Apply for loan on HIPL app available on Google PlayStore and App Store - Download Now

A heritage city with a strong IT/BPO base around Hebbal and Hootagalli, Mysuru combines steady salaried demand with a thriving self-employed silk-weaving and hospitality economy. Hero FinCorp, an RBI-registered NBFC, offers an instant Personal Loan in Mysore of Rs 50,000 to Rs 5 Lakh - collateral-free, fully digital and with transparent fees for confident EMI planning.

Here’s how you can apply for a personal loan from us:

The Personal Loan in Mysore is open to applicants who meet:

| Parameter | Requirement |

| Citizenship | Indian citizen residing in India |

| Age | 21 to 58 years loan application |

| Employment | Salaried or self-employed |

| Minimum monthly income | Rs 15,000 (subject to internal assessment) |

| Work experience | 6 months for salaried, 2 years for self-employed |

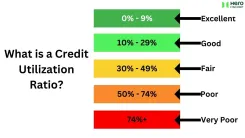

| Credit score | Ideally 725 or above |

Tip: You can check your eligibility instantly using the Personal Loan Eligibility Calculator on the website before applying.

Documentation for the Personal Loan in Mysore is paperless. The online journey validates PAN, Aadhaar and bank account details using regulator-approved digital methods. Keep your PAN and Aadhaar numbers ready, and the step is completed in minutes.

Happy Customers

Every 30 Seconds

App Installs

Locations Served

Fee schedule for the Personal Loan in Mysore - all line items upfront:

| Fee Type | Applicable Charge |

| Interest Rate | Starting from 18% per annum |

| Processing Fee | Minimum 2.5% + GST |

| Prepayment Charges | Not Applicable |

| Foreclosure Charges | 5% + GST |

| EMI Bounce Charges | Rs 350 per instance |

| Loan Cancellation | No cancellation charges via online app; interest paid and processing charges are non-refundable |

Disclaimer: The above rates are indicative and effective as of the latest Schedule of Charges published by Hero FinCorp. Actual rates may vary based on your credit profile, income, and other factors.

Across Mysore, the loan is most often used for:

Use the EMI calculator on the Hero FinCorp website or app to plan your loan. A sample - Rs 2.5 Lakh over 36 months - shows the indicative EMI and total interest. Modelling the EMI before applying helps avoid borrowing more than you need.

It's a great appreciation for obtaining the best personal loan with the fewest papers necessary and promptly disbursing loan ...funds. I truly appreciate your assistance. Simple procedure and a user-friendly interface. There are no problems, inquiries or anything else as long as you pay.

Herofincorp has great funds for various purposes. I got the best personal loan offer compared to interest rates, terms, and fees for ...my best financial situation. Thanks for your assistance.

It is a simple procedure. For financial emergencies, it is the best option. Thanks for their assistance. Adaptable and well-balanced. You can acquire an immediate loan transfer with Hero FinCorp.

Processing is quick, and had great experiences with this personal loan application and service. I appreciate customer support's gentle communication in helping the process go more smoothly. interest rates provided on the personal loan is the lowest in market. Overall experience good. I'm grateful.

I have been looking for a platform that allows me to borrow money quickly, it is convenient, safe and reliable to borrow money on this practical and reliable platform.

![]() Linkedin . 06 Aug, 2026

Linkedin . 06 Aug, 2026

![]() Linkedin . 05 Aug, 2026

Linkedin . 05 Aug, 2026

![]() Linkedin . 05 Aug, 2026

Linkedin . 05 Aug, 2026

![]() LinkedIn . 05 Aug, 2026

LinkedIn . 05 Aug, 2026

![]() Linkedin . 05 Aug, 2026

Linkedin . 05 Aug, 2026

![]() LinkedIn . 05 Aug, 2026

LinkedIn . 05 Aug, 2026

![]() LinkedIn . 04 Aug, 2026

LinkedIn . 04 Aug, 2026

![]() LinkedIn . 04 Aug, 2026

LinkedIn . 04 Aug, 2026

![]() LinkedIn . 03 Aug, 2026

LinkedIn . 03 Aug, 2026