5 Lakh Personal Loan EMI: Monthly Payment, Calculation, and Interest Rates

- Understanding Your 5 Lakh Personal Loan EMI

- How to Calculate EMI for Personal Loan of 5 Lakhs?

- The Mathematical Formula Behind EMI Calculation

- 5 Lakh Personal Loan EMI for Different Tenures (1 to 3 Years)

- 4 Factors Influencing Your 5 Lakhs Loan EMI

- Comparison of 5 Lakh Personal Loan EMI Across Top Lenders

- Eligibility Criteria for a ₹5 Lakh Personal Loan

- Benefits of Choosing Hero FinCorp for 5 Lakh Personal Loan

- How to Apply Online for a 5 Lakh Personal Loan?

- Plan Your EMI Like You Plan Your Monthly Budget

- Frequently Asked Questions

Aman was planning to take a ₹5 lakh loan to cover some immediate expenses at home. However, he had a few questions in his minds like how much EMI to pay every month and will he be able to pay them along with other expenses.

He sat down and looked at his rent, bills, and daily spending. That is when he understood that the real decision was about the EMI, not just the loan amount. Once he saw the exact number, things started to make sense. This blog explains how EMI works, how to calculate it, and what you should check before you decide.

Understanding Your 5 Lakh Personal Loan EMI

Before taking a loan, the first thing you should look at is your monthly outflow. Your 5 lakh personal loan emi is the fixed amount you pay every month until the loan closes. It includes both principal and interest, so you know exactly what leaves your account each month.

Most people check this in advance using a personal loan emi calculator. It gives you a clear idea of your monthly payment for 5 lakh loan and helps you avoid surprises later.

How to Calculate EMI for Personal Loan of 5 Lakhs?

You can calculate EMI on your own, but it takes time and careful calculation. That is why most borrowers prefer using the Hero FinCorp personal loan EMI calculator to get quick results.

Here are the details you need:

Loan amount = ₹5,00,000

Interest rate = 18% per year

Tenure = 36 months

You just have to enter the value, and the calculator will give you the EMI amount and total repayment within a second. It makes the comparison task easier as you can check different tenure options before applying.

The Mathematical Formula Behind EMI Calculation

EMI = P × R × (1 + R)^N ÷ ((1 + R)^N − 1)

Where:

P = Loan amount

R = Monthly interest rate

N = Number of months

Now let’s plug in the numbers:

P = 5,00,000

R = 18 ÷ 12 = 1.5 percent = 0.015

N = 36

EMI = 500000 × 0.015 × (1.015)^36 ÷ ((1.015)^36 − 1)

Final EMI ≈ ₹18,072

Interest here is calculated on a reducing balance basis, so the interest portion reduces as your loan balance decreases.

5 Lakh Personal Loan EMI for Different Tenures (1 to 3 Years)

Loan tenure changes everything. A shorter tenure increases your EMI but reduces the total interest you pay. A longer tenure does the opposite.

At 18% interest:

| Tenure | EMI | Total Interest |

| 1 Year | ₹45,843 | ₹50,116 |

| 2 Years | ₹24,978 | ₹99,472 |

| 3 Years | ₹18,072 | ₹1,50,592 |

Looking at this side by side makes the decision easier. You can choose what feels comfortable every month instead of focusing only on total cost.

4 Factors Influencing Your 5 Lakhs Loan EMI

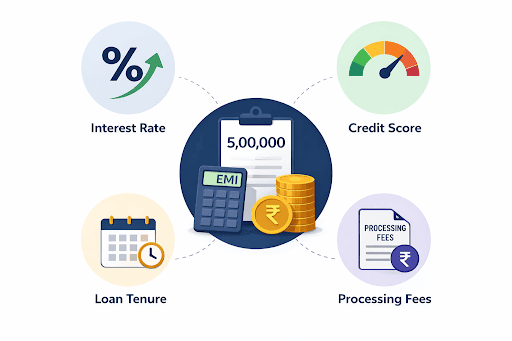

Your EMI depends on more than just the loan amount. A few key factors shape how much you end up paying.

