Difference Between Finance Lease and Operating Lease

Rajkumar has a growing logistics startup in Pune that needs delivery vans. He has two options: either buy the vehicles through a finance lease or use them temporarily through an operating lease. Both options allow him to use the assets without paying the full purchase price.

The difference between finance lease and operating lease mostly revolves around ownership, taxation, and financial planning.

The leasing definition in finance is a term whereby the lessor (owner) permits the lessee to utilise the asset for a period in return for a payment.

Let us understand what operating and finance lease structures are. This helps businesses manage cash flow while accessing expensive assets.

What is a Finance Lease?

A finance lease is a long-term lease contract. The lessee bears most of the risks and rewards and may purchase the asset at the end of the lease (not mandatory). The lessor is the legal owner of the asset.

The key features of a finance lease are:

- Long lease duration, covering most of the asset’s useful life

- Fixed periodic payments agreed at the beginning

- Possible ownership transfer at the end of the lease term

- Maintenance, insurance, and repairs - responsibility of the lessee

Example - A manufacturing company, ABCP Limited, enters a finance lease contract for the lease of heavy machinery for a lease term of 7 years.

Pros

- Access to expensive assets without a large upfront investment

- Possible ownership at the end of the lease

- Predictable long-term payments

Cons

- Less flexibility to cancel the agreement

- Responsible for maintenance/operational risks

What is Operating Lease?

To understand what is operating lease, this is an agreement wherein the ownership and risks lie with the lessor.

Businesses engage in an operating lease when they wish to use an asset without owning it.

Key characteristics are:

- Ownership remains with the lessor

- The asset is returned after the lease period

- Maintenance responsibilities often remain with the owner

For instance, NDT Ltd leases digital scanning equipment for 2 years. After the operating lease term, the equipment is returned, and a new one is leased for another 2 years.

Pros

- Greater flexibility

- Lower commitment compared to finance leases

- Easy upgrades when technology changes

Cons

- No ownership rights

- Payments continue as long as the asset is needed

Difference Between Finance Lease and Operating Lease

Here is the difference between operating and finance lease:

Accounting Treatment of Leases

Accounting rules for finance and operating leases are:

| Aspect | Finance Lease Accounting | Operating Lease Accounting |

| Balance Sheet Impact | The leased assets and liabilities are shown on the balance sheet. | Short-term leases of less than 12 months and low-value assets are treated as rental expenses in P&L. Most leases recognise RoU asset and lease liability just like in a finance lease. |

| Expense | Businesses show depreciation on the asset and interest on lease payments. | Depreciation on the Right-of-Use asset and interest expense are shown on the lease liability. Only exempt leases may be treated as rental expenses. |

| Payment Structure | Bifurcated into interest cost and principal repayment. | Allocated between principal repayment and interest unless the lease qualifies for exemption. |

| Influence | Assets and liabilities increase. | Expenses remain predictable. |

| Accounting Rules | The leased asset and liability are recognised during the lease term. | Most leases require a right-of-use asset recognition on the balance sheet, under new accounting standards. |

Tax Implications and Benefits

Tax treatment can also influence the choice between operating and finance lease options.

Finance Lease Tax Benefits

- Businesses may claim depreciation on the leased asset

- Interest components of lease payments may be tax-deductible

Operating Lease Tax Treatment

- Lease payments are often fully deductible as operating expenses

- No depreciation claims since ownership remains with the lessor

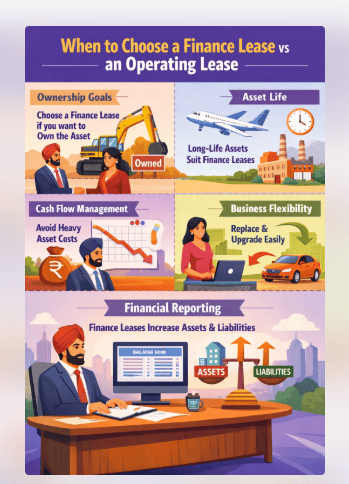

When to Choose a Finance Lease vs an Operating Lease

Choosing an operating or finance lease depends on realities like:

- Ownership goals - The business should consider a finance lease if it is interested in owning the asset.

- Asset life - Assets with a long life are more suitable for finance leases.

- Cash flow management - The business should avoid heavy asset costs.

- Business flexibility requirements - Assets should be replaceable or upgradeable, making operating leases more appropriate.

- Business financial reporting requirements - Finance leases increase assets and liabilities.

Also Read: Finance in Business: What is It? Types & Sources Explained

Examples of Finance and Operating Lease

Here are some of the real-world applications:

Finance Lease Examples

- Heavy manufacturing equipment and machinery

- Commercial vehicles/trucks

- Construction equipment

Operating Lease Examples

- Office buildings or coworking spaces

- Computers and printers

- Vehicle fleets

Signing Off

For businesses to use assets and manage cash flow effectively, it becomes important to understand the difference between finance lease and operating lease.

They are both leasing options wherein businesses or individuals can use high-value equipment without fully owning it.

If you are planning for a big purchase or managing business expenses, consider these alternatives.

You can also check your eligibility for business financing or an instant personal loan through Hero FinCorp’s digital journey here.

Prefer managing finances on your phone? Download the Hero Digital Lending App -Android/iOS.

Frequently Asked Questions

What is the difference between finance lease and operating lease?

For a finance lease, which is long-term, the risk and reward can be transferred to the lessee, while for an operating lease, which is short-term, ownership is not transferred.

What are the features of a finance lease?

Finance lease has a lengthy duration where risks are transferred to the lessee, and it includes fixed periodic payments.

What are the features of an operating lease?

An operating lease is where risks and ownership are not transferred to the lessee, and it offers more flexibility.

Who owns the asset in an operating and finance lease?

In a finance lease, the lessee can buy the asset later, but in an operating lease, the lessor retains full ownership.

What is the accounting treatment of an operating and finance lease?

Under both leases, businesses must show Right-to-Use assets and lease liability on the balance sheet (short-term and low-value assets are exempted). Lease payments can then be shown as depreciation or interest expenses.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.