What Is a Term Loan? Meaning, Types, Features, and How It Works in India

- Term Loan Meaning

- How Does a Term Loan Work?

- Types of Term Loans

- Key Features and Benefits of Term Loans

- Term Loan Eligibility Criteria

- Documents Required for a Term Loan

- Term Loan Interest Rates

- Term Loan vs. Working Capital Loan vs. Overdraft

- Advantages and Limitations

- How to Apply for a Term Loan with Hero FinCorp

- Frequently Asked Questions

Imagine you run a manufacturing unit in Pune. Orders are surging, and you need a new production line worth Rs 80 lakh. Your working capital covers daily operations, but a purchase this large needs a different kind of funding altogether. This is where a term loan steps in — providing structured, lump-sum capital that lets you execute growth plans without draining operational cash flow.

Below, we cover the meaning of a term loan, how it works, types of term loans, eligibility criteria, interest rates, and the application process — everything you need to make an informed borrowing decision.

Term Loan Meaning

A term loan is a fixed-amount credit facility from a bank or regulated NBFC, repaid over a set tenure through Equated Monthly Instalments (EMIs) that include both principal and interest.

Unlike a revolving credit line or overdraft where you draw and repay repeatedly, a term loan gives you the entire sanctioned amount upfront. Repayment tenures typically range from 12 months to 25 years depending on the loan type and purpose.

Under current RBI norms, lenders must provide a Key Fact Statement (KFS) and disclose the Annual Percentage Rate (APR) before disbursement, ensuring full transparency on costs.

Also Read: NBFC Personal Loan: Benefits, Online Process and Comparison with Banks

How Does a Term Loan Work?

Here is the typical lifecycle once you decide to pursue a term loan:

- Application & Documentation: Submit your loan application with KYC, financial statements, and business documents. Most lenders now accept digital applications with e-KYC.

- Credit Assessment: The lender evaluates your CIBIL score, business vintage, DSCR, revenue trends, and existing debt. For secured loans, collateral is also appraised.

- Sanction & Disbursement: On approval, you receive a sanction letter with all terms. The full amount is disbursed as a lump sum into your business account.

- EMI Repayment: Repayment follows an amortisation schedule — early EMIs are interest-heavy, and the principal component grows over time.

- Closure or Foreclosure: The loan closes on final EMI payment. Early repayment (foreclosure) is possible, though fees of around 5% + GST may apply within the lock-in period.

Also Read: What is Loan Amortization and How It Works?

Types of Term Loans

The types of term loans are classified by repayment duration and collateral requirement:

By Duration

- Short-Term (up to 18 months): For bridging cash flow gaps, seasonal inventory, or urgent expenses. Higher monthly EMIs but lower total interest cost.

- Medium-Term (1–5 years): The most common structure for SMEs. Used for equipment purchase, moderate expansion, and technology investments.

- Long-Term (5–25 years): For commercial real estate, large infrastructure projects, and business acquisitions. Lower interest rates but stricter eligibility.

By Security

- Secured: Backed by collateral (property, machinery, fixed deposits). Offers lower rates, higher amounts (up to 75% of asset value), and longer tenures.

- Unsecured: No collateral needed. Approval depends on creditworthiness. Faster processing but higher rates. A CIBIL score of 700+ is critical.

| Type | Tenure | Typical Use | Collateral |

| Short-Term | Up to 18 months | Cash flow gaps, inventory | Usually not required |

| Medium-Term | 1–5 years | Machinery, expansion | Depends on lender |

| Long-Term | 5–25 years | Real estate, large projects | Typically required |

| Secured | Varies | High-value investments | Mandatory |

| Unsecured | Varies | Growth without pledging assets | Not required |

What assets can a term loan finance? Industrial machinery, commercial real estate, business vehicles, technology infrastructure, plant upgrades, and business acquisitions or franchise purchases. The asset should have a productive life that justifies the loan tenure.

Also Read: Difference Between Term Loan and Working Capital Loan

Key Features and Benefits of Term Loans

- Lump-sum disbursement: Receive the entire sanctioned amount upfront for immediate large-scale purchases.

- Fixed repayment schedule: Known EMI amount, instalment count, and closure date from day one — enabling precise cash flow planning.

- Competitive interest rates: Lower than credit cards and overdrafts. Secured loans carry the lowest rates.

- Flexible tenure: Choose a repayment period matching your project’s payback cycle.

- Credit profile enhancement: Timely repayment strengthens your CIBIL score. Credit bureaus now update every 15 days under current regulations.

- Tax-deductible interest: Interest paid is generally deductible as a business expense under the Income Tax Act.

