Partial Settlement of Loans: Meaning and Impact on Credit Score

Missing a few EMIs can become stressful very quickly. When a lender suggests a “partial settlement”, it can feel like a practical way to regain control. You pay a reduced lump sum, the loan account is closed, and the immediate pressure eases.

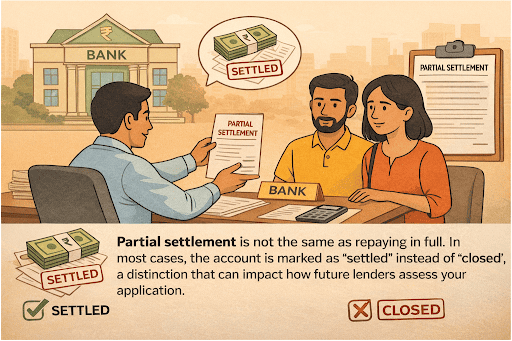

However, partial settlement is not the same as repaying your loan in full. In most cases, the account is reported as “settled” instead of “closed”, and that difference can influence how future lenders view your application.

Understanding Partial Settlement in Loans

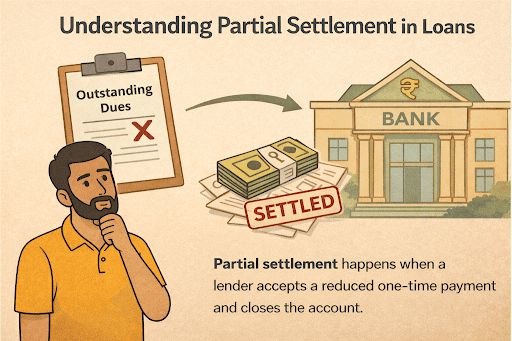

A partial settlement takes place when a lender agrees to accept an amount lower than the total outstanding loan and closes the account based on that payment. This usually happens when the borrower is unable to clear the full balance, and both sides agree on a one-time reduced payment to resolve the dues.

What is a Partial Settlement Loan in India?

The lender may agree to accept a reduced one-time payment and write off the remaining amount. Here is how it typically works in India:

- Negotiation with the lender: You request the lender to accept a reduced amount as a one-time payment

- Reduced lump-sum payment: The agreed amount is lower than your total outstanding loan

- Loan account closure: After payment, the lender closes the account

- Credit report update: The status is marked as “settled” instead of “closed” in credit bureau records

How Does Partial Approval Work for a Loan?

A partial approval occurs when the lender sanctions a lower amount than what you originally requested. For example, if you apply for ₹5 lakh and the lender approves ₹3 lakh after reviewing your income and credit details, ₹3 lakh is the final approved amount.

The Process of Partial Settlement

The partial settlement process typically begins when a borrower is unable to continue regular EMI payments and approaches the lender to discuss options. Once both sides agree, the borrower pays the negotiated amount in one instalment. The lender then closes the loan account and updates the credit bureaus with a “settled” status.

Negotiation and Agreement Terms

When you negotiate loan settlement, you and the lender agree on a reduced amount to close the loan. The terms should be clearly stated in a debt settlement agreement. Important points generally include:

- The final settlement amount

- The due date for payment

- How the account will be reported to credit bureaus

Documentation and Proof of Settlement

After completing the payment, request a settlement letter from the lender. This document confirms the agreed amount and states that the loan stands resolved under settlement terms.

You should also obtain a No Dues Certificate for partial settlement, which confirms that no further payment is pending.

Impact of Partial Settlement Loan on Your Credit Score (CIBIL)

When you close a loan by paying less than the total outstanding amount, the account is usually marked as “settled” on your credit report instead of “closed.”

Credit bureaus such as CIBIL treat a settled status as a sign that the original repayment terms were not fully honoured. The partial settlement credit score effect may include:

- A noticeable reduction in your credit score

- A “settled” remark that remains visible in your credit history for several years

- Greater scrutiny from lenders when you apply for new credit

- Possibility of higher interest rates or stricter approval terms

Also Read: Outstanding Loan Amount: Meaning & How to Find Out?

Immediate Drop in Credit Score

A credit score drop partial settlement occurs because the lender reports that the loan was not repaid in full as originally agreed. Your credit score may fall by 75 to 100 points in many cases, although the actual impact varies based on your repayment history and existing accounts.

Long-Term Repercussions on Future Loans

Getting a future loan after partial settlement may involve additional checks, leading to higher interest rates or requests for added security.

How Lenders View Partial Settlement

Lenders might reassess eligibility more strictly, review income stability in detail, or offer credit on conservative terms.

Alternatives to Partial Settlement

Common options include:

- Restructuring the loan to lower monthly EMIs

- Extending the repayment tenure

- Requesting a temporary payment pause, if permitted

- Taking a consolidation loan to manage multiple liabilities

Loan Restructuring/Rescheduling

Loan restructuring or loan rescheduling means revising the existing repayment plan so that EMIs become easier to manage. The lender may increase the tenure, adjust the EMI amount, or modify the interest terms based on your financial position.

Debt Consolidation Loan

Through a debt consolidation loan, different debts are combined into one account. This reduces the number of EMIs and may improve repayment efficiency based on the agreed terms.

Talking to Your Lender

If you expect trouble with repayments, reach out to your lender at the earliest. Most lenders offer digital platforms to check loan details and monitor EMIs. You can also use the Hero FinCorp personal loan app on Android or iOS to view your account, track payments, and stay updated.

Rebuilding Your Credit Score After a Partial Settlement

To improve CIBIL score after partial settlement, stick to simple, steady habits:

- Pay EMIs and credit card dues on time

- Maintain a low credit utilisation ratio

- Limit new loan applications within a short period

- Review your credit report regularly for accuracy

Make an Informed Decision on Loan Partial Settlement with Herofincorp

Partial settlement may ease immediate financial pressure, but it can affect your credit profile for years.

If you are planning your next financial step, Hero FinCorp offers personal loans with a quick digital process that can take as little as 10 minutes.

You can explore your personal loan options or use the personal loan eligibility calculator before you proceed.

Frequently Asked Questions

How long does a partial settlement stay on my CIBIL report?

A partial settlement can remain on your CIBIL report for up to seven years from the date of settlement.

Can Hero Fincorp offer a partial settlement option for my loan?

Hero FinCorp may consider a partial settlement in cases of genuine financial hardship, subject to internal review and policy terms.

Is partial pre-payment the same as partial settlement?

With partial pre-payment, you pay off part of the principal and continue the loan. In contrast, partial settlement ends the loan once a lower agreed amount is paid.

Will I get a No Dues Certificate after a partial settlement?

After you complete the settlement payment, the lender is expected to issue a settlement letter and a No Dues Certificate as proof of closure.

What is the minimum amount for a partial settlement?

There is no fixed minimum amount, as the settlement figure is negotiated based on your outstanding dues and the lender’s assessment.

How does partial approval differ from full loan approval?

Partial approval means the lender sanctions a lower amount than requested, while full approval means the entire applied amount is sanctioned.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.