Personal Loan Without Credit Check: How It Works and Who Can Apply

Loan applications get rejected for all sorts of reasons. But one of the more frustrating ones is a low or absent CIBIL score, especially when the salary has been steady for years.

This situation is not unusual. Millions of Indians fall into what lenders call the "credit invisible" category, people who earn well but have simply never borrowed before. No defaults, no missed payments, just no credit history at all.

This personal loan is designed specifically for borrowers like this. Instead of relying solely on a credit bureau score, lenders assess income patterns, banking behavior, and repayment capacity to determine eligibility. It is a different method of assessment not an absence of one.

What is a No Credit Check Personal Loan?

A no-credit-check personal loan is an unsecured loan in which the lender considers income and banking history rather than CIBIL score when deciding eligibility.

Most regulated lenders do access some bureau data. The difference is that a low or zero score does not trigger automatic rejection here.

What the lender actually examines is salary consistency, average monthly credits, existing EMI obligations, and the employer profile over the past few months.

NBFCs use data analytics and alternative credit-scoring methods to provide a more holistic assessment of repayment capacity. Repayments on these loans are also reported to credit bureaus, so responsible borrowers build a credit file as they repay.

Who Can Apply for a Personal Loan Without a Credit Check?

Contrary to what many assume, this is not just a product for people with bad credit. The applicant base is actually quite wide. Lenders typically consider:

- Salaried employees with no prior borrowing history and a zero CIBIL score

- Self-employed professionals with six or more months of consistent bank deposits and ITR filing

- Gig workers and freelancers with verifiable platform or client income

- Individuals with a low credit score caused by limited credit use, not defaults

- First-time borrowers who have simply never taken credit before

While banks generally require a CIBIL score of 725 or above, many NBFCs work with scores of 650 or lower, and some go further, assessing income data alone when bureau history is insufficient.

A zero score and a defaulter profile are treated as two very different situations by most NBFCs.

How No Credit Check Loans Work: The Process

The whole process runs online, no queues, no branch visits, and no stacks of physical paperwork:

- Fill in personal and employment details on the lender's website or app

- Upload three to six months of bank statements for income verification

- The lender's internal system reviews average monthly credits, outflows, existing EMI deductions, and cash flow consistency

- Employer category and income stability feed into the risk calculation alongside bank data

- A loan offer gets generated with the amount, interest rate, and tenure options once the assessment clears

- The borrower reviews the EMI, rate, and tenure before accepting

- Under RBI's Digital Lending Directions 2025, the lender transfers funds directly into the borrower's bank account

Personal loans through NBFCs have grown at a CAGR of 33% over the last four years, and much of that growth is driven by exactly this kind of faster, income-based assessment model.

Check your Hero FinCorp personal loan eligibility here and see where you stand before applying.

Key Differences: Assessment Based on Income, Not CIBIL

At a traditional bank, the credit score is a gate. Fall below the threshold, and the application stops there, salary notwithstanding.

No-credit-check personal loan products from NBFCs operate on a different logic entirely.

Net monthly income, salary credit regularity, employer type, and total EMI load relative to income carry significantly more weight than past bureau history.

RBI guidelines currently cap total EMI obligations at 50% of net monthly income for unsecured loans, so affordability still gets assessed seriously.

The key shift is that a missed payment from three years ago holds far less power over the outcome than it would at a conventional lender. Current financial standing drives the decision, not old credit events.

Also Read: How to Get Quick Personal Loan of 4 Lakh Without Physical Documents

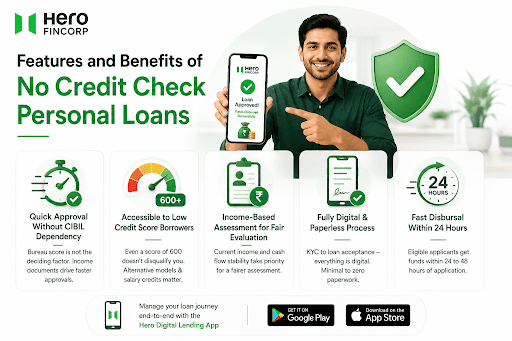

Features and Benefits of No Credit Check Personal Loans

Beyond accessibility, these loans offer several practical advantages worth knowing about. Here is a closer look:

Quick Approval Without CIBIL Dependency

Since the bureau score threshold does not act as a filter, applications move through the process faster. Income documents drive the decision, thereby significantly reducing the approval timeline.

Accessible to Low Credit Score Borrowers

As an extension of the income-first model, a CIBIL score of 600 does not automatically disqualify anyone. Alternative credit scoring models backed by NBFCs approve loans without relying only on credit scores, meaning consistent salary credits over 12 to 18 months can outweigh a weak bureau score.

Income-Based Assessment for Fair Evaluation

Building on that accessibility, the no credit check personal loan model treats a borrower with no credit history differently from one with a history of defaults. Current earnings and cash flow stability take priority, which is a fairer basis for evaluation for a large section of Indian borrowers.

Fully Digital and Paperless Process

From KYC to document submission to loan acceptance, the entire process happens on a phone or laptop. NBFC personal loans require minimal or zero paperwork compared to the lengthy documentation requirements of traditional banks. No in-person verification, no physical signatures at any stage.

Fast Disbursal Within 24 Hours

Rounding out the benefits, eligible applicants receive funds within 24 to 48 hours of completing the application. Manage the entire loan journey through the Hero Digital Lending & UPI App, available on Google Play and the App Store.