- No ownership dilution: Unlike equity financing, term loans do not reduce your stake in the business.

Term Loan Eligibility Criteria

While requirements vary by lender, here are the standard benchmarks:

| Parameter | Requirement |

| Applicant Age | 21 to 65 years |

| Business Vintage | Minimum 2–3 years of operation |

| CIBIL Score | 700–750+ for competitive rates; 650+ minimum |

| Annual Turnover | Varies; many lenders require Rs 50 lakh minimum |

| DSCR | 1.25:1 or higher (per RBI guidelines) |

| Financial Health | Consistent revenue, manageable debt, positive cash flow |

| Collateral (Secured) | Property, equipment, or fixed deposits of adequate value |

Documents Required for a Term Loan

Identity & KYC

- PAN card (applicant and business entity)

- Aadhaar card

- Business registration certificate (Partnership deed / CoI / MSME-Udyam registration)

- GST registration certificate

Financial Records

- Audited financial statements for the last 2–3 years

- Income Tax Returns (ITR) for the corresponding period

- Projected financials for the loan tenure (project-based loans)

Banking & Collateral

- Bank statements for the previous 12 months

- Existing loan account details and repayment history

- Property title deeds, valuation reports, or equipment invoices (secured loans)

Also Read: What is Debt Financing? A Complete Guide

Term Loan Interest Rates

Your rate is determined by:

- CIBIL score: 750+ qualifies for the lowest rates.

- Loan tenure: Longer tenure = slightly higher rate due to lender risk.

- Secured vs. unsecured: Collateral-backed loans carry lower rates.

- Business profile: Revenue stability, industry, and operating history.

- Benchmark: Floating-rate loans track the RBI repo rate and adjust periodically.

Hero FinCorp offers term loan interest rates starting from 18% p.a. The actual rate depends on your risk profile and product selection.

Term Loan vs. Working Capital Loan vs. Overdraft

| Feature | Term Loan | Working Capital Loan | Overdraft |

| Purpose | Capital expenditure, asset acquisition | Operational expenses | Short-term cash flow |

| Disbursement | Lump sum | Lump sum or tranches | Draw as needed |

| Tenure | 1–25 years | 6–36 months | Renewable annually |

| Repayment | Fixed EMIs | Flexible / EMI-based | Interest on utilised amount |

| Collateral | Optional | Varies | Linked to current a/c |

Use a term loan for large, one-time capital needs. Choose working capital loans for operations, and overdrafts for day-to-day liquidity.

Advantages and Limitations

Advantages

- Structured growth capital without depleting operating funds.

- Predictable EMIs for precise financial planning.

- Builds business credit — consistent repayment unlocks better future terms.

- Tax-deductible interest reduces effective borrowing cost.

- No ownership dilution unlike equity financing.

Limitations

- Fixed commitment: EMIs continue regardless of revenue fluctuations.

- Cumulative interest: Long tenures significantly increase total cost.

- Collateral risk: Secured loan default could mean losing pledged assets.

- Strict qualification: New businesses with limited history may not qualify.

- Foreclosure fees: Typically 5% + GST within the lock-in period.

How to Apply for a Term Loan with Hero FinCorp

- Visit herofincorp.com or download the app. Navigate to the term loan section.

- Check eligibility using the online assessment tool.

- Submit application with business details and loan requirement.

- Upload documents digitally (KYC, financials, business records).

- Receive approval after the credit team completes evaluation.

- Get disbursement — the loan amount is credited to your business account.

Frequently Asked Questions

What is a term loan in simple words?

A fixed amount borrowed from a lending institution, repaid through monthly EMIs over a set period. Used for large, one-time business expenses like machinery, expansion, or property.

What is a term loan facility?

The formal contractual arrangement between borrower and lender that defines the loan amount, interest rate, repayment schedule, and tenure.

Can a startup apply for a term loan?

Most lenders require 2–3 years of business vintage. Startups may explore the CGTMSE scheme, which offers collateral-free loans up to Rs 10 crore under the latest budget provisions.

Is collateral mandatory?

Only for secured term loans. Unsecured options are available for borrowers with strong credit profiles, though at higher interest rates.

Are there prepayment penalties?

Many lenders charge a foreclosure fee (around 5% + GST) for early repayment within the lock-in period. Review your specific loan agreement before prepaying.

How long does approval take?

It depends on documentation completeness and credit evaluation complexity. NBFCs like Hero FinCorp with digital processes typically offer faster turnaround than traditional institutions.

What is the ideal CIBIL score?

