What Are Credit Bureaus And What Do They Do

- Credit Bureau Meaning and Definition

- How Do Credit Bureaus Work?

- Credit Bureaus In India

- Understanding Bureau Score (Credit Score)

- Credit Bureau Regulation And Consumer Rights

- How To Dispute Credit Report Errors With Credit Bureaus

- Benefits Of Credit Bureaus

- Why Choose Herofincorp For Credit Bureau Services?

- Conclusion

- Frequently Asked Questions (FAQs)

A loan application is assessed not only on an income basis but also on previous lending behaviour. Before loans are given or interest charged, lenders consider extensive credit history.

This data is provided by a credit agency that maintains records of borrowing and repayment behavior. To determine how lenders evaluate creditworthiness and decide whether to approve or deny a loan, it makes sense to understand credit bureaus.

Credit Bureau Meaning and Definition

A credit bureau is an organisation that gathers, stores, and processes credit-related data for both customers and businesses.

A credit bureau is an institution that maintains a record of borrowing behavior, such as loans, credit card use, and payment history.

How Do Credit Bureaus Work?

The information is collected by credit bureaus from banks, NBFCs, and other financial institutions. These include loan information and repayment history, credit card usage, and occasionally public records.

This data is then used to calculate a credit score that ranges from 300 to 900 in India. A high score indicates lower risk, and a low score indicates higher risk.

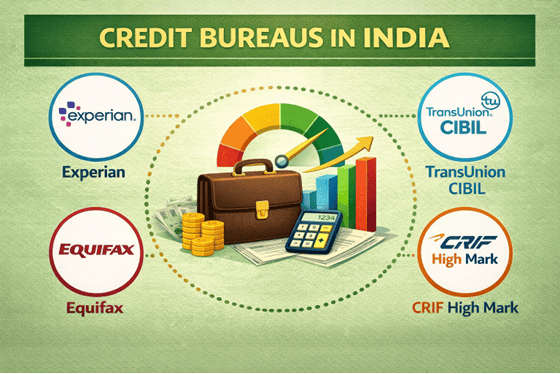

Credit Bureaus In India

RBI controls four large credit bureaus in India:

- TransUnion CIBIL (est. 2000)

The most popular bureau in India. CIBIL scores range from 300 to 900, and a score of 725 or above is generally considered strong.

- Experian India (est. 2010)

Offers credit reports and credit scores, which lenders extensively use to assess risk.

- Equifax India (est. 2010)

A world credit rating agency that provides extensive credit information and analytics.

- CRIF High Mark (est. 2007)

Typically, microfinance and rural lending data, and retail credit data.

Each bureau may show slightly different scores based on available data and calculation models.

Also Read: What is CRIF: Its importance & Difference between Cibil & CRIF Score

Understanding Bureau Score (Credit Score)

A bureau score, commonly known as a credit score, indicates creditworthiness based on financial behaviour.

In India, the scores are generally between 300 and 900 with:

- 725+ considered strong

- 650–749 moderate

- Below 650 indicates a higher risk

Several factors influence this score:

- Payment history (most important)

- Credit utilisation (how much credit is used)

- Length of credit history

- Number of active loans

- Recent credit enquiries

For example, paying EMIs on time for 12 months can improve the score, whereas consistently missing payments can significantly lower it.

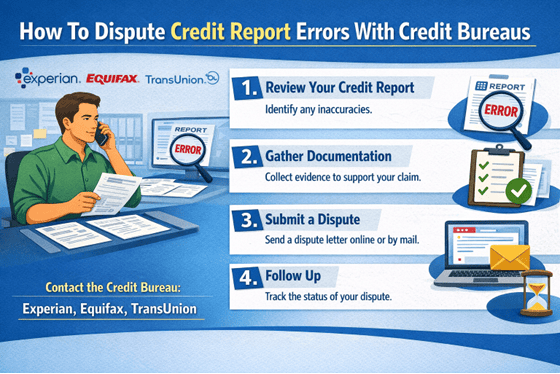

How To Dispute Credit Report Errors With Credit Bureaus

Mistakes in credit reports may affect loan approvals; it is important to rectify them.

Step 1: Access your credit report.

Obtain reports of credit agencies such as CIBIL or Experian.

Step 2: Identify errors

Detect incorrect loan entries, duplicate accounts, and default reports.

Step 3: Raise a dispute online

File a correction request at the website of the bureau.

Step 4: Verification process

To confirm the claim, the bureau contacts the lender.

Step 5: Resolution

Verification varies with updates; it is typically completed within 30 to 45 days.

Benefits Of Credit Bureaus

- Credit bureaus improve transparency by maintaining a central record of credit behaviour.

- They assist lenders in accurately evaluating risk before issuing loans.

- They lead to responsible borrowing by monitoring repayment discipline.

- They allow people to create a credit record over time.

Additional Resources And Tools

- Several tools help monitor and improve credit health:

- Credit score tracking platforms for regular monitoring

- Credit health reports to identify improvement areas

- EMI calculators to plan borrowing better

- Mobile apps that track credit usage and alerts

When exploring loan options, checking eligibility and credit standing can provide greater clarity. This can be done through Hero FinCorp’s official journey.

Why Choose Hero fincorp for Credit Bureau Services?

Hero FinCorp provides credit information that allows you to view your financial position before applying for a loan.

Loan options may be explored based on the credit profile to help align expectations with eligibility. Resources and tools make it easy to learn about credit scores, reports, and borrowing choices.

Also Read: Alternative Credit Scoring: Benefits, Features & CIBIL Alternatives

Conclusion

The credit bureaus are central to borrowing decisions. Awareness of what a credit bureau is, its uses, and its purpose would help explain credit scores, loan approvals, and interest rates, thus helping one secure better loans over time.

Frequently Asked Questions (FAQs)

1. What is a credit bureau, and how does this work in India?

A credit bureau acquires and evaluates credit information about lenders to produce credit reports and a credit score utilised when issuing loans.

2. What are the biggest credit bureaus in India?

High Mark, CRIF, Transunion CIBIL, and Experian.

3. What kind of information do credit bureaus get?

Credit card, credit card usage history, loan repayment history, and credit enquiry.

4. What determines the credit score by credit bureaus?

These scores are pegged to credit behaviour, the mix of loans, payment history, and credit usage.

5. Who is the regulator of credit bureaus in India?

According to the CICRA 2005, they are regulated by the RBI.

6. What are credit bureaus, and how are they relevant when obtaining a loan?

They facilitate lenders' risk assessment, loan eligibility determination, and interest rate determination.

7. Is it possible to check and fix credit reports?

Yes, individuals can file complaints about errors by submitting online reports.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

A credit score can seem like a number that has a lot of control over your money. When you learn about the CIBIL score range, you will see how it can help you get loan deals and have your loans approved faster.

You’ve checked your CIBIL score, then glanced at an Experian report, and the numbers don’t match. That confusion is common. Both are RBI-licensed credit bureaus that measure your creditworthiness, but they do it differently. Knowing the CIBIL and Experian difference puts you in control when a lender says they checked one over the other. Here’s exactly how they compare and why both matter.

A CIBIL score is a three-digit number ranging from 300 to 900 that summarises your credit history, repayment behaviour, outstanding debt, and credit mix. It is calculated by CIBIL (Credit Information Bureau India Limited), one of four RBI-approved credit bureaus in India alongside Experian, Equifax, and Highmark.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.