What Is a CIF Number and Why Does It Matter?

Most bank customers know their account number. Fewer know their CIF number, and even fewer know what it actually does. That is a gap worth closing, because your CIF sits at the centre of your entire banking relationship with any given bank.

Understanding it takes about five minutes and can save you a lot of confusion the next time a branch asks for it.

Understanding the CIF Number

Your CIF number is the reference your bank uses to retrieve your complete customer profile in a single request. Instead of searching through separate records for your savings account, fixed deposit, and home loan, the bank enters a single number and sees them all together.

The number is assigned when you open a bank account. Every product you add after that, another savings account, a recurring deposit, a credit card, gets linked to the same CIF. This is why it stays with you even if you shift branches. Your profile does not move to a new CIF; it stays put, and your new branch accesses the same one.

CIF Full Form and Its Significance

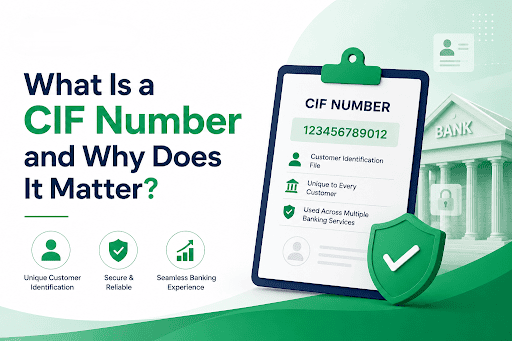

CIF stands for Customer Information File.

Here is what that file typically contains:

- Your basics, like full name, date of birth, PAN, and Aadhaar, if you have linked it

- The address proof and identity documents you submitted, plus whether your KYC is currently valid or pending renewal

- Every account you hold with that bank

- Borrowing history, such as loans you are currently repaying, EMI amounts, and credit lines you have already closed.

- Investment links like demat account, mutual fund folios, and PPF held with the same bank

- Contact and communication records, including registered mobile number, email, and nominee details

When a bank officer says they need your CIF to update your address or verify your KYC, this is the file they're referring to. It is also what loan officers access when you apply for credit, to check your full relationship with the bank before approving.

Also Read: Loan Repayment Plans: Types, Changes & Tips

How to Check Your CIF Number: Step-by-Step Guide

Offline Methods

- Passbook: The most reliable offline method. Open the first page of your passbook. Most Indian banks print the CIF number here alongside your account number and branch details.

- Cheque book: Some banks print the CIF on the first leaf or the inside front cover of the cheque book.

- Account opening welcome kit: The documents you received when opening your account usually include the CIF number in the customer summary sheet.

- Branch visit: Walk into your home branch with a valid photo ID. After identity verification, the staff will give you your CIF number on the spot.

Online Methods

- Mobile banking app: Log in and navigate to Account Details or Profile. Most major bank apps display the CIF number in this section.

- Internet banking: Log in to your bank's net banking portal. Go to Account Summary or Profile Information. The CIF number is usually listed alongside your account number.

- E-statements: PDF account statements sent to your registered email often include the CIF number in the header or account information section.

Importance of the CIF Number in Banking

The CIF number is not just administrative housekeeping. It has a direct impact on how quickly and smoothly your banking requests get handled.

- Customer identification: Banks have millions of customers. The CIF lets bank staff access your complete profile instantly, without having to repeat details across multiple requests.

- KYC compliance: Under RBI guidelines, banks must maintain current KYC records for all customers.

- Branch transfers: If you shift your home branch, your CIF follows you.

- Personalised services: Banks use CIF data to calculate your Total Relationship Value and Customer Relationship Value, determining your eligibility for pre-approved offers and loyalty benefits.

Advantages of Having a CIF Number

- All your accounts, fixed deposits, and loans sit under one profile, so you never have to explain your full banking history from scratch at every branch visit.

- KYC verification, loan applications, and account updates are processed faster because the bank already has your verified documents on file.

- Shifting branches does not disrupt your banking. Your CIF number is the same regardless of which branch you walk into.

- Pre-approved loan and credit card offers are generated based on your CIF data, which reflects your actual relationship with the bank.

- Transaction monitoring linked to your CIF makes it easier for the bank to flag unusual activity and protect your accounts from fraud.

CIF Number vs IFSC Code: Key Differences

Both appear on your bank documents and are asked for in different situations. They serve completely different purposes.

| Full Form | Customer Information File | Indian Financial System Code |

| What it identifies | The customer, not the account | A specific bank branch |

| Format | 8 to 11 digits (varies by bank) | 11 alphanumeric characters |

| Who uses it | The bank internally manages your profile | Sender's app or bank, to route transfers |

| Needed for | KYC updates, loan applications, and account linking | NEFT, RTGS, and IMPS transfers |

| Changes if you shift the branch? | No, it stays the same within the bank | Yes, each branch has its own IFSC |

| Visible on | Passbook, account statement, net banking profile | Cheque book, bank's website, RBI directory |

Your CIF is about who you are as a customer. Your IFSC code is the code for your bank branch. You will need your IFSC code when someone sends money to you or when you set up a transfer.

Also Read: NEFT vs. RTGS vs. IMPS vs. UPI: Key Differences

Frequently Asked Questions

Can one customer have multiple CIF numbers in the same bank?

Opening accounts at different branches without checking for an existing profile can create duplicate CIFs. If you suspect this, visit your home branch. Most banks can merge records into a single profile without hassle.

Is it safe to share my CIF number with others?

Your CIF number alone cannot move money or access your accounts, so it is not as sensitive as your UPI PIN or net banking password.

Does the CIF number change when opening new accounts?

No, the purpose of the CIF number is to maintain your complete banking history, which stays linked to it.

How can I verify the authenticity of a bank representative asking for my CIF number?

No genuine bank employee will call you out of nowhere and ask for your CIF number over the phone.

What should I do if I cannot find my CIF number?

Start with your passbook; it is usually printed on the first page. If your passbook is not handy, open your bank's mobile app and look under Account Details or Profile. It usually shows up there, too.

Can the CIF number be used for transactions outside the bank?

No. It is strictly an internal reference number that the bank uses to manage your customer profile on their end. You will never be asked to enter your CIF number to make a payment, send money, or complete any transaction. UPI transfers use your UPI ID or mobile number. Bank transfers use your account number and IFSC code. If anyone ever asks you to provide your CIF number to complete a transaction, that is a red flag worth taking seriously.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.