Loan NOC: What is a No Objection Certificate for Loan & Its Benefits

Clearing your loan repayments is an important financial milestone. But there is one more document that helps officially close the loop: a loan NOC. Many borrowers overlook it, even though this certificate can help maintain accurate records and avoid issues in the future.

What is a Loan NOC (No Objection Certificate/Letter)?

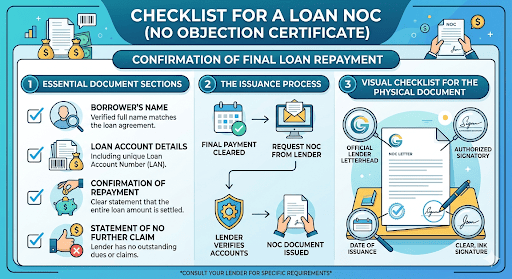

A loan NOC, or No Objection Certificate, is a document issued by a lender after a borrower has repaid the loan amount. It confirms that there are no pending dues against the loan.

A loan NOC letter includes details such as:

- Borrower’s name

- Loan account details

- Confirmation of repayment

- Statement that the lender has no further claim

A NOC for loan acts as proof that your financial obligation towards the lender has been completed.

NOC for Loan Closure: Why Is It Important?

A NOC for loan closure helps ensure your loan records are updated properly. Once you finish repayment, keeping this document safely can make future financial processes easier.

A loan NOC can also help with:

- Updating credit records

- Removing claims linked to secured loans

- Keeping proof of repayment for your records

How to Get a Loan NOC: Step-by-Step Process

The loan NOC process is simple when your repayments are complete. Here’s how to get NOC for loan:

- Complete all pending repayments: Ensure that your loan EMIs and any applicable charges have been cleared.

- Contact your lender: Reach out through the lender’s website, branch, or digital platform.

- Request the NOC certificate: Ask for the official loan NOC certificate after loan closure.

- Verify the details: Check your name, loan account number, and closure information before storing the document.

Many lenders now provide digital access to loan-related services, making it easier to track and manage your borrowing journey online.

Benefits of a Loan NOC Certificate

A loan NOC certificate offers several practical benefits:

Clear Title on Your Asset or Property

For secured loans, an NOC can confirm that the lender has no remaining claim over the asset once the loan is repaid.

Positive Impact on Credit Records

A loan NOC helps support accurate reporting of your closed loan account. This can be useful when reviewing your credit history.

Smoother Future Loan Applications

When you apply for new credit, having proper closure documents can make the verification process easier.

Legal Safeguard Against Future Disputes

A no objection certificate for loan works as written proof that repayment obligations have been completed.

Financial Peace of Mind

Keeping important documents like a noc certificate for loan helps you stay organised and prepared.

Also Read: Do Personal Loans Affect Your Credit Score?

What Happens If You Don’t Have a Loan NOC?

Not having a loan NOC may create difficulties when you need to prove that a loan has been closed. In some cases, outdated records may need additional follow-ups with the lender.

This is why collecting and storing your NOC after repayment is a useful financial habit.

Types of Loans That Require NOC

Different types of borrowing may require an NOC after closure, including:

Personal Loan

A personal loan NOC confirms that the unsecured loan has been fully repaid.

Two-Wheeler Loan

Borrowers may need an NOC to complete ownership-related processes after repayment.

Loan Against Property

For secured borrowing, an NOC helps confirm that the lender’s claim has ended.

Business Loan

A business loan NOC can help maintain clear financial documentation.

Conclusion

A loan NOC is a simple but valuable document that confirms your loan has been fully repaid. Keeping your loan NOC certificate safe can help you manage future financial needs with fewer complications.

Need quick funds for your next requirement? Check your eligibility for a personal loan with Hero FinCorp and complete the process online.

Frequently Asked Questions

What is the full form of NOC in a loan?

NOC stands for No Objection Certificate. It confirms that the lender has no pending claim after loan repayment.

Is a loan NOC the same as a loan closure certificate?

They are related documents. A loan NOC confirms no dues, while a closure certificate confirms the loan account is closed.

How long does it take to receive a loan NOC?

The timeline depends on the lender’s process after your final repayment is completed.

Do I get the NOC automatically?

Some lenders issue it automatically, while others may require a request after loan closure.

Does a loan NOC affect my CIBIL score?

A loan NOC does not directly change your CIBIL score. It helps confirm that your loan account has been closed.

Is there any charge for getting a loan NOC?

Most lenders provide a loan NOC after closure without additional charges. Check your lender’s terms for specific details.

What documents are needed to get a loan NOC?

You may need your loan details and basic identity documents to get apply for your loan NOC.

What should I do if I lose my loan NOC certificate?

Get in touch with your lender. They can aid you to get another copy after verification.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.