Debt Trap: Meaning, Warning Signs & How to Avoid It

- What is the Meaning of a Debt Trap?

- How Does a Debt Trap Work? A Step-by-Step Breakdown

- Key Warning Signs That You Are in a Debt Trap

- Common Causes of a Debt Trap in India

- How to Get Out of a Debt Trap - Practical Strategies

- Responsible Borrowing: How to Avoid a Debt Trap Before It Starts?

- Small Repayments Can Turn Into Bigger Financial Pressure

- Frequently Asked Questions

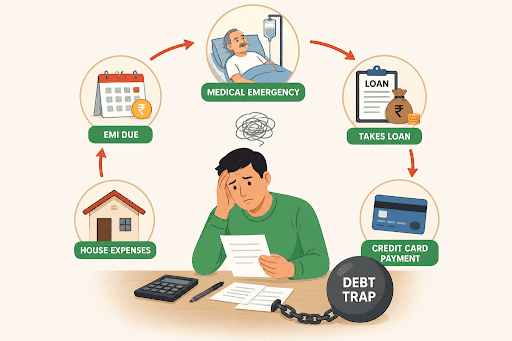

A debt trap starts when loan repayments become difficult to manage with your regular monthly income. People often take another loan or use a credit card to pay existing dues, but the payments keep piling up rather than reducing. After a point, a large part of the salary goes toward EMIs, interest, and pending bills each month.

What is the Meaning of a debt trap?

Rohit’s salary used to last comfortably till the end of the month. Then his father suddenly needed medical treatment, and he took a personal loan to manage the hospital bills. A few months later, one EMI, a credit card payment, and house expenses all landed at once, so he borrowed again just to avoid missing payments.

After that, things slowly began to slip. Part of his salary disappeared into repayments the moment it arrived, but the total debt still did not reduce. That is what a debt trap looks like. A person keeps taking new loans to cover older payments, but the financial pressure continues to grow month after month.

How Does a Debt Trap Work? A Step-by-Step Breakdown

Debt traps look manageable at first, but the repayment pressure starts building month after month.

Step 1: A person takes a loan or starts using a credit card more often.

Step 2: Monthly repayments begin to reduce available funds.

Step 3: Another loan helps cover older dues.

Step 4: Interest charges and penalties increase total repayments.

Step 5: Borrowing becomes necessary to manage regular expenses.

For example:

Monthly salary = ₹50,000

EMIs = ₹25,000

Credit card bill = ₹12,000

Money left = ₹13,000

Once rent, groceries, fuel, and bills are covered, almost nothing remains. Many people then borrow again to manage the month ahead.

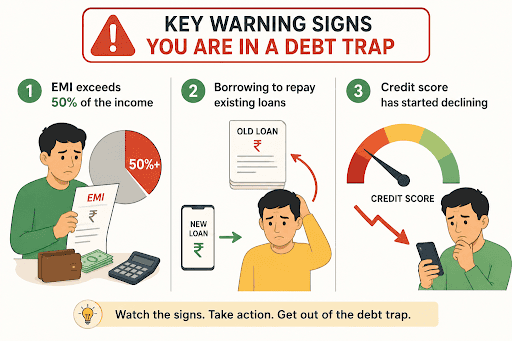

Key Warning Signs That You Are in a Debt Trap

A debt trap has very small warning signs. If you look for these signs at the beginning, you will come out of the trap soon.

Your EMI Payments Exceed 50% of Monthly Income

Your salary arrives, but most of it disappears into EMI payments within days. Saving money becomes difficult even in normal months.

You Are Borrowing to Repay Existing Loans

One loan slowly starts paying for another one. Many borrowers begin depending on credit cards or instant loan apps to avoid missing earlier EMIs.

Your Credit Score Has Started Declining

Late payments and repeated borrowing slowly affect your credit score. At some point, even getting a standard loan becomes more expensive.

Common Causes of a Debt Trap in India

Debt traps usually form from habits people do not think twice about at first.

Overspending and Lifestyle Inflation

As income increases, people tend to spend more rather than save. You shop for things that you don't even need. This habit of careless spending creates a debt trap for most people.

