How a 725+ CIBIL Score Helps You Secure a 4 Lakh Personal Loan

A ₹4 lakh personal loan is often taken for needs that require quick funding, such as medical expenses, home repairs, or consolidating existing debt. Although approval is vital, the difference is in the amount of interest that you will pay.

This is where your credit profile, in particular your CIBIL score, comes in. Having a good score, especially 725 or higher, may help obtain a lower interest rate, faster approvals, and more relaxed repayment terms.

Importance Of A 725 CIBIL Score For A 4 Lakh Personal Loan

A 725 CIBIL score is widely seen as the point at which a borrower moves from “average” to the “low-risk” or “prime” category. To the lenders, this score indicates steady repayment and financial discipline.

This is important because lenders charge interest rates based on risk. The higher the score of a borrower above 725, the lower the chances of default, and therefore, they are more appealing.

For example:

- Score 780 → Likely to get better rates and faster approvals

- Score 680 → May face higher interest or stricter checks

This is not just a difference in approval; it has a direct impact on the loan's long-term affordability.

Estimated Interest Rates For A 4 Lakh Loan With A 725 Credit Score

The interest rate on a personal loan with a 725 CIBIL is usually more competitive than for lower scores.

| CIBIL Score Range | Estimated Interest Rate | Monthly EMI (3 years) |

| 725+ | 10.5% – 18% | ₹13,000 – ₹14,500 |

| 650–749 | 13% – 18% | ₹13,500 – ₹14,500 |

| Below 650 | 18% – 24% | ₹14,500+ |

For instance, at 11%, a ₹4 lakh loan for 3 years may have an EMI of around ₹13,100, while at 18%, it may be ₹14,400. In the long run, this would add ₹40,000–₹60,000 to the total repayment.

EMI Breakdown: 4 Lakh Personal Loan For 725 CIBIL Score

Here’s how EMIs vary based on tenure:

| Tenure | Interest Rate | Approx EMI | Total Interest |

| 1 year | 18% | ₹36,672 | ₹40,064 |

| 2 years | 18% | ₹19,970 | ₹79,280 |

A shorter tenure has a larger EMI and less total interest, whereas a longer tenure has a lower monthly load but a higher total cost.

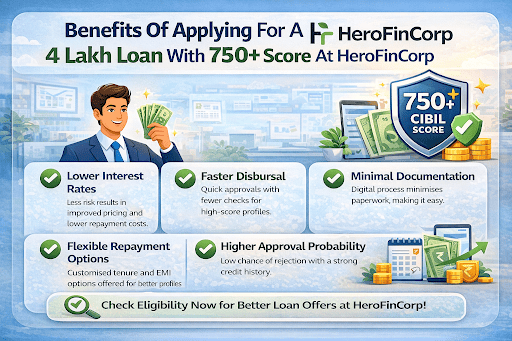

Benefits Of Applying For A 4 Lakh Loan With 725+ Score At Herofincorp

A good credit profile opens several benefits in taking a loan.

- Lower interest rates

Less risk will result in improved pricing and subsequent repayment.

- Faster disbursal

Profiles with high scores are usually eligible for faster approvals with fewer checks.

- Minimal documentation

The use of digital processes minimises paperwork and eases the application process.

- Flexible repayment options

Better profiles may get customised tenure or EMI options.

- Higher approval probability

There is a lower chance of application rejection for those with a good credit history.

Prior to applying, it is possible to check the eligibility to have an idea of the likely terms. You can explore this through Hero FinCorp’s official journey here.

Eligibility Criteria For ₹4 Lakh Personal Loan For 725 CIBIL Score

In order to be eligible, most basic eligibility requirements usually involve:

- Age between 21 and 60 years

- Minimum monthly income of ₹15,000–₹25,000 (varies by city)

- Stable employment (salaried or self-employed)

- Active bank account with transaction history

- Good repayment track record

Even with a 725 score, income stability remains important for approval.

Documents Required For A Seamless Digital Application

A digital loan application usually requires:

KYC Documents

- Aadhaar Card

- PAN Card

Income Proof

- Salary slips (past three months)

- Bank statements (past 6 months)

- ITR (self-employed people)

Verification and approval are facilitated through clear documentation.

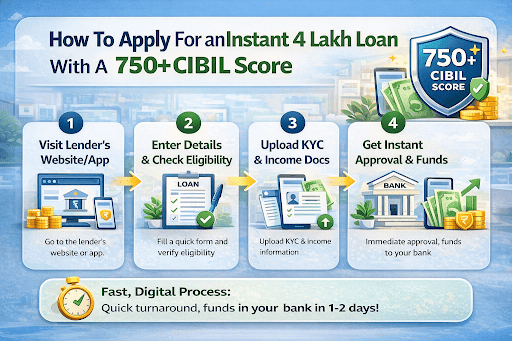

How To Apply For An Instant 4 Lakh Loan With A 725 CIBIL Score

The process is simple and largely digital:

- Go to the lender's website or app.

- Fill in simple information and verify eligibility.

- Post KYC and income information.

- Get an immediate approval (with verification)

- The money is deposited into your bank account.

This process can take 1-2 days, depending on the profile's eligibility.

Factors Beyond CIBIL That Influence Your 4 Lakh Loan Approval

A 725 score is good, but other factors are also involved.

- Debt-to-Income Ratio (DTI)

If more than 40–50% of income goes towards EMIs, approval may be affected. - Income consistency

Irregular income can reduce confidence in repayment capacity. - Employer profile

Working with reputed organisations may improve approval chances. - Recent credit inquiries

Too many loan applications in a short time may signal financial stress.

These factors are evaluated alongside the credit score to determine final loan terms.

Also Read: What Is a Term Loan? Meaning, Types, Features

Why Your 725+ Score Matters

Having a CIBIL score of 725+ would make a significant difference when seeking a ₹4 lakh personal loan. It not only increases the chances of approval but also helps reduce the interest rate, thereby lowering the overall cost of borrowing.

The slightest variation in interest rates can compound over time, making it imperative to maintain a good credit profile. Credit discipline and financial stability provide the right balance to access a better loan, and repayment is carried out comfortably.

Frequently Asked Questions

Is 725 a good CIBIL score for a ₹4 lakh loan?

Yes, it is considered powerful and can help secure better interest rates.

What is the minimum salary required?

Normally, ₹15,000-25,000 is based on the lender and location.

What EMI will I pay at 18% for 3 years?

Approximately ₹14,400 per month.

Can self-employed individuals apply?

Yes, with legitimate financial records and income records.

Does applying for a loan reduce CIBIL score?

A single inquiry is not a major difference, but multiple inquiries can decrease the score.

How quickly can the loan be disbursed?

To deserving candidates, several hours to 1-2 working days.

Is collateral required?

Personal loans are not typically secured.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.