How to Complaint UPI Transaction – Step-by-Step Guide

The following scenarios are something you must have experienced or can definitely relate to. The first: you place an order on Zomato or Swiggy, you select UPI to pay, and enter your PIN. The money gets deducted for you, but does not get registered on the app.

Or, you want to send money to a friend or a family member, but end up sending it to someone else entirely. In both scenarios, the most common reaction anyone has is, "What now?", followed by, "Will I or how can I get my money back?"

This post will answer both questions for you. It will walk you through how to raise and check the UPI complaint's status without having to run from pillar to post.

Understanding UPI and Its Common Transaction Issues

The UPI system of payments, while extremely convenient and popular, does encounter issues now and again. The following are the most common of the lot -

Failed Transactions

A failed transaction is when the money gets deducted from your account, but never reaches the recipient. This could either happen due to the bank's servers being down, a loss of internet connectivity mid-transaction, or a technical glitch. At times, payments can even get stuck at the "Pending" stage.

Misdirected Payments

The UPI system uses Virtual Private Addresses (VPA) to send and receive money. They usually follow one of two formats: use a phone number or a customer name before the designated UPI App's or bank's suffix. Eg: 8754865788@okicici or agputa@okicici.

Now, suppose you make a mistake and type one wrong digit or alphabet that corresponds to a different registered VPA, the payment now goes there instead.

Fraudulent Transactions

These occur when bad actors get access to your UPI credentials and misuse your UPI or when they trick you into making wrong payments as part of an elaborate scam.

Your only option to recover your money in these cases is by filing a wrong UPI transaction complaint.

Why Is It Important to File a UPI Complaint?

There are two primary reasons why it's important to file a UPI-compliant -

1. You can get your money back.

The National Payments Corporation of India (NCPI), the governing body of the UPI system in India, has set a 45-day window from the transaction date to raise disputes for most issues. Cross this and recovering the money you have lost becomes next to impossible.

2. Each dispute triggers an investigation.

This, in turn, brings to light gaps in the systems being exploited by fraudsters and potential issues within the system that are causing failed transactions. It helps improve and secure the UPI system as a whole.

Also Read: Registering a UPI Complaint Online: A Complete Guide

How to Raise a Complaint for UPI Transactions?

You have three primary avenues to raise a complaint for UPI transactions.

Via your UPI App (Google Pay, PhonePe, Paytm, BHIM)

Raise a complaint for a wrong or fraudulent transaction that occurred via a UPI app. Do this -

- Step 1 - Open your UPI app and go to transaction history. This can either be called a passbook, depending on the app.

- Step 2 - Find and select the problematic transaction.

- Step 3 - Then, select the following action: "Report Issue," "Get Help," or "Raise a Dispute." Menu labels vary by app.

- Step 4 - Choose your complaint type, describe what went wrong, and submit.

- Step 5 - Save the complaint reference or ticket number. You'll need this to track progress.

Ideally, failed UPI transactions should get auto-reversed the next day. In the case of failed merchant transactions, the limit is 5 days. Beyond that, banks must compensate you ₹100 per day of delay. However, please note that disputes or fraud cases can sometimes take weeks.

Register a Complaint on the NPCI Portal

If, after 7 days, you see no resolution for your complaint, escalate to NPCI like so -

Step 1 - Head to the Dispute Redressal URL on the NCPI portal.

Step 2 - Enter the information as requested. This includes the transaction ID, date/time, amount, bank details, account number, and a detailed description of what happened.

Step 3 - Submit and note your Complaint Registration Number (CRN). NPCI forwards this to your bank, which must respond within regulatory timelines.

Raise a Complaint Through Your Bank's Customer Care

Step 1 - Call your bank's toll-free customer care and select the UPI/digital payment option from the IVR.

Step 2 - Explain your issue with full transaction details.

Step 3 - Request formal complaint registration and note the reference number.

Step 4 - Follow up via email to your bank's grievance email address.

Step 5 - If unresolved within 7 days, escalate to the bank's nodal officer (contact details on their website).

For the most effective results, do all three simultaneously. If you do not see any progress happening on your complaint, raise the case with RBI's ombudsman.

How to Raise a Wrong UPI Transaction Complaint?

If money is transferred to the wrong account through UPI, you can raise a wrong UPI transaction complaint through the NPCI dispute portal.

- Visit the official NPCI website and open the UPI section.

- Select “Dispute Redressal Mechanism.”

- Click “Transaction” under Complaint.

- Choose the issue type.

- Select “Incorrectly transferred to another account.”

- Enter payment details, bank name, amount, date, and contact information.

