Loan Closed but Active in CIBIL? Here’s What to Do

Rohit had just paid the final EMI on his personal loan and closed it. He now wants to apply for a home loan and checks his CIBIL report to ensure everything is in order.

He expected his personal loan to be in Closed status, but was surprised to see it active.

Finding a loan showing active in CIBIL even after it has been fully repaid is more common than you might think.

In this blog, we explain why a loan may still appear active in your CIBIL report even after closure and how to close active loans in CIBIL.

Understanding Loan Status in CIBIL Reports

You might be surprised to see a loan showing active in CIBIL even after you’ve repaid it.

When you get a loan, your bank or NBFC reports details like the loan amount, repayment history, and current status to CIBIL. Once the loan is fully repaid, the lender must update the status to “closed.” However, this update can sometimes be delayed or missed, resulting in an active loan status.

Why Does Your Loan Show Active Even After Closure?

There could be several reasons for an active loan status in your CIBIL report.

- Lenders usually report to credit bureaus monthly. The update might be pending if you recently repaid your loan.

- If the NOC or closure formalities are not properly executed, it may lead to an active status.

- The loan can remain active due to simple data-entry errors or internal processing delays.

- When you preclose your loan, any pending foreclosure fees might result in an active status.

- The status update may be delayed due to security deposit refunds, excess payments, or interest recalculations.

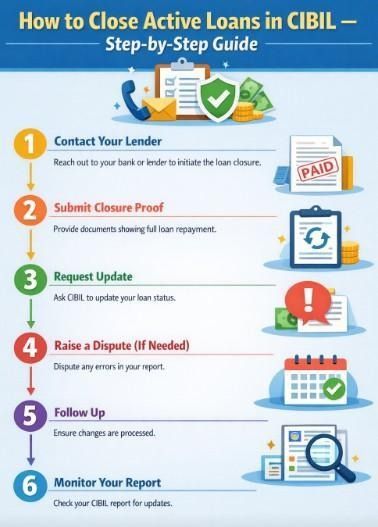

How to Close Active Loans in CIBIL- Step-by-Step Guide

If your personal loan shows active after closure, don’t panic. In most cases, it’s a minor issue, and here is how you can rectify it.

Step 1: Contact Your Lender

Reach out to customer care or your relationship manager and inform them that your loan is showing active in CIBIL.

Step 2: Submit Closure Proof

Provide your NOC, final repayment receipt, and loan closure letter. Request the lender to report your loan status to the credit bureaus in the next reporting cycle.

Step 3: File a Dispute

If the updated loan status is not reflected on your report, raise a dispute on the CIBIL portal with your closure documents.

Step 4: Monitor Your Report

Keep records of emails and complaints. Check every 10–15 days until the issue is resolved. Download your latest CIBIL report and check if your loan status is updated to Closed.

Loan Closed but Active Status: Common Issues

When you close a loan, but it remains in active status, you might face some issues like

- Delays in foreclosure payment processing

- Small unpaid charges or penalties

- Interest recalculations

- Gaps in reporting between lenders and credit bureaus

- Reporting cycle mismatches

These issues are usually temporary, but they should not be ignored. The longer an incorrect status stays, the more it can affect your financial profile.

Impact of Incorrect Loan Status on Your Credit Score

A loan showing active in CIBIL when it’s actually closed can negatively affect your credit profile. Lenders reviewing your application may think you still have ongoing debt, which increases your debt-to-income ratio and may reduce your loan eligibility.

An incorrect active status can also:

- Lower your credit score

- Make approvals slower or lead to higher interest rates

- Create confusion in your financial history

Your credit report reflects your financial discipline. That’s why you should check your report regularly and fix any problems immediately.

Take Control of Your Credit Before Your Next Loan Application

If the loan you closed still appears as active on your CIBIL credit report, coordinating with your lender to obtain the relevant documents and following up can help ensure your credit report is up to date.

Having an up-to-date credit file will help protect your score and prevent delays when applying for future loans. If any of your loans with NBFCs, such as Hero FinCorp, still appear as active on your credit report after closure, contact their customer care at the earliest and request a bureau update.

If you are thinking about another loan, consider a Personal Loan from Hero FinCorp with flexible tenures and hassle-free processing. You can download and apply through the instant loan app, but make sure your credit report shows the “Closed” status to not delay any approvals.

Frequently Asked Questions

1. How long does it take for my loan to show as closed on my credit report?

Usually, it takes 30-45 days after the full repayment. However, this may vary depending on how quickly the lender reports the update.

2. What documents do I have to collect after loan closure?

Get the NOC/loan closure letter, final payment receipt and a statement of account reflecting nil balance.

3. How can I challenge an incorrect status of an active loan on my CIBIL report?

You may raise a dispute on the CIBIL website or check with your lender to update your status.

4. Can my active loan status after closure affect my credit score?

Yes, it may affect your score if the loan is still active.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.