What Are Financial Obligations in Loans?

Ever wondered what you’re really signing up for when you take a loan? Financial obligations in loans go beyond just borrowing money. They’re the commitments you make to repay it on time, with interest, and under specific terms.

Understanding these obligations upfront helps you avoid surprises and stay in control of your finances from day one. Read on to know more.

Understanding Loan Obligation Meaning

Loan obligation is a legally binding commitment that affects your financial future, borrowing capacity, credit score and so on. When you borrow money in the form of a loan, you sign a legal contract.

This financial obligation in loans includes repaying the principal amount, interest charges, processing fees, and also adhering to specific terms & conditions set by the lender.

Having a clear understanding of these obligations helps you avoid debt traps and also build a strong financial foundation.

Also Read: What Is Personal Financial Management (PFM)? Definition, Full Form, Tools, and Apps

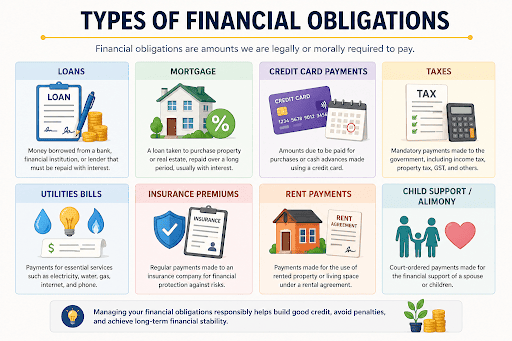

Types of Financial Obligations

Understanding the different types of financial obligations helps you manage repayments better and avoid penalties. A few of these types are-

a. Personal Loan Obligations

Personal loan obligations refer to the fixed commitments where you borrow a specific amount and repay it through Equated Monthly Installments (EMIs) over a defined tenure.

- These loans are usually unsecured.

- There is no collateral required.

- Personal loan obligations often carry higher interest rates compared to secured loans.

b. Credit Card Obligations

Credit card obligations are generally more flexible but can become costly if not managed carefully.

- When you use a credit card, you’re required to either pay the full outstanding amount by the due date or at least the minimum amount due.

- While you may have the option to pay a minimum due, carrying forward the balance attracts high interest charges.

- Managing these financial obligations requires paying the full outstanding amount whenever possible.

c. Secured Loan Responsibilities

Secured loan obligations are tied to loans backed by collateral, such as a home loan or car loan.

- These typically have lower interest rates compared to unsecured loans.

- The risk is higher as failure to repay can lead to loss of the pledged asset.

- Timely repayments are crucial to protect your assets and maintain financial stability.

Factors Affecting Total Financial Obligations

Here are some factors that have a bearing on your financial obligations in totality. They include the following-

- Income Level: The income level will determine how much obligation you can take up. More income will imply more obligations, but at the same time, you need to save as well.

- Liabilities: Liabilities like outstanding loan repayments or credit card payments will also affect your financial obligations.

- Interest Rates: Higher interest rates will mean higher amounts that you need to repay over the course of repayment.

- Tenure of Loan Repayment: Long tenures of loan repayments will lower monthly obligations but will result in high interest payments.

- Lifestyle Choices: Lifestyle choices like heavy credit card usage or luxurious purchases will affect your financial obligations as well.

- Market Conditions: Market conditions, like inflation, might also affect your financial obligations.

Also Read: Simple Steps to Effectively Manage a Debt Repayment

Smart Strategies to Manage Financial Obligations

Effective management of financial liabilities requires clarity of purpose and disciplined action. Some of the strategies you could use here include-

- Write down all your financial liabilities in one place, such as EMI, credit card payments, rent, and utility bills, so that you have a clear picture of your financial liabilities.

- Create a realistic budget that ensures that you give priority to your essentials and limit your unnecessary spending.

- Make timely payments using automated processes to save yourself from paying extra for being careless.

- Create an emergency fund to be prepared for unexpected expenses.

- Ensure debt consolidation and negotiation with creditors.

- Review your financial plan periodically.

Why Understanding Financial Obligations Matters?

Understanding financial obligations is essential for maintaining stability and making informed financial decisions. Knowing your responsibilities also help you plan your income, avoid missed payments, and protect your credit score.

Similarly, the loan obligation highlights your duty to repay borrowed funds within agreed terms, including interest and timelines.

When you clearly understand these obligations, you can budget more effectively, reduce financial stress, and avoid penalties or legal issues.

Closing Thoughts

When you clearly understand your financial loan obligations, managing repayments becomes simpler and far less stressful. And if you’re looking for a reliable way to borrow smartly, the Hero FinCorp Personal Loan app makes it easy with transparent terms and flexible options.

Contact us today to know your eligibility and stay on top of your financial commitments with confidence.

Frequently Asked Questions

1. What constitutes a financial obligation in loans?

A financial obligation in loans is a legally binding commitment to repay borrowed money, including principal, interest, and fees, according to agreed terms.

2. How does loan tenure impact total financial obligation?

Loan tenure significantly impacts total financial obligation by creating a trade-off between monthly cash flow and total interest costs.

3. Can prepayment reduce financial obligations?

Yes, prepayment reduces financial obligations by lowering the outstanding principal amount, which decreases the overall interest payable.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.