Detailed Eligibility Criteria for No Credit Check Loans

Requirements vary between lenders, but most NBFCs work within these general benchmarks:

- Age between 21 and 58 years

- Salaried applicants: net monthly income of at least Rs. 15,000

- Self-employed applicants: consistent deposits over six or more months with valid ITR

- Valid PAN card and Aadhaar card for KYC

- Active bank account with three to six months of statement history

- Total existing EMIs must not cross 50% of net monthly income per RBI guidelines

Credit score is reviewed where data exists, but does not serve as the primary filter for approval.

No Credit Check vs Regular Personal Loan: Comparison

Both products are unsecured and both disburse digitally, but the differences show up clearly once applications go in.

| Factor | No Credit Check Loan | Regular Personal Loan |

| Primary filter | Income and banking behaviour | CIBIL score and income |

| Minimum credit score | Low or none | Usually 700 to 750+ |

| Interest rate | Higher | Lower for strong profiles |

| Approval speed | Often within 24 hours | Can take several days |

| Eligibility | Broader | Stricter |

| Collateral | Not required | Not required |

How to Apply for a Personal Loan Without Credit Check

Before starting, keep PAN card, Aadhaar, salary slips, and bank statements ready. Having these at hand speeds the process up considerably.

- Visit the Hero FinCorp personal loan page or download the Hero Digital Lending & UPI App from Google Play or the App Store

- Enter employment details, monthly income, and the loan amount needed

- Upload bank statements and salary slips for salaried applicants, or bank statements and ITR for self-employed

- Complete e-KYC using Aadhaar and PAN

- Review the loan offer including EMI, rate, and tenure options

- Accept and receive the funds directly in the bank account

Important Considerations Before Applying

Before hitting submit, a few things deserve a proper look. Skipping these is where most borrowers run into trouble later.

- Verify Your Repayment Affordability: Calculate the proposed EMI against all existing monthly obligations first. RBI caps total EMI load at 50% of net monthly income for unsecured loans.

- Understand Interest Rates and Tenure Options: No credit check personal loan rates run higher than standard personal loans for strong credit profiles. A longer tenure lowers the monthly EMI but raises the total interest paid over the loan period. Running both scenarios before accepting any offer saves money in the long run.

- Confirm Income Documentation Requirements: Each lender has specific formats and minimum income thresholds. Checking these before starting avoids unnecessary delays.

- Avoid Multiple Applications Simultaneously: RBI guidelines now require a 30-day cooling-off period before a lender reassesses a rejected application. Applying to multiple lenders at once triggers several hard enquiries on the credit file.

Also Read: ₹50,000 Personal Loan Without CIBIL Score

Risks and Limitations of No Credit Check Loans

No product is without trade-offs, and these loans are no different. Going in with clear eyes helps borrowers make better decisions.

Interest rates are the most direct downside. Lenders pricing risk without a strong bureau score factor that uncertainty into the rate offered. Over a 36 or 48-month tenure, a rate four to five percentage points above a standard loan adds a meaningful amount to total repayment.

Sanctioned amounts for first-time borrowers tend to start conservatively. As repayment history builds, lenders open up higher limits on subsequent applications. Borrowers who clear a first loan cleanly tend to access significantly better terms the second time around.

Missed payments still carry full consequences here. Lenders report all repayments to credit bureaus regardless of how the loan was assessed at entry. Defaults damage the credit profile and raise borrowing costs across all future lenders, not just this one.

Also Read: How to Get 2 Lakh Loan Without Documents

Frequently Asked Questions

What is a no credit check personal loan?

A no credit check personal loan is an unsecured loan where lenders assess income, bank statement patterns, and employment stability rather than relying on CIBIL score as the primary filter.

Can I get a loan without CIBIL score check?

Regulated lenders still access some bureau data, but NBFCs do not use CIBIL score as the deciding factor. A zero or thin credit file does not trigger automatic rejection. Income consistency, banking behaviour, and existing EMI load drive the decision more than the score number itself.

How fast can I get approved without a credit check?

Many NBFCs disburse within 24 to 48 hours for eligible applicants. Having PAN, Aadhaar, salary slips, and bank statements ready before starting the application cuts processing time down considerably.

What documents do I need for a no credit check loan?

PAN card, Aadhaar, and income proof. Salaried applicants need three months of salary slips and bank statements. Self-employed applicants need six months of bank statements and one to two years of ITR. All documents go in digitally, no physical copies needed.

What are the interest rates for no credit check loans?

Higher than standard personal loans, with the exact rate depending on income level, employer category, and the lender's internal risk model. Personal loan interest rates in India generally range from 10% to 22%, with no credit check products typically sitting toward the higher end of that range. The confirmed rate appears in the loan offer after the full income assessment.

Can self-employed individuals get no credit check loans?

Yes. Lenders assess self-employed applicants on bank statement cash flows, ITR consistency, and deposit regularity. Six to twelve months of steady income credits in the bank account generally supports a strong application even without a formal salary slip.

What is the maximum loan amount without credit check?

Loan amount depends on income and the specific lender's policy. NBFCs offer personal loans ranging from Rs. 5,000 to Rs. 55 lakh depending on eligibility. For first-time borrowers without credit history, initial amounts tend to start conservatively.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.