CERSAI: Full Form, Meaning, Login, Charges, Registration & Fees

Taking a secured loan is not just about signing documents and setting up EMIs. Behind the scenes, there is a formal process that ensures the asset you pledge is properly recorded and protected.

That is where CERSAI comes in. It acts as a central record of security interests created by lenders across India. While most borrowers rarely interact with it directly, its presence strengthens trust in the lending system.

Let’s look at what CERSAI is, why it exists, and what those associated charges really mean.

What is CERSAI?

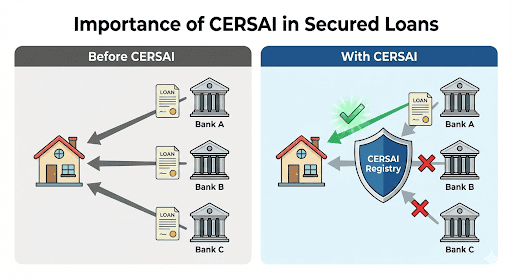

CERSAI is a central registry that keeps track of security interests created when loans disbursing loans on property, vehicles, or other movable assets. In other words, it's a database that prevents borrowers from using the same asset as collateral with more than one lender. The goal is to reduce the degree of fraudulent practices.

Before this system was in place, someone could borrow money from several banks using the same property as collateral. CERSAI lowers that risk by making loan charges visible to lenders through a centralised registry.

In short, CERSAI strengthens transparency in secured lending.

Full Form of CERSAI

The CERSAI full form is Central Registry of Securitisation Asset Reconstruction and Security Interest of India.

Its purpose is to maintain a central record of security interests created by banks and financial institutions to ensure transparency when loans are processed.

Who Owns CERSAI?

CERSAI is a government company established under the SARFAESI Act, 2002. It operates under the supervision of the Government of India (GoI), with shareholding from public sector banks and housing finance institutions. The framework ensures that it functions as a regulated and structured registry for secured transactions across the country.

What is the CERSAI Search?

A CERSAI search allows lenders to check whether an asset like a property or vehicle has already been used as collateral for a loan. In other words, they get to verify whether the asset has already been mortgaged or charged, besides avoiding disputes over their ownership.

Before approving a secured loan, lenders typically conduct this search through the CERSAI portal. This reduces the risk of duplicate financing and helps verify ownership claims. Think of it as a background check on the asset being bledged.

Also Read: Secured Loans Vs. Unsecured Loans: A Comparison

CERSAI Registration Process

When a bank or financial institution sanctions a secured loan, it must register the charge with CERSAI.

Here’s how the CERSAI registration process works:

- The lender logs into the official CERSAI portal

- Loan and borrower details are entered

- Details of the secured asset are uploaded

- Applicable CERSAI registration fees are paid

- A unique registration number is generated

This registration must usually be completed within a specified time from the date of creating the security interest.

Borrowers themselves do not directly register loans; it's the lenders that typically handle this process.

CERSAI Login: How to Access the Portal

The CERSAI login facility is primarily meant for banks, financial institutions, and authorised users.

To access the portal:

- Visit the official CERSAI website

- Create an account or log in using your registered user ID and password

- Once you're logged in, you can access all the services the portal offers

Borrowers typically cannot create direct login accounts. However, they may request confirmation from their lender regarding registration details.

CERSAI Charges and Fees

One common question most people ask is "What are CERSAI charges?"

CERSAI registration fees vary depending on:

- The type of asset (movable or immovable)

- The loan amount

- Whether it is a fresh registration or modification

As per the current fee structure on the CERSAI website, the charges levied to run a search on the portal are ₹10. The cost for the creation or modification of a security interest is ₹50. You can find all other charges listed on the website.

Importance of CERSAI in Secured Loans

CERSAI plays a major role in India’s secured lending system.

It helps:

- Prevent multiple loans against the same asset

- Increase transparency in lending

- Reduce the risk of fraudulent activities like multiple financing and benami transactions

- Strengthen lender confidence

- Ensure greater efficiency in loan processing

Without a central registry, lenders would rely heavily on manual verification. CERSAI simplifies and standardises this process across institutions.

How CERSAI Protects Lenders and Borrowers

CERSAI protection works at two levels.

For lenders, it reduces the risk of fraudulent or duplicate collateral. This lowers potential losses.

For borrowers, it creates a documented record of the loan charge. Once a loan is fully repaid, the lender must update or close the charge in the registry. This helps avoid future disputes regarding ownership or outstanding liabilities.

In that sense, CERSAI improves accountability on both ends of the spectrum.

Do you need to apply for a loan? Check your eligibility in minutes with Hero FinCorp's instant personal loan tool.

Frequently Asked Questions

What is CERSAI and why is it needed?

CERSAI is a central registry that records security interests created on assets for secured loans. It prevents lending against a property or asset that's already been charged or mortgaged.

How to register a loan in CERSAI?

The lender registers the loan through the official CERSAI portal by submitting borrower and asset details and paying the required fee.

What are the CERSAI fees?

Fees depend on the loan amount and type of asset. They are usually paid by the lender and may be included in processing costs charged to the borrower.

Can multiple lenders register the same asset?

Once a charge is registered, it becomes visible in the system. A second lender would see the existing registration during a search, which helps prevent duplicate financing.

How to check CERSAI registration status?

Lenders can check their registration status through the through the CERSAI portal. Additionally, borrowers can also request confirmation from their financial institution.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.