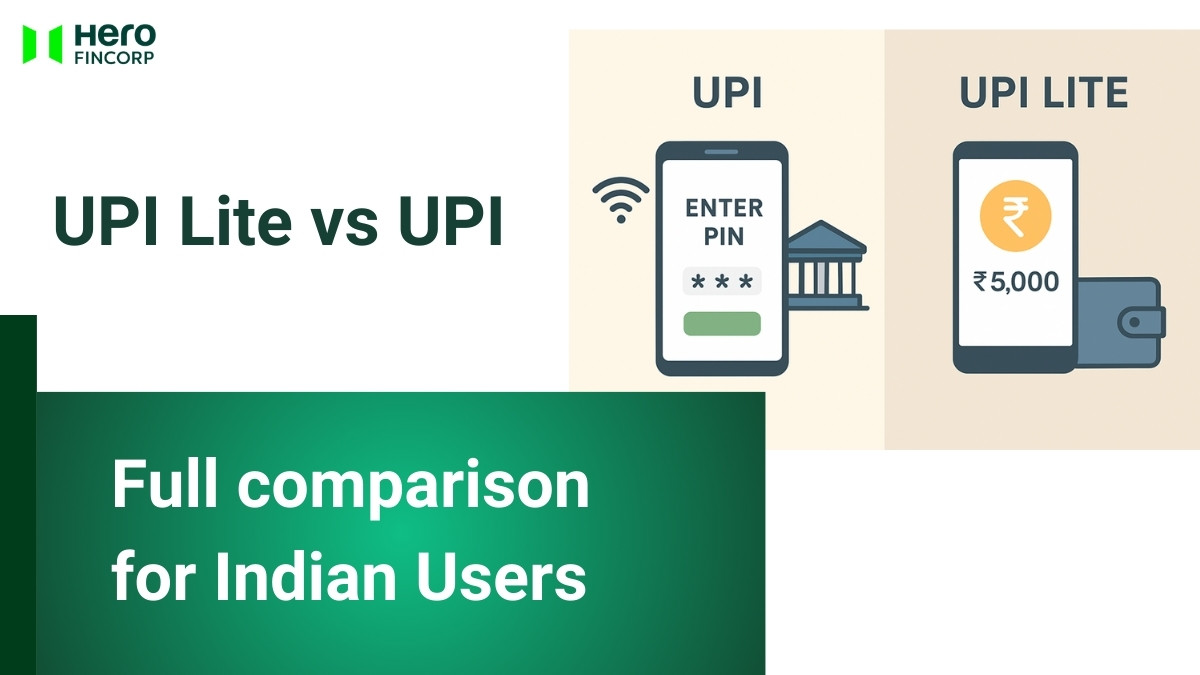

What is UPI? Unified Payments Interface (UPI) is India’s real-time, instant payment system developed by the National Payments Corporation of India (NPCI).

You can send or receive money directly from any bank account using your mobile app, without sharing sensitive account numbers. It handles everything from daily expenses to high-value transfers like rent and utilities. UPI is secure, available 24/7, and operates under the regulatory oversight of the Reserve Bank of India (RBI).

What is UPI Lite?

What is UPI Lite? It is a "on-device wallet" feature within your existing UPI app (like BHIM, Google Pay, or PhonePe).

Think of it as a mini-wallet. As per the RBI's October 2024 Monetary Policy Committee (MPC) announcement, the limits were enhanced to improve digital adoption . You can now load up to ₹5,000 into your wallet and pay instantly without entering a UPI PIN. Unlike standard UPI, UPI Lite works locally on your device, ensuring payments succeed even during bank server downtime or peak traffic.

