What is Credit Purchase? Meaning, Definition & Features

Running a business requires you to continue buying goods or services even when cash is short. It is not always practical to pay for everything upfront when funds are tied up in other operations or customer payments.

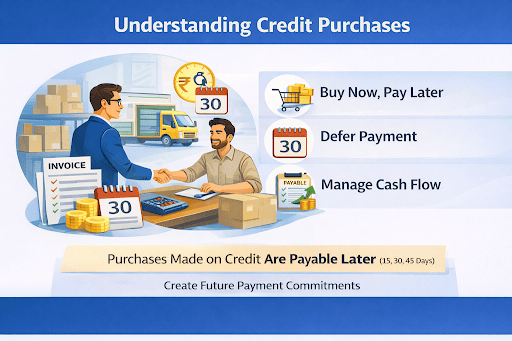

A credit purchase allows you to buy what your business needs now and pay for it later. While this helps manage short-term cash flow, it also creates future payment commitments that you need to plan for.

Understanding what a credit purchase is, how it works, and how it affects your accounts helps you use this option without creating cash flow pressure or accounting issues later.

Introduction To Credit Purchase: Meaning and Definition

When you make a credit purchase, your supplier allows you to take delivery of goods or services and pay after a fixed period. This gives your business breathing room to sell inventory or complete work before cash goes out.

So, what is a credit purchase in simple terms? It means you buy goods or services today and commit to paying your supplier within a specified number of days. You receive the goods immediately, but the cash outflow happens later. This works well when your sales cycle is longer than your purchase cycle.

Credit purchase allows you to buy goods or services without paying in cash immediately. In accounting terms, a credit purchase refers to a transaction where you receive goods or services now, but record the amount as a liability until you pay it.

Also Read: Credit Builder Loan:

Key Features Of Credit Purchase

| Feature | What it Means for You |

|---|---|

| Deferred payment | You take delivery now and pay later |

| Agreed credit period | You commit to pay within 15, 30, or 45 days |

| Working capital support | You preserve cash for operations |

| Creates liability | You record the amount as accounts payable |

| Time-bound obligation | You must pay on time to avoid penalties |

Advantages Of Credit Purchase

- Cash flow flexibility: You can buy stock or services without an immediate cash outflow.

- Operational continuity: You can continue purchasing when cash is temporarily tight.

- Better supplier terms over time: Making payments on time allows you to negotiate better credit periods.

- Scalable operations: You can align purchases with sales cycles rather than block capital upfront.

Disadvantages And Risks of Credit Purchase

- Payment pressure: It can be difficult to pay suppliers when customer payments are delayed.

- Late fees and penalties: Your costs can increase if you miss the due dates.

- Over-dependence on credit: Relying too much on credit purchases can make it difficult to handle cash.

- Supplier strain: Repeated delays can hurt relationships and affect future credit terms.

Accounting Treatment of Credit Purchase

When you record a credit purchase, you recognise both the expense or inventory and the payable.

At the time of purchase

| Account | Debit | Credit |

|---|---|---|

| Purchases / Inventory | Amount | — |

| Accounts Payable | — | Amount |

At the time of payment

| Account | Debit | Credit |

|---|---|---|

| Accounts Payable | Amount | — |

| Cash / Bank | — | Amount |

This method ensures your purchases and liabilities are accurately reflected until payment is made.

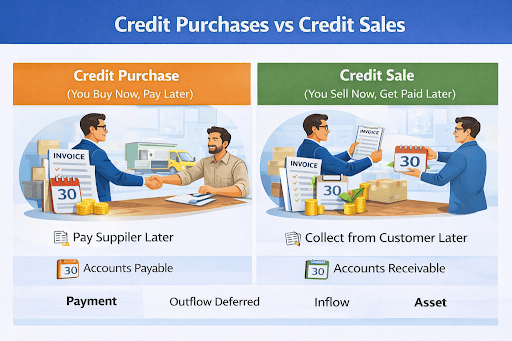

Credit Purchase vs Credit Sales

| Aspect | Credit Purchase (You Buy Now, Pay Later) | Credit Sales (You Sell Now, Get Paid Later) |

|---|---|---|

| Cash flow impact | Your cash goes out later | Your cash comes in later |

| Accounting entry | Accounts payable | Accounts receivable |

| Risk | Payment obligation | Collection risk |

| Management focus | Pay suppliers on time | Collect from customers on time |

Examples of Credit Purchase in Business

You can buy inventory worth ₹1,00,000 on 30-day credit, so you will receive the goods today and pay your supplier next month. This helps you sell the stock before cash goes out.

However, you will need to arrange payment to your supplier if the customer's payment is delayed by more than 30 days. So, align credit purchases with expected inflows.

Also Read: What is CGST & SGST? Key Differences Between Them

How to Manage Credit Purchases Effectively

- Track due dates for every supplier so payments are not missed.

- Match purchase cycles with expected customer collections.

- Avoid making large credit purchases in the same period.

- Maintain a simple schedule to track upcoming dues.

- Check credit terms regularly and negotiate if there are changes in cash cycles.

Why Choose Herofincorp for Credit Purchase Guidance

Managing credit purchases often creates short-term funding gaps. Hero FinCorp provides insights and financing options to help you manage working capital needs.

- You get clarity on aligning purchases with cash flow cycles.

- You can assess short-term funding needs more accurately.

- You receive support in planning business financing without disrupting operations.

You can explore suitable financing options for business needs through Hero FinCorp’s official journey here.

Also Read: What Is A Business Plan And Why Do You Need One?

Run Your Operations Smoothly

Credit purchases help you run operations smoothly when cash inflows and outflows are misaligned. Used well, it supports working capital and business continuity.

However, every credit purchase creates a future payment commitment that you must manage carefully. Understanding what credit purchase and planning payments on time helps avoid penalties, strained supplier relationships, and cash flow stress.

Frequently Asked Questions

What is the standard credit period given for credit purchases?

15, 30, or 45 days are common credit periods, or they may be based on supplier terms.

Can a credit purchase be cancelled or returned?

Returns or cancellations depend on supplier policies and agreed terms.

How does a credit purchase affect GST and tax filings?

GST liability arises based on invoice terms, even if payment is made later.

What happens if payment is delayed beyond the credit period?

Late fees may apply, and supplier relationships may be affected.

Is interest charged on delayed payments in a credit purchase?

Some suppliers charge interest or penalties for delays, as per contract terms.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.