Does Cheque Bounce Affect CIBIL Score?

Have you ever issued a cheque that got bounced? This can be a difficult situation, and embarrassing too. Resolving this may require dealing with an additional fee or simply speaking to your banking representative about the issue, which is enough to make most people uncomfortable.

Besides these consequences, one question that comes to mind for most people is: Does a bounced cheque affect CIBIL scores, in addition to the financial and legal repercussions? Understanding what actually happens in scenarios like this is crucial and can help you respond calmly, without unnecessary panic.

This guide breaks down the impact of a bounced cheque on your CIBIL score, so you know how to deal with a situation like this if it were ever to occur.

Understanding CIBIL Score and Its Importance

A CIBIL score is a three-digit number that reflects your creditworthiness and ability to repay, ranging from 300 to 900. Higher scores position you as a dependable borrower in the eyes of banks, often leading to easier loan approvals and more favourable terms.

Lenders review this score for every loan or credit card application, considering factors such as your repayment history, credit utilisation, loan range, and payment consistency to assess overall risk.

What Is a Bounced Cheque?

A bounced cheque is one that your bank is unable to process, likely because your account has insufficient funds. This usually happens when the issuer’s account does not have enough balance at the time of clearing. Sometimes, however, a host of other factors can also result in a cheque bounce, including:

- Insufficient account balance

- Signature mismatch

- Incorrect date or overwriting

- Account closure or frozen accounts

- Discrepancies between the numerical and written amounts

When it comes to bounced cheques, there are some serious legal repercussions under the Negotiable Instruments Act of 1881, especially if you fail to make the payment within the set deadlines. Common penalties can include fines, receiving legal notices, or even facing court proceedings.

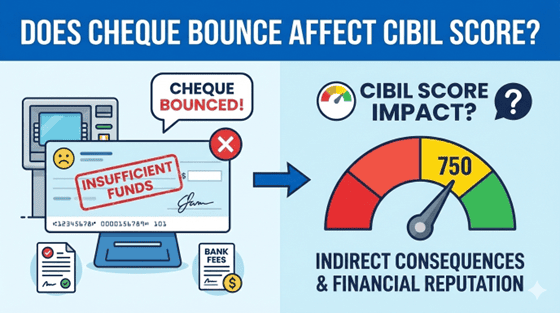

Does a Bounced Cheque Directly Affect Your CIBIL Score?

No, a bounced cheque does not directly affect your CIBIL score, but that doesn't mean it doesn't have indirect consequences (we address these in the next section). The reason is that credit bureaus only track credit-related transactions, such as loans, credit cards, and repayment history, not cheque clearances.

CIBIL records data reported by banks and financial institutions regarding credit facilities. Since a cheque bounce is a banking transaction and not a credit transaction by default, it does not automatically reflect on your credit report or lower your score in the process.

Also Read: Why Do Credit Scores Vary Across Credit Bureaus?

Indirect Impact of a Bounced Cheque on Your Creditworthiness

You're now aware that a cheque bounce does not directly reduce your score, but don't let this bring your guard down. Repeated or unresolved incidents can still hurt your overall credit profile, so you still have to be diligent every step of the way.

A bounced cheque will reduce your CIBIL score indirectly if it leads to:

- Legal action that results in default or settlement

- Delayed loan repayments due to linked ECS or cheque failures

- Negative lender perception during manual credit assessments

- Strained banking relationships that affect future credit approvals

Over time, cheque bounce consequences can make lenders cautious, even if your credit score looks healthy on paper.

Also Read: What Is A Crossed Cheque?

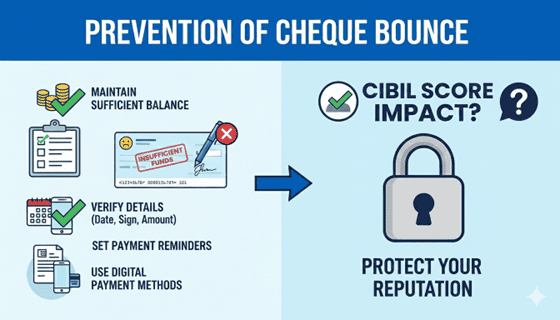

Prevention of Cheque Bounce to Protect Your Financial Reputation

Avoiding cheque bounce issues is often easier than fixing them later.

Simple cheque bounce prevention tips include:

- Keep enough balance in your savings account.

- Check the date, amounts, and signatures.

- Avoid using post-dated cheques unless absolutely necessary.

- Set up reminders to ensure payments are made on time.

- Use digital payment methods to better track your transactions.

Knowing how to prevent cheque bounce helps protect both your financial credibility and, equally importantly, your relationships with banks and lenders.

How to Handle a Cheque Bounce Situation

If a check bounces, reach out to the payee right away and sort out the payment within the notice period. If you receive any legal notices, reach out for legal advice on the best course of action. When you know how to deal with a bounced cheque, you get the benefit of preventing any form of escalation and maintaining your financial reputation.

Are you in urgent need of funds? Apply for a Hero FinCorp personal loan for quick disbursement to meet your financial needs.

Also Read: What are ACH Debit Return Charges and How to Manage Them

Frequently Asked Questions

1. Does a bounced cheque directly affect my CIBIL score?

No, bounced cheques don't appear directly on your CIBIL score, since credit bureaus only track things like loans and card payments, not bank cheque clearances.

2. Can a cheque bounce result in legal proceedings?

If you don't sort out the payment fast, the payee can take it to court under the Negotiable Instruments Act, which might mean dealing with fines or hearings.

3. What penalties are imposed for cheque bounce under the law?

The penalties for a bounced cheque could range from a fine to a legal notice. In certain cases, you may get involved in court proceedings to resolve the issue.

4. How can I avoid a cheque bounce on my account?

A few simple solutions are to keep your balance topped up in advance, always eyeball the signature and the matching figures in both numbers and words, and set up reminders. If possible, you should also try to switch to app-based or digital payments.

5. What happens if there are repeated cheque bounce incidents?

One-off bounces slide by without hitting your score, but repeated instances can make the lender consider you a risk, which in turn can affect all future transactions or loans. You could also face fines or legal notices.

6. Will a bounced cheque affect my ability to get a loan?

One bounced cheque may have little to no impact, but if this is a regular occurrence, lenders may become wary of approving loans in the future.