Dependence on High-Interest Borrowing

Credit cards and short-term loan apps charge very high interest rates. The debt grows quickly when borrowers use them regularly.

Lack of an Emergency Fund

One medical emergency or a sudden job loss can financially disrupt everything. Without savings, most people turn to borrowing immediately.

Misuse of Buy Now Pay Later (BNPL) and Digital Loan Apps

Small delayed payments may not feel serious at first. After a few months, several small repayments together can become stressful to manage.

Also Read: Buy Now Pay Later vs EMI: What You Need to Know

How to Get Out of a Debt Trap - Practical Strategies

Getting out of debt pressure takes time. Most people improve their situation slowly, not overnight.

Prioritise High Interest Debt First (Avalanche Method)

Start with loans charging the highest interest. Clearing them first reduces pressure more quickly.

Consolidate Multiple Loans Into One

Managing several EMIs together becomes mentally exhausting after a point. Debt consolidation helps combine repayments into one loan.

Build a Budget Around Debt Repayment

Tracking spending properly helps borrowers understand where money disappears every month. Small spending cuts often create more breathing space than expected.

Seek a Loan Balance Transfer at Lower Interest Rates

A lower interest rate can reduce monthly repayment pressure. Many borrowers shift loans for this reason.

Consult a SEBI-registered financial advisor or Credit Counsellor

Some situations become easier with professional guidance. Financial advisors can help borrowers create a realistic repayment plan.

Responsible Borrowing: How to Avoid a Debt Trap Before It Starts?

Check your monthly EMIs before taking another loan. If repayments already take away a big part of your salary, another EMI can quickly create financial pressure. Many people ignore this and focus only on quick approval.

Daily expenses can also quietly push people towards unnecessary borrowing. Instead of depending too heavily on credit cards, BNPL offers, or loan apps, try building a small emergency fund. Even small savings can help you manage sudden expenses without taking another loan.

Small Repayments Can Turn Into Bigger Financial Pressure

Debt problems often grow quietly. One missed payment or another small loan may not seem serious at first, but the pressure can build faster than expected when repayments keep increasing month after month.

Hero FinCorp helps borrowers manage loans more comfortably with easy tracking and digital access through the personal loan app for a. You can check EMIs, repayment details, and loan information anytime in one place. Apply now and stay in better control of your finances before debt becomes difficult to handle.

Frequently Asked Questions

What is the difference between debt and a debt trap?

Debt means borrowing money and repaying it within the agreed time. A debt trap is borrowing money in a loop and not being able to repay any loan.

What is a safe EMI to income ratio to avoid a debt trap?

Most experts recommend keeping total EMIs below 40% of monthly income.

Can a debt trap affect your CIBIL score?

Yes. When you miss EMIs or delay repaying your loan, your CIBIL score starts to decline.

Is debt consolidation always a good solution for a debt trap?

Yes. Debt consolidation turns your multiple loans into a single loan. This helps you repay the existing loan without taking a new loan.

What role do digital lending apps play in creating a debt trap in India?

Digital lending apps provide easy approvals of high-interest loans. People start taking more loans to repay the previous loan amounts.

How long does it take to recover from a debt trap?

There is no fixed recovery period from a debt trap. It usually depends on many factors, such as income, debt amount, and repayment discipline.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.

Related Blogs

Five years ago, getting a personal loan in India meant taking a half-day off work, collecting salary slips, and waiting two weeks for a decision...

One has to submit a comprehensive application with a wealth of details to apply for a personal loan. Lenders then review your details, verify documents, and assess your repayment capacity before approving the request.

Your loan EMI reaches the lender on time every month. Your insurance premium gets paid without any reminders. Even your SIP continues without any extra effort from your side. Most people enjoy this convenience but rarely stop to think about what keeps these payments running smoothly.

Did You Know

Disbursement

The act of paying out money for any kind of transaction is known as disbursement. From a lending perspective this usual implies the transfer of the loan amount to the borrower. It may cover paying to operate a business, dividend payments, cash outflow etc. So if disbursements are more than revenues, then cash flow of an entity is negative, and may indicate possible insolvency.