How a 725+ CIBIL Score Helps You Secure a 3 Lakh Loan at Lower Interest

Individuals who want to pay medical expenses or urgent repairs often apply for a 3 lakh personal loan. The interest on the 3 lakh loan varies with the loan amount.

The interest rate varies depending on the credit profile. A 725+ CIBIL score helps to reduce the interest rate. It makes the loan more affordable and easier to manage.

Understanding The Interest Rates In 2026 On A 3 Lakh Personal Loan

The interest rate on a 3 lakh personal loan in India ranges from 10% to 24% per annum. It varies with factors such as the policies of the lender, credit score and income stability.

For example, at 11% interest, a 3 lakh loan for 3 years brings EMI of about ₹ 9800.

At an 18% rate, the EMI will increase to around ₹ 10,800. This difference may be small, but the total interest varies by ₹25,000 to ₹40,000 over the loan tenure.

The interest on a 3 lakh personal loan is calculated using the reducing-balance method. The interest is charged on the outstanding principal rather than the original amount. It makes both tenure and interest rate critical when determining the total repayment.

Why Is A CIBIL Score of 725+ Considered A Magic Number By Lenders?

A 725 CIBIL score is considered low risk by lenders. This score indicates consistent repayment behavior, financial stability, and controlled credit use to lenders.

Borrowers with a CIBIL score below this threshold may still qualify for a loan, but at a higher interest rate due to perceived risk.

For example:

- Score 780: Lower interest (10-13%), faster approval

- Score 700- Moderate rates (13-17%), more checks

This difference arises from the risk-based pricing strategy used by lenders. A higher score reduces uncertainty and offers better terms to the lenders.

Estimated Interest Savings: 725+ Score vs. Average Score

The table shows how a credit score affects the cost for a 3 lakh loan:

| CIBIL score | Interest Rate | EMI (3 YEARS) | Total Interest |

| 725+ | 18% | ₹ 10,856 | ₹ 90,446 |

| 700 | 15% | ₹ 10,400 | ₹ 74,400 |

| 650 | 20% | ₹ 11,100 | ₹ 99,600 |

Borrowers with a score of 725+ can save between ₹20,000 and ₹45,000 compared to those with lower scores.

This shows that a credit score affects affordability.

Factors Influencing Your 3 lakh Personal Loan Interest Rate

Apart from credit score, many other factors also influence interest rates, such as:

- Stability of Income: A steady income provides lenders with assurance.

- Debt-to-income Ratio Factor (DTI): Lenders will increase interest rates or reduce eligibility if more than 40-50% of income is spent on EMIs.

- Credit History Length: A longer track record of responsible borrowing improves credibility.

- Existing Liabilities: Multiple active loans show a higher financial burden.

What Is The Impact Of Employment Type On Your Loan Terms?

The type of employment plays a vital role in determining the loan terms. Salaried individuals with a fixed monthly income are considered lower risk. It can lead to a higher interest rate.

On the other hand, the self-employed may face greater scrutiny due to differences in income.

Also Read: 7 Essential Personal Loan Tips for Self-Employed Applicants

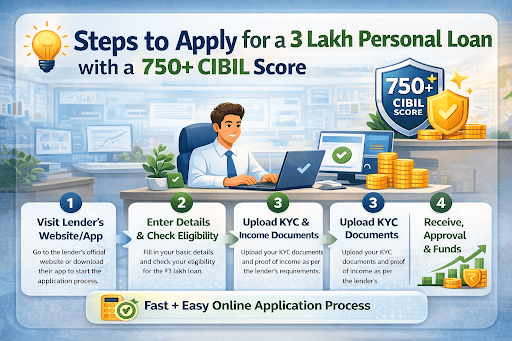

Steps To Apply For A 3 Lakh Personal Loan With A 725+ CIBIL Score

The application process is digital and simple:

- The first step is to go to the lender’s website or app

- You have to enter the basic details and check your eligibility

- Upload KYC and income documents

- You will receive approval after the verification process

- At last, the borrower will receive the funds in their bank account

Before applying, checking eligibility can help avoid unnecessary rejections and set clear expectations. You can explore suitable options through Hero FinCorp’s official journey here.

High-score borrowers will get approvals within a few hours to 1-2 working days.

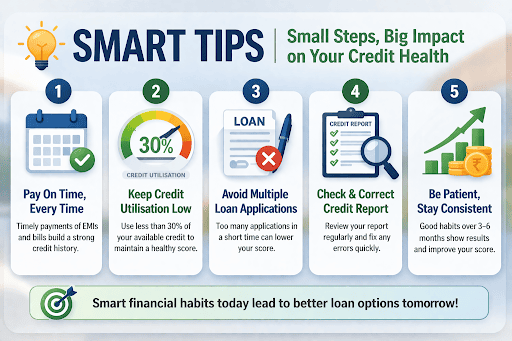

Smart Tips To Maintain Your 725+ Score After Getting The Loan

It is necessary to maintain a strong CIBIL score after borrowing a loan. Some smart tips to maintain a good CIBIL score are:

- Pay EMIs on time without any delay

- Do not use more than 30 to 40% of available credit

- Do not apply for multiple loans at a time

- Keep a track of credit reports

- Do not go for frequent loan inquiries

Missing one EMI will reduce the score by 50-70 points. It also affects individuals' future borrowing ability.

Conclusion

A 3 lakh personal loan may be manageable, but the interest rate depends on your credit profile. A CIBIL score of 725+ improves the chances of loan approval and reduces borrowing costs.

The small differences in interest rates can add up over time. This is the reason why a credit score is important. Individuals will get better terms by maintaining proper financial habits.

Frequently Asked Questions

Can I close my old credit accounts to improve my credit score?

No, closing old credit accounts might reduce the score.

Can a borrower with a 700 credit score apply for a personal loan?

Yes, a borrower with a credit score of 700 can apply for a loan at a high interest rate.

How much credit limit can I use?

You must use less than 30% of the credit limit to maintain a good score.

How much time does it take to improve the credit score?

The credit score may take several months to years to improve, depending on various factors.

Does Hero FinCorp offer better rates for high scores?

Yes, strong credit profiles are offered competitive rates.

Do frequent checks affect credit score?

No, soft checks have no impact on credit score.

When does the borrower receive the loan?

Normally, the loan is disbursed within a few hours to 1-2 days.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.