Learn How to Remove Settlement from CIBIL

Rajnish is a salaried professional in Pune. He applied for a personal loan to cover a medical emergency. All his documents were in place, displaying his steady income and stable job. Still, his application faced delays. When he checked his credit report, he noticed a ‘settled loan account’.

Such situations can lower one's creditworthiness and make lenders cautious. Many borrowers search for how to remove settlement from CIBIL. With the right steps, you can learn how to remove settled status from CIBIL and rebuild your credit profile.

Let us understand the CIBIL clearance process, how to remove loan account from CIBIL, and how to improve your score.

What is CIBIL Settlement?

A loan settlement is a process in which a borrower does not pay the full outstanding amount to close the loan. He pays a reduced amount. In this case, the credit report marks the account as ‘Settled’ instead of ‘Closed.’

Why this matters:

- It shows that the full loan amount was not repaid

- It may reduce your CIBIL score

- Future loan approvals may require additional checks

This is why you must understand how to remove settlement from CIBIL and restore your credit profile.

What is Settled Status in CIBIL?

Here is the difference between ‘Settled’ and ‘Closed’ status in CIBIL:

| Status | Meaning | Impact on Credit Score |

| Closed | Loan fully repaid as per the agreement | Positive impact |

| Settled | Loan partially repaid after negotiation | Negative impact |

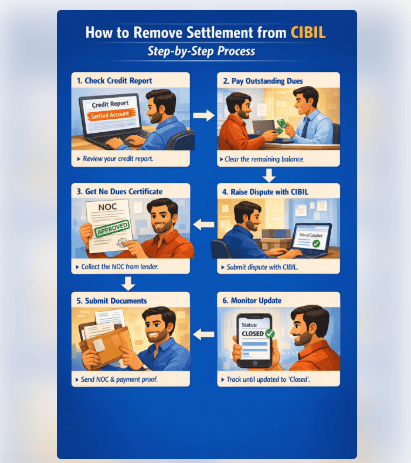

How to Remove Settlement from CIBIL - Step-by-Step Process

For CIBIL clearance, follow these steps:

Step 1 - Check the Latest Credit Report

Check your credit report and verify the settled account. Check:

- Loan amount

- Settlement remarks

- Lender name

Step 2 - Contact the Lender and Pay Outstanding Amount

Reach out to the lender and request the exact remaining balance that needs to be paid for closing the loan fully.

Step 3 - Clear Outstanding Dues

Pay the remaining amount and keep payment proof, such as receipts or bank statements.

This step is essential if you want to know how to remove settled status from CIBIL successfully.

Step 4 – Ask for a No Dues Certificate

After clearing the pending amount, request a No Objection Certificate or NOC from the lender. This certificate confirms that the loan is fully repaid, and there is no outstanding amount.

Step 5 - Submit a Dispute with CIBIL

Raise a dispute through the credit bureau portal and attach:

- Payment proof

- NOC from the lender

Step 6 - Monitor the Update

The correction process may take a few weeks. Track the status until the account reflects ‘Closed’ instead of ‘Settled.’

Also Read: Negotiating a Personal Loan Settlement: Everything You Need to Know

Can Settlement be Removed Without Paying Dues?

In most cases, removing a settlement without payment is not possible.

Credit bureaus only record information provided by lenders. If a loan was settled for a lower amount, the record remains unless the full outstanding dues are cleared and the lender reports the updated status.

Therefore, if you are searching for how to remove settled status from CIBIL, the most reliable method is:

- Repay the remaining balance

- Obtain NOC

- Request the lender to update the credit record

Also Read: What is NOC After Loan Closure?

How to Avoid Settling Loans in the Future

Loan settlement should be a last-resort option. You can reduce the chances of settlement by following these practices:

- Maintain an emergency fund for unexpected expenses

- Borrow within your repayment capacity

- Pay EMIs on time to avoid penalties

- Track your credit report regularly

- Avoid taking multiple loans at the same time

Also Read: Loan Settlement vs Loan Closure: Key Differences, Rules & Impact

How to Remove Loan Account from CIBIL

Follow these steps to remove an incorrect loan account from your credit report:

Step 1 - Check your credit report and verify the details of the incorrect account

Step 2 - Cross-check with the lender

Step 3 - Pay all pending dues

Step 4 - Obtain an NOC

Step 5 - Raise a dispute with the credit bureau, and ask for status correction

Step 6 - Monitor the update

How to Remove Settled Status from CIBIL

To summarise, if you are thinking how to remove settlement from CIBIL, then it involves four actions:

- Repay the remaining outstanding loan amount

- Obtain a No Dues Certificate from the lender

- Request the lender to update the account status

- Raise a dispute with CIBIL if the record is not updated

Following these steps can help move the account from ‘Settled’ to ‘Closed,’ improving your credit profile over time.

How to Improve CIBIL Score After Settlement Removal

Even after removing settlement remarks, you must follow these steps to improve your CIBIL score after settlement removal:

- Pay all your EMIs and bills on time

- Maintain low credit utilisation

- Avoid multiple loan applications

- Keep older credit accounts active

- Check your credit report for errors

Uniform repayment behaviour strengthens your credit profile and improves borrowing confidence.

If you require funds for planned or urgent needs, you can explore options like checking your eligibility for a personal loan through Hero FinCorp’s instant personal loan journey.

You can also manage applications conveniently using the Hero Digital Lending App – Android/ iOS.

Signing Off

While a loan settlement might feel like a quick escape from financial pressure, it often leaves a lasting footprint on your credit history. Opting for a "settled" status instead of a "closed" one is a signal to future lenders that the original agreement was not fully honoured.

This distinction can linger on your CIBIL report for years, acting as a red flag that suggests a higher risk profile, which often leads to higher interest rates or outright rejections when you apply for essential credit in the future.

Frequently Asked Questions

What is a ‘settled’ status in a CIBIL report, and how does it affect your credit score?

A settled status means the borrower paid a reduced amount to close the loan. It may lower the credit score because the full amount was not repaid.

Can a settled status be removed from the CIBIL report permanently?

Yes, but only after paying the remaining dues and requesting the lender to update the status to ‘Closed.’

Can I remove the CIBIL settlement without paying the outstanding amount?

No. You must confirm full repayment before updating the status.

How long does a settled loan status remain on a credit report?

It may remain for several years unless corrected after repayment.

What steps are required to change a ‘settled’ status to ‘closed’?

You must repay the remaining dues, obtain an NOC, and request that the lender and credit bureau update the record.

How long does it take to update the settlement removal after repayment?

Updates can take a few weeks after the lender verifies the change.

Will removing settled status immediately improve your credit score?

Your score may gradually improve as lenders check your repayment behaviour.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.