Submit the complaint for review and resolution and save the wrong UPI transaction complaint number.

Also Read: CRN Number: Meaning & How to Find It

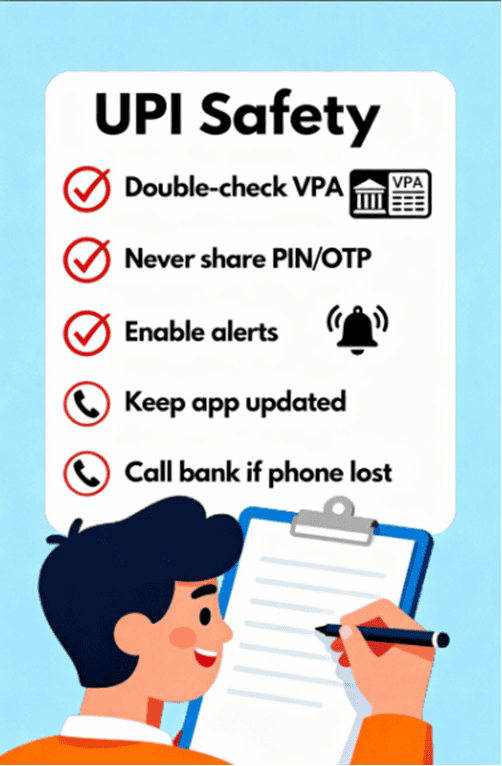

Tips to Prevent UPI Transaction Issues and Frauds

Here are a few simple tips to help prevent future issues when making UPI transactions -

- Double-check the VPAs before sending funds. If you are unsure, send ₹1 first.

- Never share your UPI pin or any UPI-related OTPs with anyone. Avoid easy-to-guess UPI Pins.

- Always enable transaction alerts for UPIs as well as others (debit and credit card transactions and fund transfers).

- Always keep your UPI apps updated to the latest version.

- Call your bank to block UPI services the moment your phone is stolen or as soon as you realise it's lost.

Also Read: Is It Safe to Share Your UPI ID? HeroFinCorp Guide to UPI ID Safety

Getting Your UPI Issues Resolved With Confidence

Even though most UPI issues get resolved, the delay can still cause stress, especially when the payment was meant for something urgent. Pending refunds or blocked payments shouldn’t leave you stuck.

If you need funds while your UPI complaint is being sorted out, Hero FinCorp’s personal loans can help you bridge the gap. Apply in minutes through the digital app, get instant approval, and receive funds the same day, so you never have to pause your plans.

Conclusion

UPI transaction issues can feel stressful, but quick action improves the chances of faster resolution and fund recovery. By reporting problems through your app, bank, or NPCI portal and following safe payment practices, you can protect your money and use digital payments with greater confidence and peace of mind.

Frequently Asked Questions

How long does it take to resolve a UPI complaint?

Most UPI complaints are solved within a couple of days. However, in the event of fraud or if money has been sent to the wrong recipient, the timeline can go up to 90 days in some cases.

Can I get my money back if I sent it to the wrong UPI ID?

In these cases, everything depends on the recipient. If they return the funds voluntarily, well and good; else, it's a long-drawn legal process with no guarantees.

How can I escalate if the app or bank does not resolve my UPI complaint?

In such cases, your first step should be to escalate to your bank's nodal officer first. If the case is still unresolved after 30 days, file it with the RBI's Banking Ombudsman.

Do I need to file separate complaints with the bank and NPCI?

Ideally, file the complaint via your UPI app and bank first. If unresolved in 7-10 days, then file with NPCI.

What is an RRN number in UPI, and where can I find it?

RRN is a unique transaction reference number. You can find it in transaction history, SMS alerts, or bank statements.

How do I check the live status of an open UPI complaint online?

Check your complaint status through the UPI app, NPCI portal, or your bank’s grievance tracking section.

What should I do if my bank or UPI app rejects my transaction dispute?

You can escalate the dispute to NPCI or the RBI Ombudsman if your bank or app rejects the complaint.

How can I locate the direct customer care lines for specific platforms like BHIM UPI?

Visit the official BHIM UPI or bank website for verified customer care numbers and grievance contact details.

Can I complain directly to the RBI if my wrong UPI payment remains unresolved?

Yes, you can approach the RBI Ombudsman if the complaint remains unresolved after following proper escalation channels.

What happens if I accidentally input an incorrect UPI ID and the payment clears? Can the bank auto-reverse it?

No, banks usually cannot auto-reverse successful payments. You must raise a complaint immediately for recovery assistance.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.