Explaining the Prompt Corrective Action Framework (PCA) by RBI

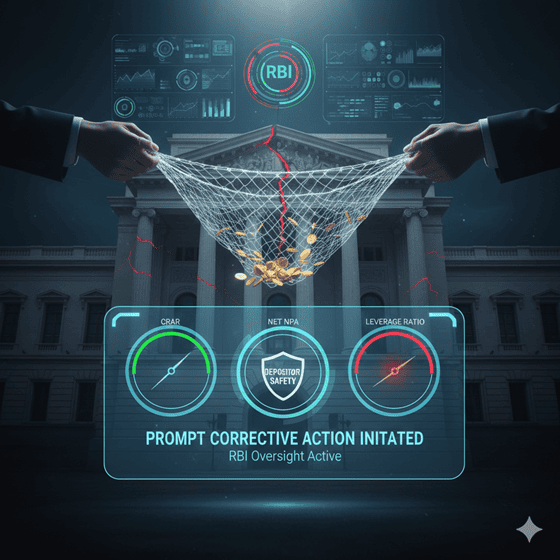

In the financial world, health is everything. Just as a doctor monitors vitals to prevent illness, the Reserve Bank of India (RBI) uses Prompt Corrective Action (PCA) to monitor banks. So, what is prompt corrective action? It is a supervisory framework that allows the RBI to intervene when a bank’s financial health deteriorates. PCA in banking isn't about closing institutions; it’s about early detection. By catching red flags like falling capital or rising bad loans, the regulator ensures a bank doesn’t reach a point of no return.

Importance of PCA in Banking

Banks are the backbone of the economy; if one falters, it can shake public trust in the entire system. The importance of PCA in banking lies in its role as a safety net for depositors. When a bank is placed under this framework, it is forced to tighten its belt and fix internal issues. This proactive approach prevents small cracks from becoming total collapses, ensuring your money remains safe while the bank regains its footing.

RBI’s Prompt Corrective Action Framework: An Overview

The prompt corrective action framework is the RBI's rulebook for disciplined banking. While it primarily applies to commercial banks, the PCA framework rbi uses is transparent and based on specific numerical thresholds.

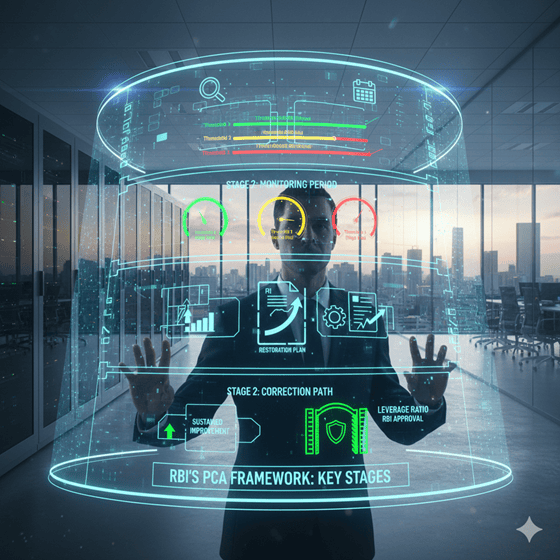

Key Components and Stages:

- Monitoring: The RBI tracks performance based on audited annual results.

- Risk Thresholds: There are three risk levels. As financials worsen, a bank raises thresholds and imposes stricter penalties.

- Correction Path: Banks under PCA must submit a "restoration plan" to fix their balance sheets.

- Exit Strategy: A bank exits only after showing sustained improvement and meeting strict RBI criteria.

Key Parameters That Trigger PCA by RBI

The PCA framework rbi monitors three specific "vitals." If these cross certain limits, the prompt corrective action framework kicks in:

- CRAR (Capital to Risk-Weighted Assets Ratio): Measures the capital cushion available to absorb losses.

- Net NPAs (Non-Performing Assets): The percentage of loans unlikely to be repaid. High NPAs signal poor lending health.

- Tier 1 Leverage Ratio: Compares core capital against total exposure to ensure the bank isn't over-extended.

Steps and Regulatory Actions Under the PCA Framework

Once triggered, the prompt corrective action framework allows the RBI to take several measures. PCA in banking involves two types of actions:

Mandatory Actions:

Dividend Restrictions: Banks cannot pay out profits to shareholders.

- Branch Expansion: Limits on opening new branches to save costs.

- Capital Infusion: Owners may be required to pump in more cash.

- Discretionary Actions:

- Lending Limits: The RBI may halt lending to high-risk sectors.

- Special Audits: Deeper inspections of the bank's books.

- Management Changes: In extreme cases, the RBI may suggest restructuring or leadership changes.

Impact of PCA on Banks and Customers

For a retail customer, very little changes day to day. You can still withdraw money and use ATM services. However, a bank under PCA in banking may become pickier about granting new loans and might stop offering high-risk products. For the bank, it is a period of "forced austerity"—cutting costs and focusing entirely on recovering bad loans to become healthier for the future.

Significance of PCA Framework in Ensuring Banking Sector Stability

The prompt corrective action framework is a guardian of financial stability. By intervening early, the RBI prevents "contagion"—where one bank's failure panics the whole market. In a growing economy, this discipline is non-negotiable. It replaces guesswork with data-driven regulation, building confidence among international investors and local depositors alike.

How Herofincorp Helps Understand and Navigate PCA

At Hero FinCorp, we help you stay ahead of complex regulations, such as the Prompt Corrective Action Framework. We support your financial journey by:

- Simplifying Finance: Breaking down RBI rules into clear insights.

- Strategic Planning: Helping businesses understand how a bank’s PCA status affects their credit options.

- Financial Health: Providing guidance to help you maintain a strong profile, mirroring the discipline the RBI expects from banks.

Frequently Asked Questions

What triggers Prompt Corrective Action in banks?

PCA is triggered by breaches in the capital-to-risk ratio (CRAR), Net NPAs, and Leverage Ratio thresholds.

How does PCA affect daily banking services?

Daily services like withdrawals and deposits remain unaffected. The main impact is on the bank’s ability to lend or expand.

Can a bank exit the PCA framework?

Yes, if it shows sustained improvement in its financials for at least one year and meets RBI standards.

How is PCA different from a merger?

PCA is a corrective phase to fix a bank. Mergers are "resolution" measures used when a bank cannot be fixed through PCA.

What role does PCA play in protecting depositors?

It acts as an early warning, forcing banks to fix issues before they risk losing depositor money.

How often does RBI review banks under PCA?

While based on annual results, the RBI monitors progress on a continuous, quarterly basis.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.