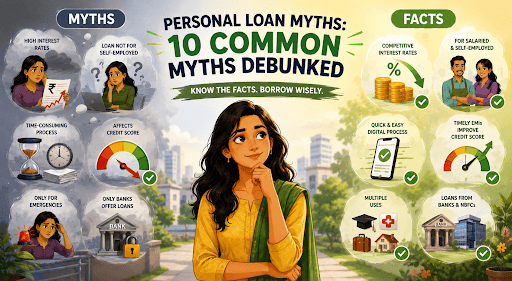

Personal Loan Myths: 10 Common Myths Debunked

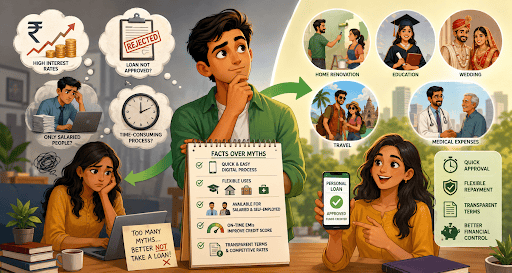

Armaan needed urgent funds to renovate his flat. But, he rejected a personal loan offer because he assumed high interest charges.

Yamini, a freelancer seeking to pay medical costs, also ignored the idea, believing she was ineligible for a personal loan.

Both were influenced by personal loan myths that deter you from making informed financial decisions.

In 2026, digital lending has made borrowing way easier. Understanding facts can help borrowers pick the best solution for their needs.

About Personal Loan Myths

Personal loans can be used for meeting short-term, emergency, and even long-term costs. Even today, people rely on unverified assumptions and are unsure about personal loan eligibility, approvals, and repayment.

Such personal loan myths create hesitation. Let’s separate fact from fiction and understand how to use personal loans responsibly.

10 Common Personal Loan Myths – Check Facts!

The top 10 personal loan myths are:

Myth 1: High Costs and Interest Rates

- Fact - Interest rates on personal loans can differ because of credit score, income, and debt management.

- Example - Two people getting the same personal loan amount can be offered different interest rates. A person who consistently pays all bills on time receives better terms than someone who has payment delays.

Myth 2: Applying for Multiple Loans Reduces Approval Chances

- Fact - It’s normal to compare loan options, but applying for lots of them in a short period can affect your credit score. This happens due to multiple hard inquiries.

- Example - Researching your eligibility first helps you avoid haphazard applications and protects your credit rating.

Myth 3: Personal Loans Are for Salaried Individuals Only

- Fact - Salaried, self-employed, or freelancers can get a personal loan if they meet the eligibility criteria.

- Example - A self-employed graphic designer can qualify just as easily as someone living on a salary, as long as they both prove they've got a steady income coming in.

Myth 4: The Personal Loan Application Process Is Time-Consuming

- Fact - Digital lending has made the process much simpler.

- Example - Leading banks now have digital apps for loan applications. You can do it all online - submitting your documents, waiting for verification, approval, and even having the money deposited in your account, no branch visit required.

Myth 5: Only for Financial Emergencies

- Fact - Personal loans can be used for all kinds of expenses, whether they are planned, immediate, or emergency.

- Example - You can take a personal loan for home renovations, education, weddings, vacations, and even medical emergencies.

Myth 6: Personal Loans Dip Your Credit Rating

- Fact - The fact is that paying EMIs on time enhances your credit score.

- Example - Paying personal loan EMIs shows lenders you’re reliable. This improves your score.

Myth 7: Only Banks Can Offer Personal Loans

- Fact - NBFCs that are RBI-approved and regulated offer personal loans too.

- Example: People prefer NBFCs for personal loans because of their online apps, quick approvals, and reliable customer support.

Myth 8: Personal Loans Are More Expensive

- Fact - Borrowing costs vary based on different financial products and personal situations.

- Example - Some people prefer personal loans with set monthly payments because it's easier to plan the repayments than with other types of loans.

Myth 9: You Can Only Have One Personal Loan at a Time

- Fact - Fact is, you can get more than one personal loan if you meet the requirements and show lenders you'll repay them.

- Example - A person paying off an existing personal loan might still be eligible for another cash loan, depending on lender policies.

Myth 10: You Can Use Personal Loans for Any Purpose

- Fact - The idea that personal loans are good for any old thing is a myth. Fact is, you've got flexibility, but there are limits.

- Example - Personal loans work for legitimate personal and financial needs. But you cannot use them for prohibited activities like speculative investments, illegal activities, gambling, or activities not approved by applicable laws and regulations.

Additional Insights on Personal Loans

Learn some basic facts and clear your understanding of myths about personal loans:

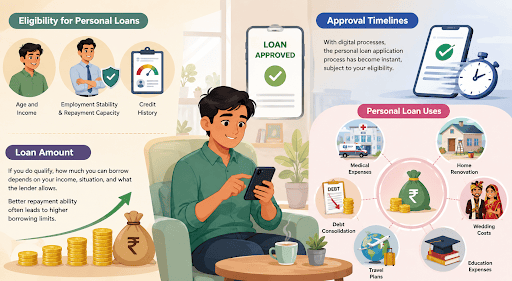

Eligibility for Personal Loans

The following factors influence loan approval and terms:

- Age and income

- Employment stability and repayment capacity are considered

- Credit history.

Loan Amount

If you do qualify, how much you can borrow depends on your income, situation, and what the lender allows. Those with better repayment abilities often get larger borrowing limits.

Approval Timelines

With digital processes, the personal loan application process has become instant, subject to your eligibility.

Personal Loan Uses

People take personal loans for:

- Medical expenses

- Home renovation

- Wedding costs

- Education expenses

- Travel plans

- Debt consolidation

Also Read: Planning Your Dream Day: Average Wedding Cost in India

Hero FinCorp's Personal Loan Solutions

When you are unfamiliar with the modern digital loan application systems, you could be influenced by personal loan myths. Hero FinCorp personal loan solutions simplify the borrowing experience with features like:

- Apply online with Hero FinCorp.

- Check your eligibility fast

- Consider flexible repayment options.

- The terms are transparent, and you get good interest rates based on your profile.

- Use their user-friendly Android/iOS app for all your digital lending needs.

If you need funds for planned or urgent expenses, get the best personal loan offers by checking your eligibility through Hero FinCorp's Instant Personal Loan journey.

Financial Choices Based on Facts - Not Loan Myths

People should make financial decisions or loan-based decisions based on facts, not personal loan myths.

Consider verifiable information about personal loans, and take into account your monthly expenditure, affordability, and repayment capacity before borrowing.

Read the fine print and opt for loan solutions, like Hero Fincorp's personal loan web journey, that complement your financial goals.

Frequently Asked Questions

Who can get a Hero FinCorp personal loan?

Eligibility criteria depend on age, income, occupation stability, ability to repay, and legal requirements.

How much can one borrow?

The personal loan amount is determined based on the borrower's eligibility, income, and credit profile.

How fast can you get loan approval?

Approval and disbursal vary depending on the verification and eligibility processes.

Can you use the loan for your business?

Personal loans are meant for personal use. However, several people also use personal loans to cover everyday business expenses. Always refer to the lender's policies regarding the end use of personal loans.

Will paying EMIs on time boost my credit score?

Yes. Making EMI payments on time can improve credit history.

Are there any hidden fees in HeroFinCorp personal loans?

No. It is better to check your loan agreement before you sign on the dotted line.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.