NOC for Loan Closure: Importance, Format, and Step-by-Step Process

Hero Introduction

You've done it - you've paid off your loan in full. Congratulations!

But your financial responsibility doesn't end with the final EMI payment. There is only one critical piece of paper you must have: a NOC (No Objection Certificate).

Without a NOC for loan closure, you may face issues with your credit report, legal challenges, or be unable to sell your security.

Here, we've explained why you require a NOC after loan closure, what information it includes, and how you can procure one. Understanding the importance of securing a NOC after loan closure is essential for every borrower.

What is NOC After Loan Closure?

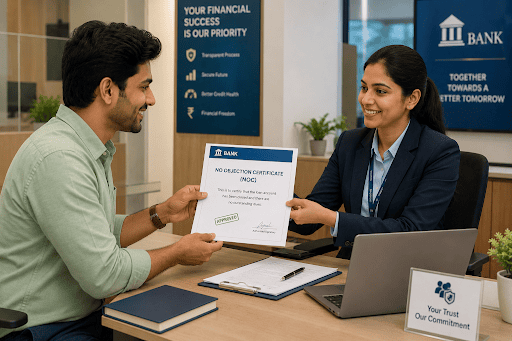

Your NOC (No Objection Certificate) is issued by your bank in which they say that you have cleared the total loan amount, and nothing is due to them.

Understanding what is NOC after loan closure is crucial for every borrower. This certificate serves as proof that:

- Your loan account is closed

- You owe no money to the lender

- The lender has no claim on your assets or income

- You're free to use the collateral (if any) as you wish

When you receive a NOC for loan closure, it typically arrives as a one-page letter on the lender's official letterhead with their stamp and authorised signature. For secured loans like gold, auto, or home loans, the NOC after loan closure also authorises the removal of any lien or hypothecation from your asset, giving you complete ownership and the right to sell or transfer it.

The NOC for loan closure is essential documentation that officially concludes your borrowing relationship with the lender and protects you legally.

Importance of Securing a NOC After Loan Closure

Understanding the importance of securing a NOC after loan closure cannot be overstated. This critical document serves multiple essential purposes for every borrower.

- Credit Protection: It provides proof that you've fulfilled your loan obligation, supporting your creditworthiness for future borrowing.

- Legal Safety: It protects you from false claims by the lender about outstanding dues or disputes.

- Asset Freedom: For collateral-based loans, the NOC enables you to sell, gift, or pledge your asset elsewhere without lender interference.

- Peace of Mind: It officially closes your relationship with the lender, eliminating any future complications.

Without an NOC, credit bureaus might show your loan as ongoing even after repayment, damaging your credit profile.

Consequences of Not Getting an NOC After Loan Closure

Failing to obtain a NOC for loan closure can have serious long-term consequences. Understanding the risks of not having NOC helps you prioritize this critical document immediately after repayment.

Impact on Credit Score and Creditworthiness

Even after repaying, your loan account may show as 'active' on your credit report, negatively impacting your credit score. This affects your eligibility for future loans.

Financial Loss and Continued Charges

Some lenders continue charging interest or processing fees on 'active' accounts. Without a NOC, it would be harder to establish you are not in debt.

Legal Battles and Lawsuits

The bank could resort to the recovery of funds or filing of a case for recovery of dues years later, thereby incurring unnecessary legal expenses.

Difficulty in Asset Transfer or Sale

For gold or auto loans, without an NOC removing the lien, you cannot legally sell, transfer, or pledge your asset.

How to Get NOC After Loan Closure: Step-by-Step Process

Learning how to get NOC for loan closure is straightforward if you follow these systematic steps:

- Request Immediately - Contact your lender within 7–10 days of final payment. Don't wait; timely requests expedite the process.

- Submit Required Documents - Provide your loan account number, final payment proof, and PAN/Aadhaar details.

- Verify Loan Status - Ask your lender to confirm your account is settled with zero outstanding dues.

- Receive NOC - The lender typically issues the NOC within 5–10 working days, either via post or email.

- Verify Details - Check that your name, loan account number, and closure date are accurate before accepting.

NOC for Loan Closure Format: What to Look For

A proper NOC for loan closure format should include specific elements to ensure its authenticity and legal validity.

Essential Components:

- Lender's official letterhead and contact details – Confirms the legitimacy of the NOC.

- Your full name and loan account number – Must match your original loan agreement exactly

- Loan closure date and final repayment date – Establishes when you completed repayment

- Clear statement: No outstanding dues – The core declaration in any NOC.

- Authorisation to release any lien or hypothecation – Critical for secured loans

- Lender's authorised signature and official stamp – Verifies authenticity

- Date of issue – Shows when the NOC was generated

For personal loans, the NOC for closure is typically brief (one page) and straightforward. For secured loans, it may include additional clauses about asset release.