1. Interest rate

Even a small increase here can push your EMI higher. It also increases the total repayment significantly. You should always check current personal loan interest rates before applying.

2. Credit score

Lenders look at your credit score before deciding on your interest rate. A stronger score usually means better terms.

3. Loan tenure

Extending your tenure lowers your EMI, but you pay more interest overall. A shorter tenure works the other way around.

4. Processing fees

These do not affect your EMI directly, but they increase the total cost of your loan.

Comparison of 5 Lakh Personal Loan EMI Across Top Lenders

Not all lenders offer the same rates, and that difference shows up in your EMI.

| Lender | Interest Range | EMI (3 Years) |

| Hero FinCorp | Around 18% | ₹18,072 |

| Kotak | 11% to 16% | ₹16,500 to ₹17,800 |

| SMFG | 12% to 18% | ₹17,000 to ₹18,500 |

| Airtel Finance | 12% to 24% | ₹17,500 to ₹20,000 |

Even a small rate difference changes your monthly outflow. That is why comparing lenders before applying always helps.

Eligibility Criteria for a ₹5 Lakh Personal Loan

You should always check whether you meet the basic requirements for a personal loan before applying.

Salaried applicants: You need a stable income, usually starting around ₹15,000 per month, along with a consistent employment history.

Self-employed applicants: You should show consistent income and business stability through financial records.

Documents required: Identity proof, address proof, and income proof are required for verification.

An eligibility calculator can give you a quick answer before you start the application.

Benefits of Choosing Hero FinCorp for 5 Lakh Personal Loan

Choosing the best lender makes your overall loan process smooth and easy. Let's see the benefits of applying for a personal loan from Hero Fincorp.

- Fully digital application process

- Fast approval and quick disbursal

- Flexible repayment options

- Clear and transparent terms

How to Apply Online for a 5 Lakh Personal Loan?

The process of applying for a personal loan online through Hero Fincorp is very simple. You have to follow these simple steps:

Step 1: Visit the Hero Fincorp website and click on products

Step 2: Click on "Apply Now"

Step 2: Enter your details and check eligibility

Step 3: Upload required documents

Step 4: Choose your loan amount and tenure

Step 5: Submit your application and wait for approval

After approval, the amount gets credited directly to your bank account.

Plan Your EMI Like You Plan Your Monthly Budget

A loan feels manageable when the EMI fits into your monthly routine without affecting your usual expenses. You already have a sense of where your money goes each month, so adding one more commitment should feel structured and thought through.

Hero FinCorp simplifies this entire process through its personal loan app. This app lets you track your EMI, and stay updated on your loan without going back and forth. Download the personal app on Android and iOS.

Frequently Asked Questions

What is the EMI for a 5 lakh personal loan for 3 years?

According to interest rate of 18%, the EMI comes to around ₹18,072 for 3 years. However, the exact amount depends on your profile and the lender.

Can I get a 5 lakh loan without collateral?

Yes. You can get a personal loan without providing any assets, as these loans are unsecured.

How does my credit score affect my 5 lakh loan EMI?

Your credit score influences the interest rate you receive from the lender. A higher score can reduce your EMI by allowing you to get a lower rate.

Are there any hidden charges on a 5 lakh personal loan?

No. The lenders disclose all the charges clearly, but you should always review the loan terms carefully.

Can I prepay my 5 lakh personal loan?

Yes, many lenders allow prepayment, though some may charge a small fee.

How long does it take for 5 lakh loan disbursal?

Disbursement of a 5 lakh loan takes a few hours to a couple of days with digital lenders.

What is the minimum salary required for a 5 lakh personal loan?

Most lenders require a minimum monthly income of around ₹15,000 along with stable employment.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.