Micro Credit:Definition, How it Works & Importance

Ramesh needed funds, but there was no lending option available to him. When he researched his options, he learned about microcredit.

He applied for it to meet his funding requirements. Microcredit is a provision of small funds to individuals who do not have access to traditional lending services.

Let's explore microcredit in detail, including its types and eligibility criteria.

Micro Credit Meaning, Definition, and History

Microcredit is a small loan offered to individuals or groups with no access to traditional lending options. It is designed for people living in rural or semi-urban areas who want to start a small business but lack the money.

Micro credit became popular in the 1980s when Professor Muhammad Yunus founded Grameen Bank. He wanted to offer small loans to individuals who could not access traditional lending options because of a lack of collateral and lower socio-economic conditions. The initiative led to the establishment of many microfinance institutions worldwide. In India, microfinance started to gain popularity in the 1990s and was introduced in 1994.

Features and Benefits Of Microcredit

Microcredit loans help low-income individuals become financially independent. Here are the features of microcredit:

- It is for low-income groups or individuals in semi-urban and rural areas

- Based on repayment history and necessity, borrowers are eligible for repeat loans

- These loans can be used for employment or entrepreneurship

- The loans are collateral-free with low interest rates

- Microcredit helps encourage social cohesion and supports sustainable development

- Individuals can generate income through employment or business, which helps reduce poverty

How Micro Credit Works?

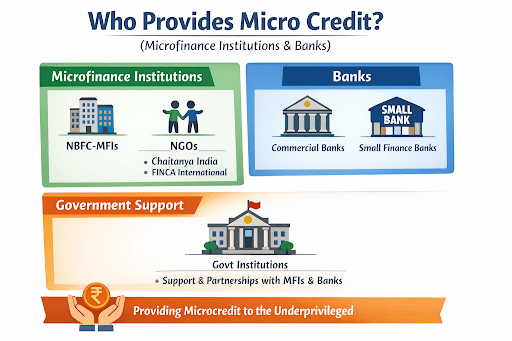

Microfinance Institutions (MFIs) or Non-Governmental Organizations (NGOs) operate micro credit. These institutions specialize in providing financial services to the underprivileged. They provide small loans to groups or individuals, often without any collateral. These loans are usually used for income-generating activities and have affordable interest rates.

In many cases, borrowers create a group in which each member is responsible for ensuring that others pay their loans. If one member fails, the whole group is affected, fostering a sense of responsibility. Some schemes may require the borrower to deposit a share of their income into a savings account. Once the borrower repays the loan, they can withdraw the full amount from the savings account.

Also read: Benefits of CIBIL Score: Why a Good Credit Score Matters

Types of Microcredit

There are various lending options available under microcredit. Here are the types of microcredit:

- Microloans: These are small loans without any collateral. They help borrowers build a credit history.

- Micro Savings: These loans do not require borrowers to maintain a minimum balance.. These loans encourage the habit of saving and help individuals earn interest on their deposits.

- Micro Insurance: It provides coverage to microloan borrowers at a low rate of premium. Individuals and families receive coverage for illness or other emergencies.

Also Read: Small Personal Loan or Mini Loan: How Are They Different?

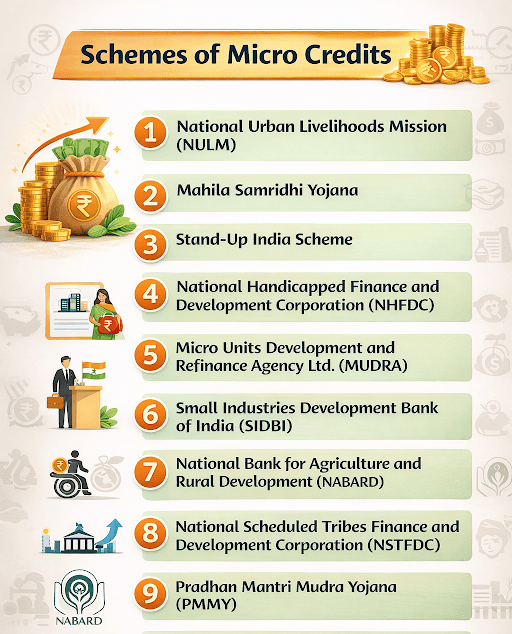

Micro Credit Operation Channels in India

Micro credit is operated mainly by SHG – Bank Linkage Programme (SBLP) and Microfinance Institutions (MFIs) in India.

SHG – Bank Linkage Programme (SBLP)

Launched by NABARD in 1992, the scheme supports women in economically backward classes in self-help groups. The women in self-help groups contribute their savings, which are later used to fund activities.

Microfinance Institutions (MFIs)

Under this channel, a group of 4-15 individuals can avail of loans either as a group or individually.

Apart from these channels, there are certain banks and non-profit social organisations that provide micro credit.

Challenges and Criticisms of Micro Credit

Here are the challenges and criticisms of micro credit:

- Borrowers use the loan to fund daily expenses instead of growing their business, which leads to excessive debt

- Some MFIs charge a higher rate of interest, which makes repayment harder

- The governance might be tricky. For example, there is a lack of awareness and newer technological challenges in adoption.

Manage Your Finances With Hero Fincorp

Microcredit loans support people without access to traditional lending options. This way, it helps these individuals start their earnings and improve their standard of living.

Hero Fincorp also offers personal loans to support emergencies or business needs such as working capital, expansion, and more. Simply install the instant loan app and complete the application process.

Frequently Asked Questions

Is microcredit the same as microfinance?

No. Microcredit focuses on short-term loans, while microfinance has a broader focus, including loans, savings, insurance, and money transfers.

What are the eligibility criteria for micro credit?

All microcredit schemes have specific requirements. Check these before applying.

What is the typical loan amount for micro credit in India?

The loan amount depends on the borrower, their income, and the purpose.

How is microcredit repaid?

Microcredit is repaid in small and regular installments.

Can microcredit help improve financial inclusion?

Microcredit helps people with no access to regular banking. It gives a chance to earn and also build a credit history, giving more opportunities in the future.

Disclaimer: The information provided in this blog post is intended for informational purposes only. The content is based on research and opinions available at the time of writing. While we strive to ensure accuracy, we do not claim to be exhaustive or definitive. Readers are advised to independently verify any details mentioned here, such as specifications, features, and availability, before making any decisions. Hero FinCorp does not take responsibility for any discrepancies, inaccuracies, or changes that may occur after the publication of this blog. The choice to rely on the information presented herein is at the reader's discretion, and we recommend consulting official sources and experts for the most up-to-date and accurate information about the featured products.