Key Information in NOC for Personal Loan Closure

When you receive your NOC for personal loan closure format, ensure it contains these critical details to guarantee its authenticity and completeness:

- Loan Account Number - Must match your original loan agreement exactly

- Borrower Name - Appears exactly as it does in your identification documents

- Closure Status - Clearly states 'Loan Account Closed'

- Outstanding Balance - Shows 'NIL' or 'Zero'

- Date of Issue - When the NOC was generated

- Lender's Official Seal - Authentic stamp and authorised signatory confirming the NOC

- Contact Information - Lender's address and phone number for verification purposes

A properly formatted NOC can be verified by contacting the lender directly if you have any doubts about its authenticity or completeness.

Key Things to Remember While Applying for NOC

Securing your NOC for loan closure involves several important points to keep in mind throughout the process.

Apply Immediately After Loan Closure

Don't delay - obtain the NOC for loan closure within days of final repayment to ensure timely credit bureau updates and prevent misreporting.

Maintain Safe Records and Copies

Keep the original NOC in a safe locker and create digital/printed copies for your financial records.

Verify Details Before Accepting

Cross-check your name, account number, closure date, and lender details on the NOC before accepting it.

Update Credit Bureau Records

Share the NOC with credit bureaus (CIBIL, Experian, Equifax) to ensure your account is marked as 'closed' promptly and accurately.

Also Read: Difference Between CIBIL Score and Equifax

Removing Lien or Hypothecation After Getting NOC

For collateral-based loans (gold, auto, property), obtaining your NOC for loan closure is just the first step. The NOC for loan closure authorises lien removal, but you must complete additional procedures for removing the lien after the loan closure.

- Submit the NOC to the registrar (for property) or issuing authority (for vehicles)

- Pay any administrative fees for lien removal

- Obtain a release certificate confirming your asset is lien-free

This process typically takes 2–4 weeks. Don't attempt to sell collateral without completing this step-it can lead to disputes.

What If You Lose Your NOC?

Don't panic. You can request a duplicate NOC from your lender by providing:

- Original loan account details

- Proof of identity

- Written request letter

Most lenders issue duplicates within 3–5 working days, often free of charge. Some digital lenders provide instant duplicate NOCs via email, making recovery from a lost NOC even faster. Keep the original NOC and at least one photocopy in a secure location.

Frequently Asked Questions

How long does it take to get an NOC after loan closure?

Most lenders issue a NOC after loan closure within 5–10 working days of your request and final payment verification. Some digital lenders provide instant NOCvia email, significantly expediting the process. The time taken depends on the speed at which your lender works, and also how quickly you deliver your necessary documents post the repayment. Follow up with your lender on the processing time for receiving your NOC.

Is NOC required for all types of loans?

Yes, NOC is required for all borrowing types. Personal loans, auto loans, home loans, gold loans, and business loans all necessitate a NOC after loan closure. This mandatory document officially confirms loan repayment completion and protects you legally. Whether your loan was secured (collateral-based) or unsecured, obtaining a NOCshould be your priority after final payment.

Can I get an NOC before fully paying my loan?

No. A NOC is issued only after the entire loan amount, including interest and all charges, is completely repaid. Lenders cannot issue a NOC while any outstanding dues remain. Ensure full payment before requesting your NOC for loan closure to avoid delays or rejection of your application.

What details should be in the NOC format?

A proper NOC should include your full name, loan account number, loan closure date, final repayment date, lender's official details, and a clear statement confirming 'zero outstanding dues.' The document must have the lender's authorized signature and official stamp to validate the NOC. Verify all information matches your loan agreement before accepting the NOC.

Can I get a duplicate NOC if I lost the original?

Yes. If you've misplaced your NOC, contact your lender with proof of identity (PAN/Aadhaar) and account details. Most lenders issue a duplicate NOC within 3–5 working days, often free of charge. Some digital lenders provide instant duplicate NOC via email, making recovery quick and convenient.

Does NOC affect my credit score positively?

Indirectly, yes. A NOC ensures your account is marked 'closed' on credit reports, preventing negative impacts from an ongoing loan status. This proper documentation supports a healthy credit profile for future borrowing. Without a NOC for loan closure, your account might show as active, damaging your creditworthiness despite perfect repayment history.

Is there a charge for getting an NOC from the lender?

Most lenders issue a NOC for loan closure free of charge as part of their standard loan closure procedure. However, some may charge nominal fees for duplicate copies or expedited processing of your NOC. Always verify your lender's specific policy regarding NOC charges before requesting the document.

Ready to Close Your Loan Properly?

Getting an NOC after loan closure is a non-negotiable step. It protects your credit, prevents legal hassles, and gives you complete asset freedom.

If you're planning to take a personal loan and want to understand the full lifecycle-from approval to closure-explore Hero FinCorp's resources. We help borrowers make informed decisions at every stage. Check your personal loan eligibility today and understand the complete journey.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.