How a 725+ CIBIL Score Helps You Get a 5 Lakh Loan at Lower Interest

A personal loan of ₹5 lakh is often taken for home repairs or medical expenses. The interest rate on the fixed loan amount may vary depending on your requirements.

The difference in interest rates will affect your CIBIL score. A high CIBIL score helps bring down the 5 lakh personal loan interest rate, making it more affordable.

Interest Rate In India On A 5 Lakh Personal Loan

The interest on a 5 lakh loan in India is from 10% to 24% per annum. It varies based on factors such as income stability, credit score, and the lender's policies.

The EMI on a 5 lakh loan for 3 years at an interest rate of 11% is about INR 16,300. At an interest rate of 18%, the EMI increases to about INR 18,100.

Why Is It Necessary To Get A 725+ CIBIL Score For A 5 Lakh Loan?

A 725+ CIBIL score is considered a strong benchmark by lenders. This score indicates repayment behavior and low credit risk.

From a lender’s perspective, a borrower with a score over 725 is considered reliable. It reduces uncertainty, and borrowers get a better term.

How Does Your Credit Score Influence The Interest Rate for a 5 Lakh Loan?

Risk-based pricing is a general concept used by lenders. It means the interest on a 5 lakh loan is adjusted based on the borrower's risk.

The higher score shows:

- Timely repayments

- Controlled credit usage

- Lower probability of default

These reasons allow the lenders to reduce the risk premium added to the base interest rate.

Comparative Analysis: 5 Lakh Loan Interest For Different CIBIL Brackets

| CIBIL score range | Estimated rate of interest | Risk level |

| Below 650 | 18% to 24% | High |

| Between 650 and 749 | 13% to 18% | Moderate |

| 725+ | 10% to 18% | Moderate |

The shift from 725 to 760 reduces the total interest burden over time.

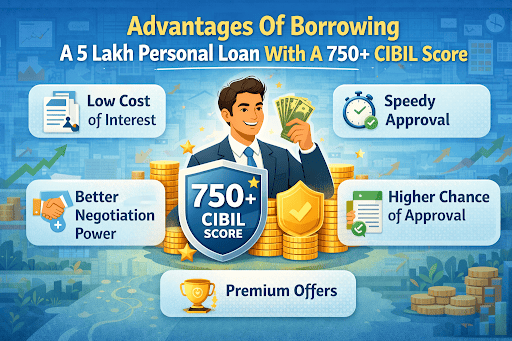

Advantages Of Borrowing A 5 Lakh Personal Loan With A 725+ CIBIL score

A high credit score lowers the loan interest rate. Some other benefits of taking a loan with a 725+ CIBIL score are:

1. Low Cost of Interest

The reduction in the rate of interest of 2 to 3% saves between ₹ 40,000 and ₹ 70,000 in the full loan tenure.

2. Speedy Approval

Borrowers with a high CIBIL score often get fast approvals with minimal verification.

3. Better Negotiation Power

Lenders offer flexible tenures and lower charges to borrowers.

4. Higher Chance of Approval

Applications are less likely to be rejected because of low risk.

5. Premium Offers

Many lenders offer instant loans to borrowers with high credit scores.

Estimation Of Monthly Outflow: 5 Lakh Loan Interest Per Month

The EMI of a 5 lakh loan depends on the interest rate and tenure.

- At 11% for 3 years- EMI- ₹ 16,300

- At 15% for 3 years- EMI- ₹ 17,300

- At 18% for 5 years- EMI- ₹ 12,700

Longer tenure reduces EMI and increases total interest paid.

Impact Of Tenure On Your Total Interest Payable

A shorter tenure of 3 years includes higher EMIs but lower overall interest. A 5-year tenure reduces the monthly burden but increases the total repayment.

A 5 lakh loan at 18%:

- 3 years- ₹ 1 lakh interest

- 5 years- ₹ 2.1 lakh interest

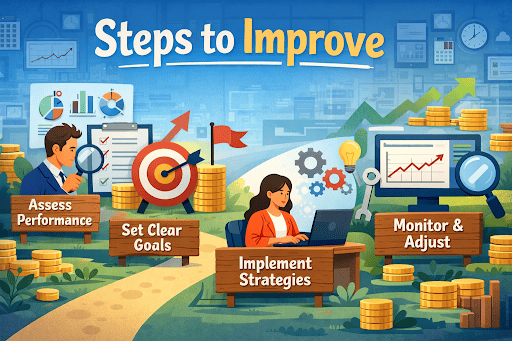

Steps To Improve The Score If It's Below 725

Improving a credit score is a gradual but profitable process. The steps to make the credit score better are:

- Paying EMIs and credit card bills on time

- Maintaining a credit utilisation below 30%

- Do not apply for multiple loans in a short period

- Check the credit report for errors and correct them

Following these steps for 3 to 6 months shows improvement.

Other Factors That Affect The Rate Of Interest Beyond CIBIL

Even though the CIBIL score is important, some other factors also affect the rate of interest, such as:

Income Stability

Regular income gives borrowers confidence to repay their loans.

Employer Profile

Employees working in reputed companies improve their eligibility.

Debt-to-Income Ratio

Lenders will adjust terms if existing EMIs increase by 40-50% of income.

Why Choose Hero Fincorp For An INR 5 Lakh Personal Loan?

Hero FinCorp offers a streamlined, transparent loan system for individuals with strong credit profiles.

You must check eligibility before applying for a loan. It helps to avoid rejection of the loan application. You can explore options through Hero FinCorp’s official journey here.

Conclusion

A loan of ₹5 lakh may seem straightforward, but the interest rate varies based on the credit profile. A CIBIL score of 725+ improves approval chances and reduces the overall cost of borrowing.

Frequently Asked Questions

What is the minimum CIBIL score for a 5 lakh loan?

Most lenders choose 700+, while the score of 725+ provides better interest rates.

How does a score of 725+ decrease the interest rates?

This score indicates a lower risk and helps lenders offer competitive pricing.

What are the processing fees for borrowers with a high score?

Fees vary depending on the borrower. The individuals with strong profiles may pay lower fees.

How is the rate of interest calculated on a 5 lakh loan?

The interest rate is calculated based on the interest rate, principal, and tenure using EMI formulas.

Can a borrower check their CIBIL score often?

Yes, the frequent checks can be done by a borrower.

How quickly can a 5 lakh loan be disbursed?

Disbursements for eligible profiles will occur within a few hours to two days.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.