700–750+ for competitive rates. Some lenders consider 650+, but terms may be less favourable.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Taking a personal loan is the easy part. Managing the EMIs, month after month, is where the real work begins.

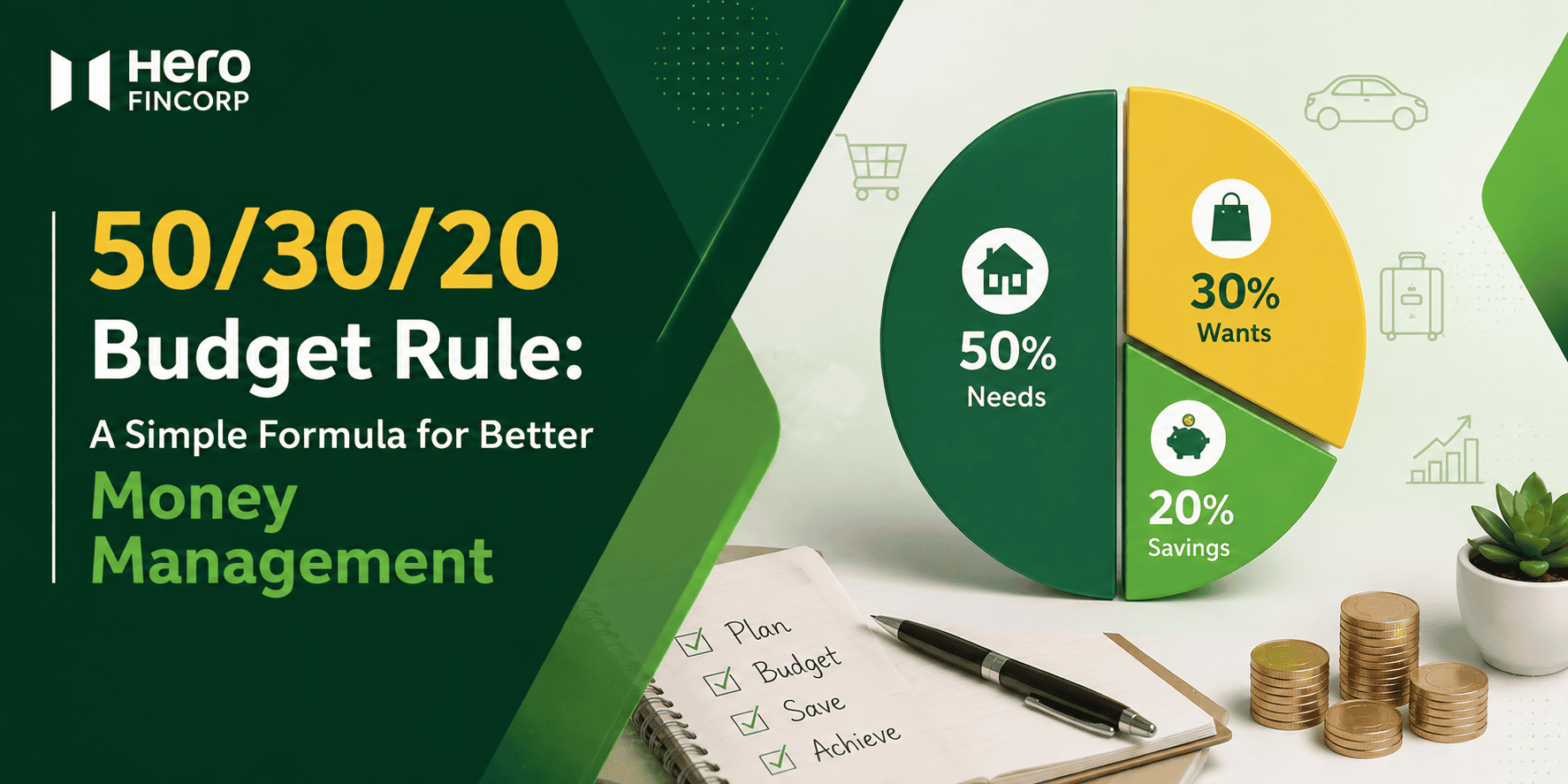

You look at your bank balance in the middle of the month. You think about where your salary went. This happens to a lot of people. The 50/30/20 budget rule is a way to stop feeling bad about how you spend your salary.

Every month, a slice of your salary vanishes into something called “PF”. It’s easy to treat it as just another deduction, but that deduction is quietly building your retirement corpus, tax-free. Understanding PF in salary, such as what it means, how it’s calculated, and when you can withdraw it, helps put you in charge of your long-term financial health. Let’s decode it without the jargon.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.