Advantages and Disadvantages of EMI: What You Should Know

When one takes a loan, they become subject to an EMI, which is paid monthly. At first, paying in instalments can be manageable and comfortable.

After a few months, the same EMI will be occupying a place in your budget right next to rent, groceries and other daily items. At this point, EMIs indicate both sides of the story. They enable major purchases but also create recurring monthly obligations.

The knowledge of the pros and cons of EMI makes you understand when the EMIs are in your favour and when you need to plan them more thoroughly.

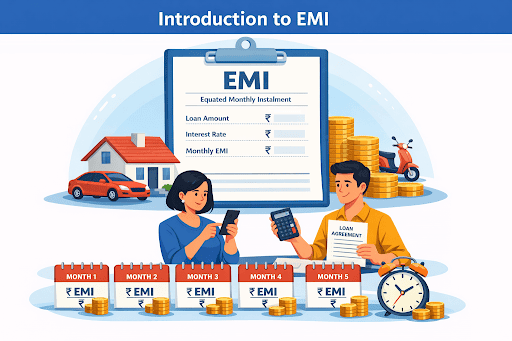

What is EMI?

EMI or Equated Monthly Instalment is the amount you pay monthly to clear a loan. This sum consists of the loan principal and the interest on the loan. EMIs are applied to personal loans, vehicle loans, home loans and most high-value purchases.

EMIs make repayments orderly, as you are sure of the amount to be disbursed on a monthly basis. This predictability helps you to plan your monthly finances easily because your income is constant. Meanwhile, an EMI is an unchangeable obligation in your budget as long as the loan is not completely paid off.

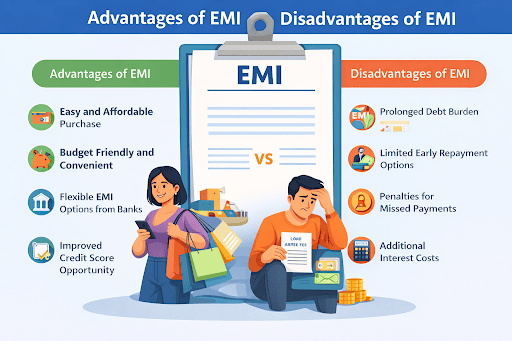

Advantages of EMI

Easy and Affordable Purchase

EMIs enable the management of the high costs to be paid without incurring the total cost at once.For example, a purchase worth ₹1,20,000 can be repaid in EMIs of around ₹5,500 to ₹6,000 per month over 24 months. This makes essential or planned purchases more accessible without draining savings in one go.

Budget Friendly and Convenient

Fixed EMIs offer certainty to monthly expenditure. For instance, if the monthly EMI is ₹7,000, it can be budgeted each month rather than dealing with irregular, high one-time payments.

Flexible EMI Options from Banks

Numerous lenders provide flexibility in the tenure and EMIs depending on income levels. A ₹2,00,000 loan can be repaid in 12 months with a higher EMI, or in 24 or 36 months with a lower monthly payment.

Improved Credit Score Opportunity

On-time EMI payments help to build a good repayment history. To illustrate, regular payment of EMIs within 6 to 12 months demonstrates financial discipline, which will reflect on your credit profile.

Disadvantages of EMI

Prolonged Debt Burden

EMIs offer months or years of repayment, which means being in debt longer. For instance, a ₹1,50,000 loan spread over 36 months may feel light monthly, but it creates a fixed obligation for three years.

Limited Early Repayment Options

Some loans have restrictions or charges for premature closure. Although financial conditions improve, prepayment expenses may offset the advantage of paying off a loan early, making it more difficult to become a debt-free borrower.

Penalties for Missed Payments

Missed or late EMIs incur penalties, additional interest, and a lower credit score, and repeated defaults can make future loans more expensive or trigger recovery action.

Also Read: What Will Happen If A Personal Loan EMI Bounces?

Additional Interest Costs

An EMI payment increases the purchase cost, as interest accrues over the tenure. For example, a ₹1,00,000 loan may end up costing more than ₹1,10,000 or ₹1,15,000 over the tenure, depending on the interest rate and tenure.

Summary: Is EMI Right for You?

EMIs can help you to handle large expenses without depleting your savings. They are convenient, have regular repayments, and they also enable you to create your credit profile. Meanwhile, EMIs will be calculated from a portion of your monthly earnings and will include interest.

EMIs are good when your salary is regular, and you can comfortably carry the commitment. Accepting EMIs without considering long-term affordability may silently tax your pocket over the years.

If you need money to cover planned or unforeseen costs, exploring loans and eligibility options can help you proceed with greater confidence. You can start by checking eligibility through Hero FinCorp’s official journey here.

Also Read: What is no-cost EMI and does it actually work in your favour?

Frequently Asked Questions

Can EMIs affect your credit score negatively?

Yes. Missed or late EMIs may reduce your credit rating. Timely payments favour a good credit history.

Are EMIs available for all types of loans and purchases?

Most personal, vehicle, and home loans are available in the form of EMIs, but they depend on the policies of the lender and the borrower's eligibility.

How can you reduce the interest burden while paying EMIs?

Reducing the total interest paid can be achieved by selecting shorter tenures, ensuring a good credit score before borrowing and making part-prepayments where possible.

What happens if you default on an EMI payment?

Late fees may apply, and repeated defaults can affect your credit score and lead to recovery processes.

Can you switch EMI plans during the loan tenure?

Some lenders allow tenure changes or part-prepayments, depending on loan terms and applicable charges.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.