Also Read: UPI Lite Transaction Limits

UPI vs UPI Lite: 6 Major Differences

At their DNA, the UPI and UPI Lite difference is minimal as both are digital payment methods, but they serve different transactional needs. Let’s break down the key differences as of January 2026.

| Feature | UPI (Standard) | UPI Lite |

| Transaction Limit | ₹1 Lakh (Standard); ₹5 Lakh for Taxes/Hospital/Education | ₹1,000 per transaction |

| Wallet/Daily Limit | No wallet; Daily limit usually ₹1 Lakh | ₹5,000 wallet limit; ₹10,000 total daily spend |

| PIN Requirement | Mandatory for every transaction | No PIN required for payments |

| Internet Need | Always Required | Can work offline (via UPI Lite X features) |

| Statement Clutter | Every transaction appears in bank passbook | Only wallet loading appears in passbook |

| Refunds/Credits | Direct to bank account | Direct to bank account (cannot receive to wallet) |

1. Transaction Limits

The standard UPI allows you to transfer up to ₹1 lakh per day for most P2P (Peer-to-Peer) transactions. However, for specific categories like Tax payments, Education, and Hospital bills, the limit has been enhanced to ₹5 lakh per transaction.

The UPI Lite vs UPI limits differ significantly for small-ticket items. The RBI recently increased the per-transaction limit for UPI Lite to ₹1,000, with a maximum wallet balance of ₹5,000 at any point to facilitate faster micro-payments.

2. PIN Requirement

With every UPI transaction, you’ll have to enter a secure 4 or 6-digit PIN. This adds a layer of safety but can feel cumbersome for small payments. UPI Lite skips the PIN step altogether, making the experience frictionless and faster for spends under ₹1,000.

3. Speed and Dependence

Since UPI connects to your bank’s core banking system (CBS) every time, it depends on bank server strength. This can cause "technical declines" during peak hours. UPI Lite resides on your device wallet, so payments are processed instantly, independent of bank server availability at the time of transaction.

4. Send or Receive?

UPI is fully two-way. You can send, receive, and request money. UPI Lite is currently a "debit-only" tool. You can only send money. Any refunds or incoming transfers cannot be credited to the Lite wallet; they will automatically go to your linked bank account.

5. Record-Keeping

Standard UPI transactions can clutter your bank statement with dozens of small entries (e.g., ₹10 for tea). UPI Lite keeps your bank statement clean, as only the "loading" of the wallet is recorded in your passbook, not the individual micro-spends.

6. Global Availability

UPI now works across several countries, including France, UAE, Singapore, Nepal, and Mauritius. UPI Lite is primarily focused on the domestic Indian market to streamline high-volume, low-value traffic.

Pay As You Like With UPI and UPI Lite

UPI Lite vs UPI the choice depends on your needs. UPI Lite is a great option for daily, small-value spending. It is fast and PIN-free. For larger payments or receiving funds, you can rely on traditional UPI.

If you require a larger financial cushion for emergencies or big-ticket purchases, Hero FinCorp (a regulated NBFC) offers Instant Personal Loans with transparent terms and digital processing. This ensures your high-value needs are met while your daily payments stay seamless via UPI.

Frequently Asked Questions (FAQs)

Is UPI Lite safer than UPI?

Both are highly secure. UPI uses PIN-based authentication, while UPI Lite limits financial exposure by capping the wallet balance at ₹5,000.

2. Can I use UPI Lite without internet?

Yes, UPI Lite is designed to support offline-like functionality for small payments. The advanced UPI Lite X variant further enables near-field offline payments between devices.

What happens if I lose my phone with UPI Lite balance?

Since UPI Lite is an on-device wallet, you should contact your bank immediately to block the account. Most apps also allow you to disable the wallet from another device or claim the balance via bank reconciliation.

Disclaimer: The information provided in this is for informational purposes only. While we strive to present accurate and updated content, travel conditions, weather, places to visit, itineraries, budgets, and transportation options can change. Readers are encouraged to verify details from reliable sources before making travel decisions. We do not take responsibility for any inconvenience, loss, injury, or damage that may arise from using the information shared in this blog. Travel involves inherent risks, and readers should exercise their judgment and caution when implementing recommendations.