Call Money vs Notice Money: Key Concepts and Differences

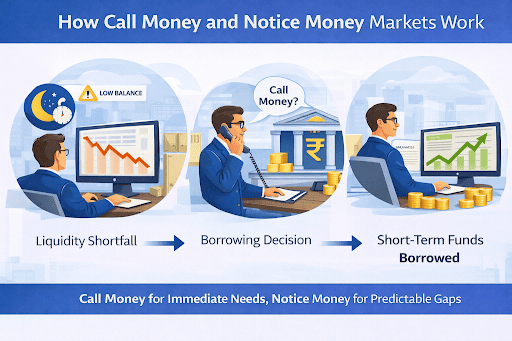

Imagine being in a bank’s treasury team and making large payments earlier than expected. The cash balance at the end of the day is running low. You need to arrange short-term funds immediately to stay compliant. This is where call money is used. However, if the gap is for a few days, notice money comes into play.

Understanding call money vs notice money helps you see how banks manage daily liquidity gaps without disrupting operations.

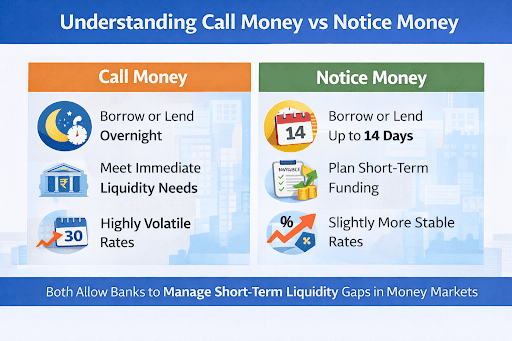

What is Call Money?

It refers to overnight borrowing and lending between banks and eligible financial institutions to meet very short-term liquidity requirements. The loan is repayable on demand or the next working day.

What is Notice Money?

It is similar to call money but with a slightly longer tenure. Funds are borrowed for up to 14 days. This option is used when liquidity needs extend beyond overnight but remain short-term.

Notice money allows short-term planning without locking funds for long periods. It is useful for making quarter-end adjustments or settling mismatches.

Key Differences Between Call Money and Notice Money

| Aspect | Call Money | Notice Money |

|---|---|---|

| Typical tenure | Overnight or 1 day | Up to 14 days |

| Purpose | Immediate liquidity needs | Short-term liquidity planning |

| Rate volatility | Highly volatile | Slightly more stable |

| Repayment | On demand / next day | As per the agreed notice period |

| Use case | Sudden cash shortfall | Planned short-term funding |

Call money is used when funds are needed immediately and only for a day. Notice money is suitable for situations where liquidity gaps are predictable for a few days.

Call Money Rate and Its Significance

The call money rate is the cost of borrowing funds overnight in the interbank market. Call money rates rise quickly when liquidity is low. When surplus liquidity exists, rates tend to fall.

Tracking rates can give you an idea about the conditions of short-term liquidity in the banking system. Sudden spikes indicate tight liquidity due to tax outflows, quarter-end requirements, or policy actions.

Also Read: Difference Between CRR and SLR

Functions of Call Money and Notice Money Markets

Call money and notice money markets support daily liquidity management in practical ways:

Helping meet reserve requirements

If end-of-day balances fall below regulatory requirements due to large withdrawals or settlements, short-term borrowing through call money helps bridge the gap until inflows arrive the next day.

Smoothing short-term cash mismatches

Call money covers overnight gaps, while notice money helps when the shortfall is expected to last a few days. For example, large customer payments may be scheduled for the next day while outflows happen today.

Supporting settlement of interbank transactions

Interbank settlements can create sudden liquidity needs. Short-term funds from call and notice money markets help complete settlements on time without disrupting operations.

Acting as a channel for monetary policy transmission

Call money rates fluctuate with any changes in RBI liquidity. They rise quickly when liquidity is tight, which shows higher short-term funding costs across the system.

Providing pricing signals for short-term funds

Movements in call money and notice money rates reflect real-time demand and supply of funds, helping banks price short-term borrowing more accurately.

Participants in Call and Notice Money Markets

Participants include scheduled commercial banks, co-operative banks, and certain financial institutions permitted by the regulator.

Banks with surplus funds lend in these markets, while banks facing shortfalls borrow.

Advantages and Disadvantages of Call Money and Notice Money

| Aspect | Call Money & Notice Money |

|---|---|

| Quick access to funds | Immediate access to short-term liquidity |

| Regulatory and operational support | Helps meet reserve requirements and complete daily settlements on time |

| Settlement efficiency | Supports smooth settlement of interbank transactions without delays |

| Liquidity signals | Reflects real-time demand and supply of short-term funds in money markets |

| Rate volatility | Rates can move sharply, especially in call money during tight liquidity |

| Market dependence | Availability and pricing depend on overall liquidity conditions |

Practical Examples: Call Money vs Notice Money Transactions

Take an example where you have made an unexpected settlement, but end-of-day outflows exceed inflows by ₹150 crore. Customer inflows are expected the next morning. Call money can cover this one-day gap, and you can repay when funds arrive.

In another scenario, payments of ₹300 crore are due over the next three days, but inflows are expected only after four to five days. Notice that money helps arrange funds for a few days.

Summary

Call money and notice money can help you manage short-term liquidity in the banking system.

Understanding call money vs notice money can help you choose the right funding option based on urgency and duration. It also interprets short-term interest rates in money markets.

Frequently Asked Questions

1. What is call money in banking?

Call money refers to the borrowing and lending of funds between banks to meet overnight liquidity needs.

2. How long is the tenure of call money and notice money?

Call money is for overnight use. But notice that money is for managing cash for up to 14 days.

3. Who can lend and borrow call and notice money?

Banks and eligible financial institutions participate in these markets in accordance with regulatory guidelines.

4. Why do call money rates fluctuate frequently?

Rates change based on daily liquidity conditions, tax outflows, settlements, and policy actions.

5. How do call money and notice money affect bank liquidity?

They provide short-term funding options that help banks manage daily liquidity gaps.

6. Are call money and money at call the same?

Yes, they refer to overnight funds repayable on demand.

7. What is the difference between call money and term money?

Term money extends beyond 14 days, but call money is overnight.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.