Personal Loan vs Business Loan: What's the Difference?

- What is a Personal Loan?

- What is a Business Loan?

- Key Differences Between Personal Loan vs Business Loan in India

- Purpose and utilisation

- Eligibility criteria

- Interest rates and costs: Personal loan vs business loan rates

- Other charges and fees

- Tax implications for personal loans used for business

- When to Choose a Personal Loan

- When to Choose a Business Loan

- Make the Right Loan Choice for Your Financial Goals

- Frequently Asked Questions

Loans are not interchangeable. A personal loan usually handles personal obligations, while a business loan supports commercial activity. From documentation to repayment expectations, the structure changes depending on the loan type.

In this comparison of personal loan vs business loan, we outline the key distinctions that matter.

What is a Personal Loan?

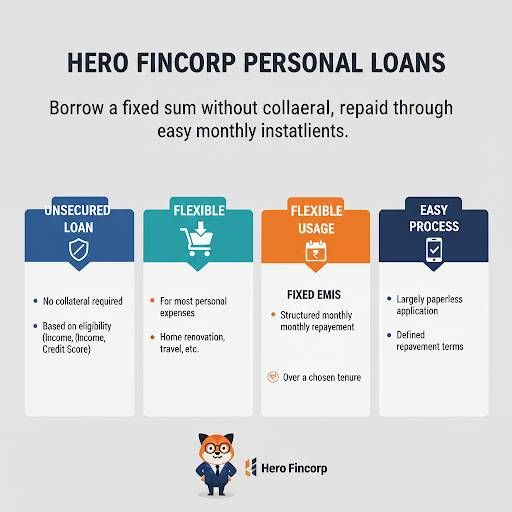

With a personal loan, you borrow a fixed sum without pledging any asset. You then repay the amount through structured monthly installments.

Here are some key features:

- Unsecured loan: No collateral required

- Flexible usage: Funds can be used for most personal expenses

- Fixed EMIs: Structured repayment over a chosen tenure

- Eligibility-based approval: Income, credit score and repayment capacity matter

Hero Fincorp offers personal loans with a largely paperless application process and defined repayment terms.

What is a Business Loan?

Companies take business loans to cover expenses like inventory, machinery or expansion plans. The lender evaluates the business’s financial position as part of the approval process.

Key features include:

- Higher loan amounts: Usually suited for business-scale funding needs

- Business-only usage: Loan amount is intended for operational needs

- Set repayment structure: Paid back through regular EMIs over an agreed period

- Financial review: Approval depends on turnover and repayment ability

Also Read: Top-Up Loan vs. Personal Loan: Which One Should You Choose?

Key Differences Between Personal Loan vs Business Loan in India

The table below highlights the differences between a business loan vs personal loan.

| Basis of Comparison | Personal Loan | Business Loan |

| Purpose | Used for individual financial needs | Used strictly for business requirements |

| Usage Restrictions | Generally flexible | Must be used for business activities |

| Loan Amount | Usually lower, linked to personal income | Often higher, linked to business turnover |

| Eligibility | Based on income, credit score and repayment capacity | Based on business vintage, turnover, profits and credit profile |

| Documentation | KYC, income proof, bank statements | Business registration, financial statements, GST returns |

| Tenure | Commonly 1–5 years | Often 1–4 years, depending on lender |

| Tax Benefit | Typically none | Interest may be treated as a business expense |

Knowing the difference between business loan and personal loan helps you match the loan type to your financial need.

Purpose and utilisation

A personal loan is commonly taken for expenses such as medical treatment, education, or consolidating debt. Lenders usually allow flexibility in how the money is used.

A business loan may be used for working capital, buying stock, upgrading machinery or expanding operations.

Eligibility criteria

Personal loan eligibility is assessed based on your monthly income, employment stability, credit score and current liabilities.

Business loan eligibility focuses more on the company’s financial position. Lenders examine aspects like annual turnover, profit levels, and credit history.

Interest rates and costs: Personal loan vs business loan rates

Personal loan interest rates are shaped mainly by your credit score and how stable your income is. In the case of a business loan, lenders look at turnover, profitability and the company’s credit standing.

Other charges and fees

Common additional charges include:

- Processing fees: Often calculated as a percentage of the loan amount

- Prepayment or foreclosure charges: May apply for early repayment

- Late payment penalties: Charged for missed EMIs

- Administrative or documentation fees: As per lender policy

Tax implications for personal loans used for business

If the funds are used strictly for business purposes, certain tax considerations apply:

- The interest paid may be claimed as a business expense

- Proper records of how the funds were used are necessary

- The principal repayment does not qualify for deduction

When to Choose a Personal Loan

Choose personal loan options when the requirement is strictly personal and not linked to business activity. It can be suitable if:

- You need funds for medical expenses, travel, weddings or education

- You want to combine multiple debts into a single EMI

- You prefer an unsecured loan without pledging assets

- You have a stable income and a healthy credit score

You can also apply through the Hero FinCorp personal loan app for Android and iOS, which allows you to check eligibility and complete the application online.

Also Read: What Is A Business Plan And Why Do You Need One?

When to Choose a Business Loan

Choose business loan financing when the funds are meant for business use. This may be appropriate if:

- You require working capital to manage daily operations

- You plan to buy stock, equipment or upgrade infrastructure

- Your business has consistent turnover and financial records

- The funding requirement exceeds personal loan limits

Make the Right Loan Choice for Your Financial Goals

A personal loan works well for individual expenses and offers flexibility in usage. A business loan is more suitable when funds are required for operations, working capital or expansion.

Hero FinCorp offers both personal and business loan options with a simple online process. Explore Hero Fincorp's loan options and use the personal eligibility calculator to find the loan that matches your requirement.

Frequently Asked Questions

Can I convert personal loan into a business loan later?

Personal and business loans are structured differently and follow separate eligibility rules. If your needs change, you must submit a fresh application for a business loan.

How does my credit score affect personal vs business loan approval?

Your credit score directly affects approval and the interest rate offered. A stronger score works in your favour.

Are there any government schemes or subsidies for business loans in India that I should be aware of?

Pradhan Mantri Mudra Yojana (PMMY) is one scheme that supports small businesses and MSMEs by facilitating access to formal credit.

What documents are typically required for a Hero FinCorp business loan vs a personal loan?

Personal loans generally require KYC and income proof. Business loan documentation typically includes registration certificates, financial statements, GST filings and bank statements for the business account.

Does Hero FinCorp offer top-up options for existing personal or business loans?

If you have maintained timely EMIs, you may qualify for a top-up loan. Hero FinCorp evaluates your repayment behaviour and financial standing before making a decision.

How quickly can I get funds disbursed after approval from Hero FinCorp?

After final approval and document checks, personal loan amounts are often disbursed within a brief period.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Two terms that sound almost identical but represent very different stages of the loan process. Mixing them up costs time, sometimes triggers an unnecessary hard enquiry on the credit report, and occasionally sets up expectations that the final application cannot meet.

Flight fares between Delhi and Goa have been known to double in a single week. Spotting a good deal is one thing. Having the full amount sitting in your account on the same day is a different problem entirely.

Seeing a three-digit number flash on your credit report can feel like opening a report card. But when that number reads credit score 777 is it good or bad? In short: it’s not just good, it’s excellent.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.